Global| Mar 14 2008

Global| Mar 14 2008Inflation Flares Further in the Euro Area

Summary

The upward-revised headline EMU inflation rate leaves the ECB even more perturbed over events. While a tenth of a percentage point upward revision is no big deal, it makes the highest inflation on record since the Euro Area was formed [...]

The upward-revised headline EMU inflation rate leaves the ECB even more perturbed over events. While a tenth of a percentage point upward revision is no big deal, it makes the highest inflation on record since the Euro Area was formed even higher. Some members have said that the revision is a further risk to second round effects. To the extent that the public sees it and makes that their wage target based on that higher rate, it is so.

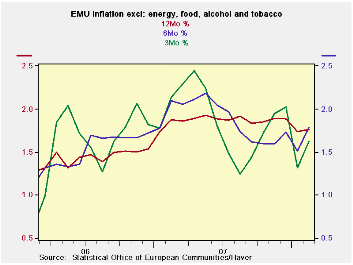

The chart on the lest shows the ‘core’ inflation rate, without food and energy and ‘sin’ (alcohol and tobacco). The core rate is in better shape and it shows a muted pass-through of inflation. At 2.4% year/year it is about what US core inflation is (2.3% for ex food and energy inflation). The ECB is making a big deal of inflation over its ceiling of 2% while the Fed ‘references’ the core PCE which is lower than the Core CPI. The Core CPI is now below its Core-PCE-equivalent ‘reference ceiling’ of 2.4%. But since the ECB thinks in terms of headline inflation only, its shortfall is not 2.4% (core) Vs 2% but 3.3% Vs 2% and that is a much bigger distance. For the record US headline inflation is even higher. Who is doing this the right way?

Central banks are what they make themselves into and what their mandate demands. The US has seen enough weakness to react to the economy and financial strife by cutting rates. And that works for a central bank with a dual growth and inflation mandate. The ECB has no such mandate. It is strictly to fight inflation and so it is doing that, for better or worse. Meanwhile, however, the euro continues to climb and that has its own deflationary consequences for the Euro Area. It seems everyone in the Euro Area is worried about it. Perhaps that is the way out for the ECB to see what the strong euro is doing to help fight inflation as well as undermine growth. Holding policy steady until inflation breaks noticeably could be a problem since commodity prices are high enough that even with euro strength they are and will be an inflation contributor for a while longer. Central banks have entered the very foggy ‘judgment zone.’

One thing we can conclude is that with the weaker economy in the US and the brunt of the financial problems there, it is a good thing that the Fed is the central bank with the dual mandate and not vice versa. In the meantime look for central banks to muddle though under their own existing rules. Inflation may be near peaking since it’s hard to imagine another move up in commodity prices to any significant degree from these levels.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Feb-08 | Jan-08 | Dec-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | 0.3% | 0.3% | 0.2% | 2.8% | 4.5% | 3.3% | 1.9% |

| Core | 0.3% | 0.1% | 0.2% | 2.6% | 2.9% | 2.4% | 1.9% |

| Goods | 0.3% | -0.5% | 0.1% | -0.8% | 5.3% | 3.8% | 1.5% |

| Services | 0.5% | -0.2% | 0.9% | 4.9% | 1.1% | 2.5% | 2.4% |

| HICP | |||||||

| Germany | 0.2% | 0.3% | -0.2% | 1.1% | 3.9% | 2.9% | 2.0% |

| France | 0.0% | 0.3% | 0.4% | 3.0% | 4.1% | 3.2% | 1.2% |

| Italy | 0.6% | 0.1% | 0.4% | 4.2% | 4.7% | 3.1% | 2.2% |

| Spain | 0.4% | 0.2% | 0.5% | 4.6% | 6.1% | 4.4% | 2.5% |

| Core:xFE&A | |||||||

| Germany | 0.3% | -0.2% | 0.3% | 1.5% | 2.1% | 2.2% | 1.8% |

| France | 0.1% | 0.3% | 0.3% | 2.7% | 2.7% | 2.3% | 1.4% |

| Italy | 0.4% | 0.0% | 0.3% | 2.7% | 3.1% | 2.5% | 2.1% |

| Spain | 0.3% | 0.2% | 0.3% | 3.2% | 4.1% | 3.3% | 2.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief