Global| May 27 2008

Global| May 27 2008INSEE Biz Indicator is Weakening

Summary

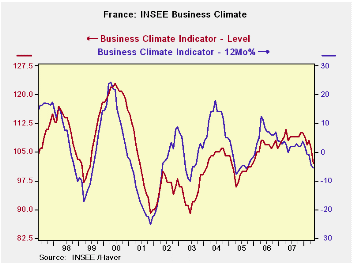

The INSEE survey of business sentiment is lower in May, as the overall index fell to 102 from 106 in April. The index (blue line) has been moving sideways until early this year. The four point drop is the sharpest since April of 2005. [...]

The INSEE survey of business sentiment is lower in May, as the overall index fell to 102 from 106 in April. The index (blue line) has been moving sideways until early this year. The four point drop is the sharpest since April of 2005. Still the climate index is above its average (since 1990) by one point. And still resides in the upper portion of its range, 58th percentile. The recent trends put it at a raw reading of -15, well below the average at -5, ensconced in the 42nd percentile of its range. The likely trend, however is extremely strong standing in the 84th percentile of its range. That one is surprising since other readings hardly seem to justify it. Overall orders and foreign orders are in about the 58th percentile of their respective ranges. Price expectations are high, in the 78th percentile of their range and well above average.

French president Sarkozy is asking the EMU to put a freeze on the VAT on fuel. Since the VAT is a percentage tax it boosts the price of fuel further each time overall oil/fuel prices rise on world markets. Fuel costs in EMU are already at extreme levels. France has been suffering though a wave of protests over high fuel costs. In the UK a protest was made along the M4 by freight haulers wanting a VAT rebate as essential users for the high fuel costs. Energy costs are clearly out of hand when we see this sort of thing.

For some reason haulers and other businesses do not think they are able to pass on high fuel costs to end users. While that may be good for the inflation fight it raised questions about growth prospects.

| INSEE Industry Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since Jan 1990 | Since Jan 1990 | |||||||||

| May-08 | Apr-08 | Mar-08 | Feb-08 | %tile | Rank | Max | Min | Range | Mean | |

| Climate | 102 | 106 | 108 | 107 | 58.0 | 105 | 123 | 73 | 50 | 101 |

| Production | ||||||||||

| Recent Trend | -15 | -7 | -6 | -9 | 42.2 | 138 | 44 | -58 | 102 | -5 |

| Likely Trend | 48 | 48 | 52 | 43 | 84.4 | 5 | 63 | -33 | 96 | 9 |

| Orders/Demand | ||||||||||

| Orders & Demand | -11 | -5 | 1 | -1 | 58.6 | 90 | 25 | -62 | 87 | -14 |

| Fgn Orders & Demand | -7 | 3 | 1 | 1 | 57.3 | 94 | 31 | -58 | 89 | -10 |

| Prices | ||||||||||

| Likely Sales Price Trend | 14 | 14 | 12 | 16 | 78.7 | 20 | 24 | -23 | 47 | 1 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief