Global| Sep 07 2006

Global| Sep 07 2006Initial Jobless Insurance Claims Fell

by:Tom Moeller

|in:Economy in Brief

Summary

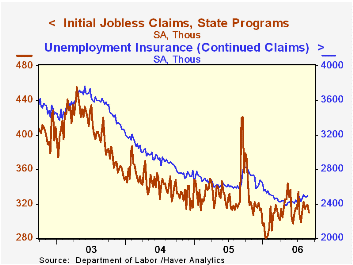

Initial claims for jobless insurance fell 7,000 last week to 310,000 from an upwardly revised level during the last full week of August. Consensus expectations had been for 315,000 claims. During the last ten years there has been a [...]

Initial claims for jobless insurance fell 7,000 last week to 310,000 from an upwardly revised level during the last full week of August. Consensus expectations had been for 315,000 claims.

During the last ten years there has been a (negative) 78% correlation between the level of initial claims and the m/m change in nonfarm payroll employment.

The four-week moving average of initial claims fell to 315,250 (-1.4% y/y).

Continuing claims for unemployment insurance rose 15,000 following a decline of 6,000 the prior week that initially was reported as a modest increase.

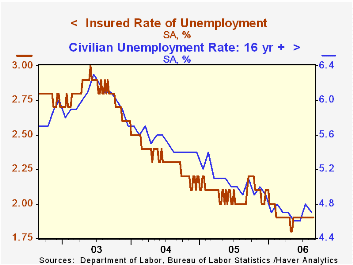

The insured rate of unemployment was steady at 1.9% where it has been since February.

The latest Beige Book from the Federal Reserve Board can be found here.

Welfare Recipiency, Job Separation Outcomes, and Postseparation Earnings: Insight from Linked Personnel and State Administrative Data from the Federal Reserve Bank of Atlanta is available here.

| Unemployment Insurance (000s) | 9/02/06 | 8/26/06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Initial Claims | 310 | 319 | -4.0% | 332 | 343 | 403 |

| Continuing Claims | -- | 2,492 | -3.5% | 2,662 | 2,924 | 3,532 |

by Carol Stone September 9, 2006

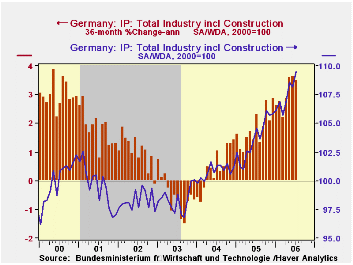

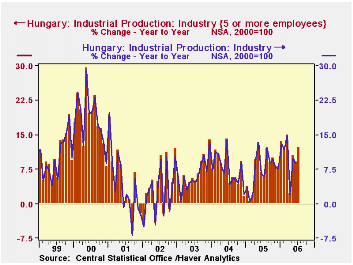

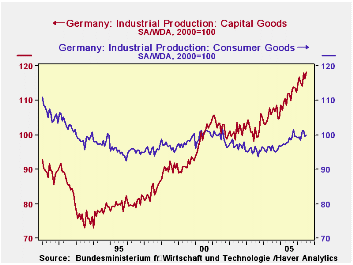

We hear so much about the development of industry in various Asian nations that it's sometimes easy to think that industry elsewhere is shriveling up and fading away. This is hardly the case, as a quick look at new production data for Germany and Hungary can show.

Industrial production increased 1.2% in Germany in July, far more than forecast survey expectations that called for 0.5%. Analysts apparently expected June's 0.4% decline to be reversed, but not exceeded, as it was. The year-on-year growth also more than reversed its prior month's performance, surging to 4.7% from a drop of 1.2%. Since the present expansion began in mid-2003, German industrial production has grown at a 3.5% annual rate.

In Hungary, production increased 1.1% in July, a third consecutive gain after a minor dip in April. The year-on-year advance is 12.2%. Growth there since early 2004 has averaged 8.7%. These figures cover firms with five or more employees; the total dataset for July will be out September 15.

In both of these countries, the strength has come in more industrial products than in consumer goods. Germany reports details on the "market groupings" of its production, and during this latest 30-month recovery period, intermediate products have averaged 4.9% annualized growth, capital goods 5.5% and consumer goods 1.5%. July's industry performance over a year ago was above average for chemicals, rubber & plastics, metals, machinery, electrical equipment and transport equipment. A similar pattern obtained in Hungary in its full dataset through June, with the addition of the mining sector, leather goods and "not elsewhere classified", which includes furniture.

Thus, while consumer goods production, particularly nondurable goods, may have shifted to other geographic regions, "heavy industry" still appears to be firmly ensconced in Europe. In fact, in both Germany and Hungary, production of these industries is a major source of growth for the entire economy.

| Industrial Production* | July 2006 | June 2006 | May 2006 | Year Ago | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| Germany, 2000=100 | 109.5 | 108.2 | 108.6 | 104.6 | 104.1 | 101.7 | 98.0 |

| % Change | 1.2 | -0.4 | 1.5 | 4.7 | 2.4 | 3.7 | 0.1 |

| Hungary, 2000=100 | 148.4 | 146.8 | 143.9 | 133.0 | 132.0 | 122.9 | 114.4 |

| % Change | 1.1 | 2.0 | 1.6 | 12.2 | 7.4 | 7.5 | 6.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief