Global| Mar 03 2020

Global| Mar 03 2020Inflation's Comeback Is Blunted As Coronavirus Is Hunted

Summary

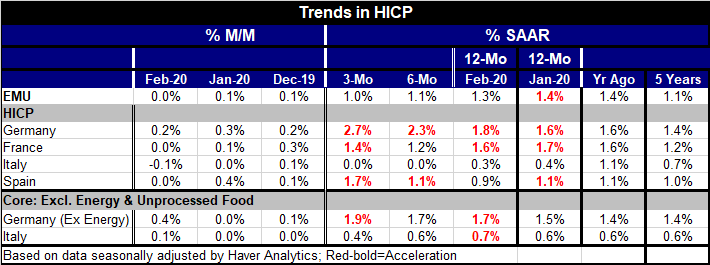

EMU inflation was dead flat at zero in February; the year-on-year rate ticked down to 1.3% from 1.4%. The German economy saw its year-on-year rate rise in February compared to January. But in France, Italy, Spain and in all of the [...]

EMU inflation was dead flat at zero in February; the year-on-year rate ticked down to 1.3% from 1.4%. The German economy saw its year-on-year rate rise in February compared to January. But in France, Italy, Spain and in all of the EMU, the month’s year-on-year rate ticked lower. However, in Germany and Italy, ex-energy inflation rates ticked higher in February relative January.

EMU inflation was dead flat at zero in February; the year-on-year rate ticked down to 1.3% from 1.4%. The German economy saw its year-on-year rate rise in February compared to January. But in France, Italy, Spain and in all of the EMU, the month’s year-on-year rate ticked lower. However, in Germany and Italy, ex-energy inflation rates ticked higher in February relative January.

Inflation rates overall are not trending lower. The sequential rate patterns from 12-months to six-months to three-months are clearly trending higher only in Germany and in Spain. In France and Italy, three-month inflation rates are below the pace of 12-month inflation. The near-term inflation path is still somewhat muddled.

Even so putting trend aside and looking at year-on-year rates of inflation, regardless of the trend or pressure, what is happening is that inflation is still below its targeted pace of just-below-2%. For the EMU, the year-on-year pace is only 1.4%. Oil prices are still weak and the virus impact will slow the economy and is more likely to bring inflation rates lower. It is clear that in this transition period as the virus spreads economic data should be viewed with some degree of skepticism and not taken wholly at face value.

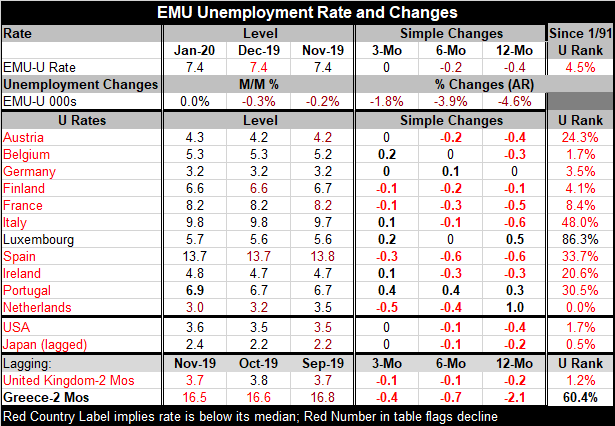

European rates of unemployment were flat at their lows reached just before the 2008 recession/financial crisis as of January. Of the 11 long-term EMU member countries that are also current in reporting data, only four have declines in their unemployment rates over three months. Five have rates that are higher on balance. Two have unchanged rates of unemployment. Greece, that is a lagging reporter, is still seeing its unemployment rate fall- that is as of November.

What we are seeing is the ongoing impact of the global trade problem. These data are up to date through January and are unlikely to have any corona effect in them as of yet. But based on what we know about the virus spreading, the impact is coming. Neither monetary policy nor fiscal policy can stop it because the way the virus is brought under control is by slowing and containing economic interactions. That will slow growth. There is no policy alternative since slowing growth is the policy.

However, no policymaker is going to say this. Instead, we are going to see policy moves announced that will be as futile as the kid at the beach who digs a hole in the sand and sees it fill with water then tries to bail it out…to no avail. When growth is being shut down and restrictions on travel and other activities are being put in place, trying to stimulate the economy is an oxymoron. There needs to be a policymaker in the house that can play the role of an adult in the room to say that growth is going to slow, but policymakers will keep the economy’s backing strong and keep the impact from harming the real fabric of the economy. When the virus passes, growth can and will spring back. At that time- AT THAT TIME- policy steps can and will be taken to boost growth. But the economy for now should be viewed as if it is in a period of convalescence when its performance will be curtailed to help it restore its health later. That may not be the message you want to hear, but that is the reality. We can look to China to see how it will probably play out- at least to some extent. I doubt that any central bank head or policy-maker is going to utter those words but keep them in mind because they reflect the real situation.

The unemployment scene

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief