Global| Aug 26 2013

Global| Aug 26 2013Inflation Trend-Differences Hamper Policy in EMU

Summary

While everyone is getting warm and fuzzy about the improvement in growth and in growth prospects for the European Monetary Union, the Union continues to face important issues. One issue is that growth is uneven, as we have seen. The [...]

While everyone is getting warm and fuzzy about the improvement in growth and in growth prospects for the European Monetary Union, the Union continues to face important issues. One issue is that growth is uneven, as we have seen. The Union overall is posting a rise in GDP while a number of important members continue to be mired in recession; along with that there are persisting differences in the evolution of inflation.

While everyone is getting warm and fuzzy about the improvement in growth and in growth prospects for the European Monetary Union, the Union continues to face important issues. One issue is that growth is uneven, as we have seen. The Union overall is posting a rise in GDP while a number of important members continue to be mired in recession; along with that there are persisting differences in the evolution of inflation.

In looking at the recent history and problems in this monetary union, we can argue about whether the real problem has been fiscal differences or differences in regional inflation. While they may be related, they are not the same thing.

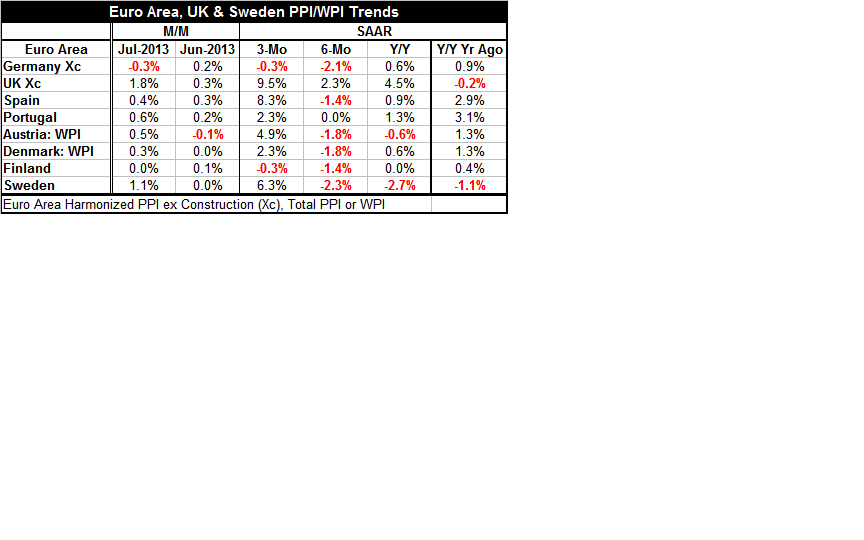

With countries in the periphery still suffering weak growth, their distress is not altogether bottling up inflation. Spain's overall PPI is growing at an 8.3% annual rate over three months compared to Germany where the index is declining at a 0.3% annual rate over three months. Year-over-year Spain's inflation is not so different up by 0.9% compared to Germany at 0.6%.

The biggest inflation divergence is in the table- fortunately - are among the Zone's single currency members those countries that are not in the single currency framework but are members of the economic union. Year-over-year the UK has a 4.5% inflation rate while Sweden is at a -2.7% inflation rate in the overall PPI.

Looking at single currency members only, that would be Germany, Spain, Portugal, Austria, Denmark and Finland, we see that over six months PPI prices are falling everywhere except in Portugal where inflation is flat at zero. However, turning to three-months, there's a difference with only Germany and Finland showing continuing price declines while Spain is posting and 8.3% annual rate of increase, Austria a 4.9% rate, and Portugal at a 2.3% rate of increase along with Denmark.

Of course, the European central bank prefers to look at inflation through the lens of the CPI, and the harmonized index of consumer prices. But inflation pressures at the producer or the wholesale level can eventually become a problem at the consumer level. And, of course, one of the things that inflation divergence tells us is that the economic union is not very well integrated and spells a problem for policy no matter what it looks at since indicator divergence (be it inflation or growth) says that there is no single gauge or group of countries it can or should look at to set policy.

If the economic union were well-integrated, inflation divergence could not and would not persist. Prosperity would come to regions that had lower inflation (output costs), that would bring an increase in output, a migration of labor and eventually cause some increase in prices there. Meanwhile, high inflation areas (high cost areas) would become less prosperous, would cut back on output, would lose labor and prices would recede. In a truly integrated monetary union profitability, sector prices, and output prices would be determined in a single framework -- not in multiple local arenas -- with persisting differences. There would always be some regional differences, but essentially those differences would be bounded by economic competition and arbitrage. The point is that in the European Union these forces really don't exist in any strong fashion. Because of this failing, the European Union needs to do other things to try to create unity in its region-wide markets. Having adopted some harmonization rules, while a laudable exercise, is not enough.

We're going to continue to monitor inflation differences in producer prices and consumer prices in all different ways because we think that these are evidence of regional disparities that once again lead to regional problems. We still think that the best way to analyze the euro-Zone is by looking at its constituent members rather than the overall index of pooled data. The problem with pooled data is those data have weights that emphasize an economy's size. That means that Germany is going to get a tremendous weight when looking at what's going on in the euro-Zone as a single unit. However, the point that has been made time and time again is that the euro-Zone is running nothing that is anything like an optimal currency area. Anyone trying to prove that it is, gives off the unmistakable sounds of someone trying to smash a square peg through a round hole.

The euro-Zone is first and foremost a political union that has a number of odd bedfellows thrown in together for the sake of political stability. Therefore the euro-Zone is a mismatched economic zone and that creates political tensions. Since it ultimately is a political animal we have to be aware of incipient political tensions that are going to be caused by the lack of economic suitability among the countries have been pulled together in the single zone with a single currency and a single monetary policy. The question is whether these countries can come to the necessary political accommodations given their unsuited economic circumstances. That means we have to continue to look at the divergence within the Zone in order to understand it and to assess its progress and viability. That means that looking at overall euro-Zone data will lead to an important loss of information. We recommend looking at the euro-trees instead of the euro-forest.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief