Global| Sep 11 2013

Global| Sep 11 2013Inflation in the Euro Area: Is it the Fly in the Ointment?

Summary

The chart shows that inflation has been diminishing in countries that have had austerity imposed upon them. If the goal of austerity has been to reduce their price inflation trend, it has been successful. If the goal has been to [...]

The chart shows that inflation has been diminishing in countries that have had austerity imposed upon them. If the goal of austerity has been to reduce their price inflation trend, it has been successful. If the goal has been to restore their competitiveness to where it was when the Euro Area was formed, it still has a long way to go. If the goal is to restore budget balance so that moving forward these countries can have more balanced finances, the jury is out on that until we see how each responds when growth returns.

The chart shows that inflation has been diminishing in countries that have had austerity imposed upon them. If the goal of austerity has been to reduce their price inflation trend, it has been successful. If the goal has been to restore their competitiveness to where it was when the Euro Area was formed, it still has a long way to go. If the goal is to restore budget balance so that moving forward these countries can have more balanced finances, the jury is out on that until we see how each responds when growth returns.

In simple terms, it's very hard for austerity, a very broad and meat-handed economic approach to create the sort of fine-tuning or adjustment that we would like to see in some of these troubled EMU member countries.

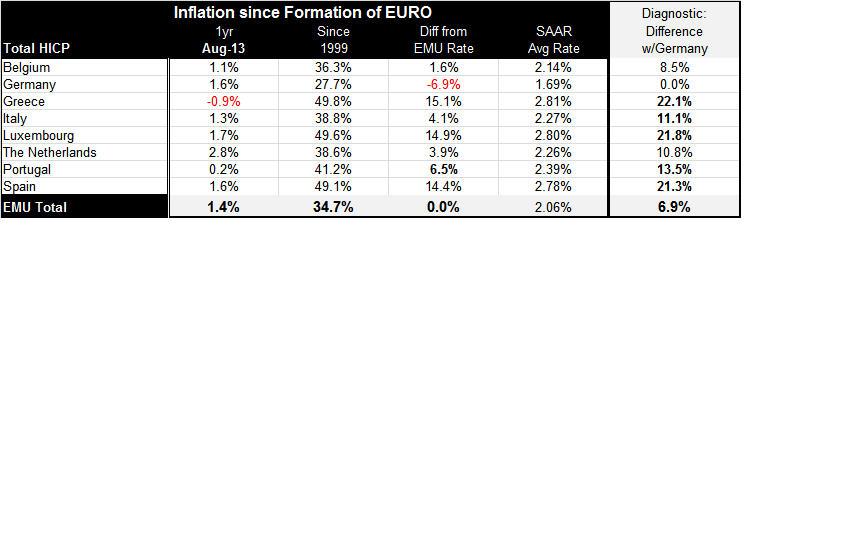

The table below makes it pretty clear where a lot of the problems have come from. Since the Euro Area was formed Germany has continuously run the lowest rate of inflation in the monetary union. Since the price target for the European Central Bank was/is a weighted-average of its members and, since Germany is the largest member as well as the member with the lowest inflation rate, year in and year out, Germany helped the ECB to hit its inflation target while many countries ran inflation rates that were over the top of the ECB's range. Indeed, among this group of countries we see that only Germany has run inflation lower than the EMU rate since the start of the Monetary Union. The German price level is 6.9% below the aggregate rise in the EMU price level. The closest country to Germany in this table is Belgium, whose rate is 1.6% higher than the EMU rise making it 8.5 percentage points higher than the German inflation rise. After Belgium, the Netherlands trails Germany's aggregate price rise by 10.8 percentage points, Italy trails it by 11.1 percentage points and so on. The countries that had developed the most inflation disadvantage are Greece with the price level that rose 22% more than Germany's, Luxembourg, where the price level rose 21.8% more than Germany's and Spain whose price level rose 21.3% more than Germany's. And, of course, except for Luxembourg - the clear odd-man out in the Euro Area because it is so clearly different in its economic structure as a financial center - the countries with the biggest inflation difference with Germany have been in the group that has had the most problems.

This can cause us to wonder whether the problem has been Germany rather than the rest of the zone.

Because of the high weight attached to the inflation performance in Germany, the ECB continued to act as though it had its inflation target because the metric it looked at said that it did - even though many countries continued to post rates of inflation that were high above the EMU target and high above Germany's. Perhaps had the ECB been shooting at a target like an un-weighted average or the median inflation rate among members, it would have been looking at a different inflation result each year and that possibly could have resulted in a different dynamic in monetary policymaking. But as it was since the ECB was hitting its target and since the Germans were always very concerned about the ECB target low German inflation ensured that that target was hit and so the Euro Area was able to go on year in and year out under the illusion that the European Central Bank was doing his job when in fact entrenched pockets of excessive inflation had been nurtured from the very start of the Euro Area. No one in policy circles that mattered worried about his compositional inconsistency.

One of the things that makes this a very interesting anomaly is that it was because of these inflation differences that there had been some of the skepticism about forming the European Monetary Union in the first place. It was because of these differences that Europe adopted precursor exchange rate regimes involving the formation of the `currency snake' and of the `currency snake in the tunnel' to try to homogenize disparate rates of inflation. While these mechanisms helped to reduce inflation, in the high inflation countries inflation differences were not eradicated and, as we can now clearly see, they help to usher in an environment that planted the seeds of its own destruction. The problem in the Euro Area wasn't simply regional fiscal excesses. It was the lack of competition and the lack of capital market arbitrage that would have kept these kinds of inflation differences from persisting even if they had emerged. Capital flowed to China much more freely than it flowed across borders in EMU.

The imposition of austerity on members that are having capital market problems is only a patch, not a solution. The solution for Europe would be to invite much more integration, perhaps more than the Europeans really want. Part of the problem of the Monetary Union - and the economic union - that the members are willing to homogenize to some extent but maybe not enough to support a single currency. But that will be a judgment eventually made by markets, reality, and history.

The table which includes only those countries that are early reporters of the August harmonized index of consumer prices shows that, in the new environment with austerity being imposed on more countries, Germany, which historically has had the lowest inflation rate by a long shot among EMU members, is no longer posting the lowest inflation rate over the last year. In fact over the past year four countries have a lower inflation rate than Germany and one has the same inflation. Spain's inflation rate is the same, Belgium's inflation rate is up by only 1.1% compared to Germany's 1.6%. Italy's inflation rate is lower, too, up by just 1.3%. Portugal's inflation rate is up by 0.2% and Greece's inflation rate is showing price level declines, lower by 0.9% year-over-year.

Despite this sort of inflation `progress,' it is progress that has been achieved at a terrible price. The lack of growth, the economic contraction, and the rise in unemployment rates among these countries are now making inflation progress represent a very steep cost, which pays for what is essentially minor progress in moving these countries' price levels back toward Germany's. It's important to remember that these legacy price differences listed in the table continue to exist. Since the formation of the Euro Area, Greece's price level has risen 49.8% Germany's has risen 27.7%. Those figures represent differences in prices that endure even AFTER the progress Greece has made to date. Even as Greece clawed back 2.7 percentage points of lost competiveness over the past 12 months, it continues to lag well behind Germany in terms of where its price level resides.

While I will not go into any detailed digression here, we know from the history of the United States that price level differences can exist and persist and that an economy still can flourish in a common currency area. But there have to be reasons why price levels diverge. Those reasons have to stem from economic differences that make sense. In United States, very high price levels in California and New York contrast with much lower price levels for houses and property in Wyoming and in the Dakotas partly because of the differences in lifestyle, differences in economic development, the differences in economic structure, and a huge distance between these various regions. It's not so clear to me that the differences among European `states' are as diverse as that.

When I look at Europe I continue to think of these underlying price differences that persist. I think of the different political structures and of the countries with the different economic objectives and philosophies. I wonder about Finland with a very different set of values from much of the rest of the Euro Area and if it is going to be able to continue to find solace as a Euro Area member. While the Finns will raise taxes and engage in expenditures to harmonize living standards within their country, they balked at paying for bailouts and other countries. Similarly, the Germans seem to think that the model of reuniting Germany should be a model for development in the rest of the Euro Area without recognizing that East Germany got a lot of help from West Germany, and that United Germany is not willing to provide that same kind of support the rest of the union.

Country differences still matter in the monetary union even though the currency is the same. And in this union, that is still trying to put a banking union together, and that has no fiscal union, the currency turns out to be pretty thin glue against the kinds of strains that it's facing. The future for Europe depends not on the currency being the same but on the values and the convictions of the European members. They either must find their values coming closer together or they must be willing to engage in economic transfers that will allow countries with different values to sustain them. As far as I can see Europe is a long way from reaching any of these decisions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief