Global| May 15 2014

Global| May 15 2014IP Drops, Trend Still strong; But Does That Matter?

Summary

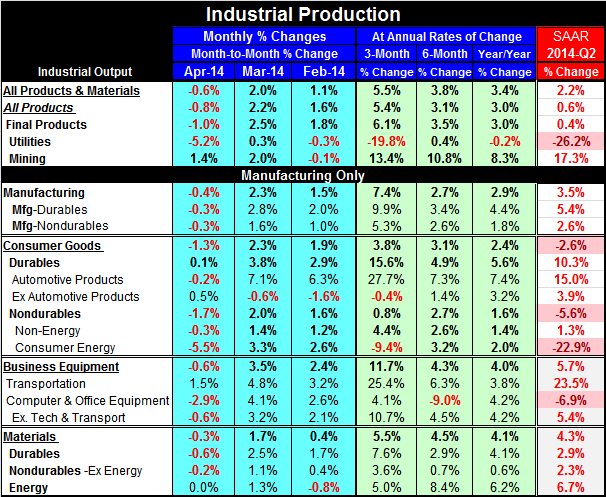

Industrial output's trend slowed in April, as output fell by 0.6% following a 2% spurt in March. Utilities' output fell sharply by 5.2% after a 0.3% gain in March. Mining output continues to be strong, slowing to a 1.4% gain after a [...]

Industrial output's trend slowed in April, as output fell by 0.6% following a 2% spurt in March. Utilities' output fell sharply by 5.2% after a 0.3% gain in March. Mining output continues to be strong, slowing to a 1.4% gain after a 2% rise in March.

Industrial output's trend slowed in April, as output fell by 0.6% following a 2% spurt in March. Utilities' output fell sharply by 5.2% after a 0.3% gain in March. Mining output continues to be strong, slowing to a 1.4% gain after a 2% rise in March.

Manufacturing output, the heart of the industrial production report, fell by 0.4% in April after a 2.3% gain in March. Despite the slowdown, manufacturing is still growing at a 7.4% rate over three months up from 2.7% over six months and stronger than its twelve-month growth of 2.9%.

Looking into the details of industrial production, consumer goods output fell by 1.3% in April. However, it still is showing accelerating trends with a 3.8% three-month growth rate that surpasses its six-month growth rate, as the six-month growth rate at 3.1% surpasses its twelve-month growth rate of 2.4%. Even with a 1.3% decline in April, consumer goods output is still accelerating. Most of that is due to durable goods production that barely ekes out a 0.1% gain in April. But consumer durables output is still flying forward at a 15.6% annual rate of expansion over three months. Nondurable goods are considerably more tempered. The output of consumer nondurables fell by 1.7% in April clamping its three-month growth rate down to 0.8%, a slowdown from its 2.7% expansion over six months and below its 1.6% growth rate over 12 months. But if we exclude the energy sector from consumer nondurables, a picture of expansion and acceleration reemerges. Consumption of energy was as affected as anything by the peculiar weather patterns that the US economy has faced early in the year.

Business equipment output fell by 0.6% in April, but only after two robust months where it rose by 3.5% in March and 2.4% in February. As a result, the three-month growth rate of 11.7% accelerated sharply from 4.3% over six months and beyond its 4% rate over 12 months. Transportation equipment output leads the growth although excluding tech and transport output is at a 10.7% annual rate, accelerating over three months as well. Business equipment output seems to be experiencing strong and balanced growth.

Turning to materials, output fell by 0.3% after a 1.7% spurt in March. Over three months materials output is accelerating at 5.5%, up from 4.5% over three months and 4.1% over 12 months. The consumption of energy materials has been strong all through this horizon; however, for nondurables excluding energy, the acceleration in materials is made clearer. For durable materials goods, there is strong growth over the period with output acceleration over three months compared to six months.

The bottom line for industrial production is that the economy is doing pretty well. In the quarter to date industrial production is up at a 2.2% rate with manufacturing up at a 3.5% rate. Consumer goods production early in the second quarter is falling at a 2.6% annual rate despite a 10.3% annual rate growth for consumer durables output. The output of consumer nondurables is falling in the quarter because the output of consumer energy goods that is down at a rapid 23% annual rate. Exclude energy products from consumer nondurables, output is increasing at a modest but still solid 1.3% annual rate. Business equipment output is rising at a 5.7% annual rate in the quarter. Materials output is up at a 4.3% annual rate in the quarter.

Weather has clearly bounced industrial output around at the turn of the year and created fluctuations in its path. What seems to be last is a sector that still is expanding since the ex-energy portions of the major sectors are all showing firm-to-strong growth. That assessment applies to sequential growth rates as well as the current levels of an industrial production relative to the first quarter average. It looks as though March and February same bounce back after previous weakness and even with a setback in April there is still solid momentum in industrial output. However, because of volatility and because the weather effect has been dominant, we want to keep our eyes on the reports in the coming months to make a final determination. But on the data before us, the industrial sectors looking solid.

Context/Synchronicity: The industrial sector taken on its own seems to be in good shape as we argue in the above paragraphs. However, the industrial sector rarely is a leading sector, as its job is to satisfy the demands for its output. US exports continue to grow, so they absorb some of this output. Capital spending in the US has been firm more than it's been strong and it absorbs another part of this output. Consumer spending has been more erratic and although there were one or two strong months, in April weakness has set in again. The inventory data tell us that inventories have been in excess for some time. That means that the goods that have been produced have piled up on the shelves as spending has slowed. With the new slowdown in retail sales, we have to wonder if some of the trends in industrial output are exaggerated. If so, some of those goods that have been produced are going to wind up as inventories and languish. If that happens, the feedback effects for industrial production will work to reduce the demand for output until consumer spending picks up and absorbs the goods that are in excess in the retail sector. While the trends in industrial production on their own seem to be fine, it is those factors that stimulate demand and invite output that matter; they seem to be walking on thin ice. For industrial production context is everything and trend is nothing.if not misleading.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief