Global| Feb 12 2014

Global| Feb 12 2014IP: Europe Plays Catch-up...Sort of

Summary

The chart shows industrial production in the euro area has moved up sharply. It is beginning to challenge the growth rate of production in the United States -or at least it was. Despite this broad move higher by European output, in [...]

The chart shows industrial production in the euro area has moved up sharply. It is beginning to challenge the growth rate of production in the United States -or at least it was. Despite this broad move higher by European output, in December, Europe logged a step backward. The US also took a step backward in December.

The chart shows industrial production in the euro area has moved up sharply. It is beginning to challenge the growth rate of production in the United States -or at least it was. Despite this broad move higher by European output, in December, Europe logged a step backward. The US also took a step backward in December.

Two steps forward, one step back?: The euro area's step back comes amid clear evidence that industrial production has been improving. For example, one year ago industrial production in the euro area was declining. Now it is advancing, but the pace of its progress is uncertain.

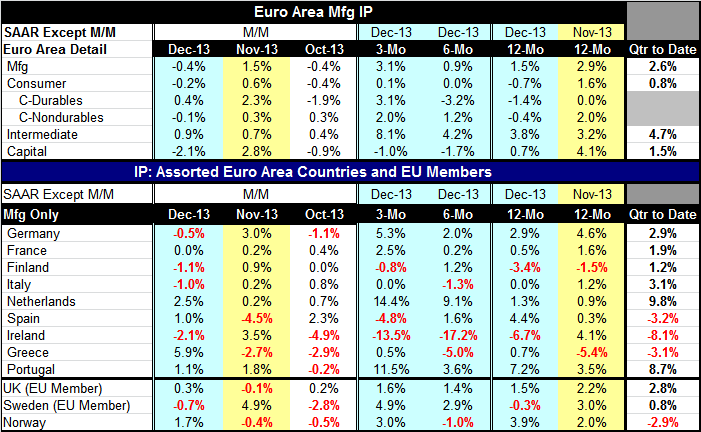

Internal divergence is still an issue: We previously documented the divergences in the growth rates of industrial output among the various European Monetary Union members listed in the table. That divergence causes problems of sorts. The fresh data on industrial production give us some detail on the composition of output across various sectors for the union as a whole. That new detail does not reassure us at all.

Manufacturing trends: Overall manufacturing output fell by 0.4% in December, following a strong gain of 1.5% in November and a drop of 0.4% in October. Despite the drop in December, manufacturing output appears to be on an upswing. Over 12 months output is up by 1.5%. Over six months it's up at a pace that it is just under a 1% annual rate. Over three months it's up at a 3.1% annual rate.

Consumer goods output lags...durables lag nondurables: The consumer sector, however, still does not seem to have developed. Output fell by 0.2% in December after rising by 0.6% in November and falling by 0.4% in October. Over three months overall consumer goods output is up at a skinny 0.1% annual rate of change. Consumer output is flat over six months. Consumer output is still falling by 0.7% over 12 months. The consumer sector is still struggling. Within the consumer goods sector, however, nondurable goods are showing a steady, if not strong, recovery with annualized rates of growth moving up from -0.4% over 12 months to 1.2% over six months and to 2% over three months. Consumer durables output, in contrast, is a strong 3.1% annual rate over three months but is down at a 3.2% annual rate over six months. On balance it is 1.4% lower over 12 months. Durable goods spending and production tend to be very cyclical. This sector should be leading nondurables output not lagging it if recovery is in gear.

Strong intermediate goods sector: In sharp contrast, intermediate goods output is showing consistent increases, rising in each of the last three months. Its growth rate has been building to a crescendo of 8.1% at an annual rate over the last 3 months as well. The strength of intermediate goods is curious since we have neither that strength in consumer goods, nor in capital goods, that should be fed by the intermediate goods sector.

Erratic capital goods output: In capital goods once again we see the pattern that shows a 2.1% drop in output in December after a 2.8% rise in November and a 0.9% fall in October, drops in two of the three most recent months. Capital goods output is up by 0.7% over 12 months. However, over six months, capital goods output is falling at a 1.7% annual rate. The capital goods sector, a sector that is the backbone of the German economy, is faltering for the euro area at-large. Even for Germany alone output in this key sector has falling over the last three months, although it is still strong over the last 6 months.

Getting a grip on performance: From these sectors' performance, it is a hard to get at what is going on in the euro area. Demand really hasn't revived and so output isn't picking up. Capital goods output isn't picking up. Consumer output isn't picking up either. In the grand scheme of the interrelated economy, if demand doesn't pick up, then supply will not be stimulated. If supply isn't stimulated and if hiring does not improve, then demand won't pick up and may backslide. Supply and demand are tied together in any economic system. Of course, there is the international sector to consider and the mechanics in the euro area are more complicated. Not all domestic demand is served by domestic supply and because of the euro area framework relatively more trading goes on within the currency union. Still, that does not explain these weak euro area-wide trends.

Is the trend still our friend?: While, on trend, it would appear that the euro area is in recovery mode, on close inspection some of the important links in the chain of growth appear to be broken. Even the German economy by itself appears to be struggling more than it had been. It could be that the trend simply will reassert itself and that growth will resume. Maybe bad weather is the real culprit here and there has been a lot of that.

Is policy the problem instead of the solution?: However, we are possibly seeing accumulating evidence that Europe's recovery simply does not have the right stuff after all. For example, is Europe implementing banking reform too early in its fragile cycle? If banks are forced to hold even more capital so soon before demand has recovered, where will the credit come from to drive consumer and business spending? It's a good question.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief