Global| Dec 11 2014

Global| Dec 11 2014IP in EMU Members: Should We Believe the Weakness or the Strength?

Summary

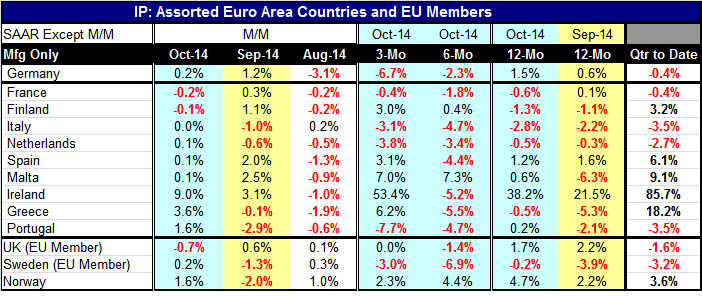

A breadth of expansion in October: Industrial output has risen in October in seven of ten early reporting EMU members and has fallen in just two. This follows September when six of ten countries advanced. However, the drop in August [...]

A breadth of expansion in October:

Industrial output has risen in October in seven of ten early reporting EMU members and has fallen in just two. This follows September when six of ten countries advanced. However, the drop in August output was so sharp and so widespread that three-month growth rates are still lower in five of ten EMU members. However, of the countries with output down sharply over three months, only Germany and Portugal have sequentially declining growth rates from 12 months to six months to three months. Only Finland has sequentially accelerating growth rates on that time path.

A breadth of expansion in October:

Industrial output has risen in October in seven of ten early reporting EMU members and has fallen in just two. This follows September when six of ten countries advanced. However, the drop in August output was so sharp and so widespread that three-month growth rates are still lower in five of ten EMU members. However, of the countries with output down sharply over three months, only Germany and Portugal have sequentially declining growth rates from 12 months to six months to three months. Only Finland has sequentially accelerating growth rates on that time path.

Uneven quarter-to-date: In the quarter-to-date, a calculation that takes the October level of output and calculates its annualized growth over the Q3 average, we find half of these countries are expanding and half are contracting. However, contracting IP is at a very slow pace in Germany and France but at a faster pace in Italy, the Netherlands and Portugal. Meanwhile, output is expanding at a brisk pace in the advancing countries: Finland, Spain, Malta, Greece and Ireland. These groups illustrate that some of the countries that have been the most depressed are starting to show some rebound. But the larger EMU members are still not doing very well and they are the ones that have the biggest impact on the EMU-area growth. Growth is not a numbers game by country; it is a weighted average numbers game and on that score there is still a lot of weakness in train.

Other Europe struggles: The early reporting European countries that do not participate in the single currency arrangement are showing more weakness than strength; two of them Sweden and Norway show sequentially weakening growth rates of output. The U.K. is not sequentially weak, but it is showing weaker growth in more recent periods generally. The U.K. and Sweden are showing falling output in the quarter-to-date while Norway is advancing on that metric.

Large countries are laggards: What is clear is that the EMU has very little momentum in its largest countries. Even though most nations showed output rises in October, in three of those with rising output, that expansion was just 0.1% in the month. The four largest EMU nations by GDP, Germany, France, Italy, and Spain, are still very much struggling.

EMU inflation connecting more dots... Inflation too lags behind the ECB goals. Year-over-year inflation is at 0.7% in Germany, 0.7% in France, 0.8% in Italy, and 0% in Spain. In each of these countries, year-over-year core inflation is still too low: it's at 1.4% in Germany, 0.8% in France, 1.1% in Italy and 0.3% in Spain. These are not the inflation results that EMU members signed up for. Meanwhile the TLTRO program from the ECB has been once again lightly subscribed. Member country banks are simply not participating in this program with much gusto. Its impact is therefore being minimalized.

Oil prices to the rescue? There may be some optimism that lower oil prices are partly to blame for the inflation undershoot and that they will yet provide a big boost to growth. The consumer stimulus will be less in Europe than in the U.S. because of the relatively greater role of taxes in European energy costs to consumers. In the U.S., we see surprising resilience in growth despite a more negative impact on industry from falling oil prices and no evidence of retardation in industry from a rising dollar. There is optimism that U.S. growth is breaking out and that it may have enough momentum to surge through these ill effects. But will it really? Maybe the lagged effects are simply still in train? If Europe is benefiting from the weak euro, why isn't the U.S. hurting from the strong dollar? November consumer spending in the U.S. was a bit better than expected. There is optimism about the possibility of consecutive quarters of 4% GDP growth. But there are also risks.

Things that are not what they have seemed: It seems too optimistic to believe that the global economy could be under such pressure and that the U.S. will carry it all on its back - doesn't it? China's fiscal revenues are weakening as we found out in a report released today. On closer inspection, the rise in U.S. average hourly earnings in the November payroll report did not extend to production workers; it was an artifact of continued wage bifurcation (skewed income distribution). Japan is still weakening not rebounding after its consumption tax hike.

The continuing pressures on Europe: Europe may stay weak longer than expected. Russia is still making trouble on its borders from the Baltic to Ukraine. Ukraine itself is near bankruptcy and is asking for a special package to prop it up. Can Europe really ignore the problems within its own community and yet join an aid package for Ukraine? The Russian economy is doing so badly and yet the Russian central bank is hiking rates with the economy skidding lower. Yet the ruble is not responding to that particular medicine. We continue to view Russia as a dangerous wounded bear. The Russian economy is in such shambles; Russia has little to lose from becoming more aggressive and Putin is just the guy to cross those old lines to restore Russia's greatness.

More risk than just Russia: While risks continue to emanate from Russia and as weakness lingers in Europe, we also see growing risks in China and a lethargic economy in Japan. It's no wonder that the dollar is under upward pressure in this environment.

The U.S. as a bastion of growth? The dollar (real effective dollar) is now above its PPP value for the only second time since it fell to an undervalued state in October 2004. However, the notion that the average real effective dollar is a good estimator of its PPP value (which is the calculation to which I refer) needs to be reconsidered in light of the some facts. The U.S. current account has been in continuous deficit since Q3 1991 and the deficit has averaged 3.1% of GDP over that period. The 2014 Q1 current account deficit is 2.6% of GDP and is reduced substantially by development of U.S. oil, not necessarily due to an improvement in overall U.S. competiveness.

In 1971 as OPEC began to influence oil prices the U.S stopped having steady strings of current account surpluses. It had only one more episode of surpluses from Q1 1973 to Q2 1976 in which surpluses outweighed deficits. That episode was undoubtedly due to the contraction of imports in a very severe recession. Since then, the U.S. has been a chronic net importer- chronic.

Can the U.S endure? Or what has changed? The question we need to ask is where anything has really changed to allow us to believe that the U.S. economy can really continue to grow with such an uncompetitive dollar? If the contraction in the current account is more due to the development of the oil patch, then we will not see any widespread improvement in industry outside that sector especially with a less competitive dollar. The stronger dollar will also help inflation to undershoot and reinforce the impact of falling oil prices helping to keep the Fed from hitting its inflation target. U.S. job growth has improved but the quality of job created has not.

Be careful what you believe: In short, there are many more reasons to fear the weakness than to embrace the strength where we see episodically in the global economy. It is a very good time to think very deeply about how you think the economy works and what you think drives growth. We need to separate that which is trend and may not last from that which is fundamental and will continue to drive growth. When we do that, we can also separate what is illusory for that which may be sustainable. The world economy is running dry. When all its members come to drink at the last remaining oasis, will that sustain them or will they drink it dry too? Exactly how strong do you think the U.S. economy is and what is the real basis for this strength? Can Europe rely on it? What is Europe's real base of strength? What are the global risks? I think the answers to these questions are more disturbing than reassuring.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief