Global| Sep 07 2007

Global| Sep 07 2007Industrial Production Growth Slips in Germany

Summary

The ratchet lower in German production follows the sharp weakening in German industrial orders. The sequential growth rates in the table below do not show the slowing due to base effects (in April). The table shows that IP was soft in [...]

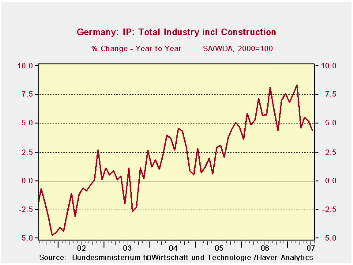

The ratchet lower in German production follows the sharp weakening in German industrial orders. The sequential growth rates in the table below do not show the slowing due to base effects (in April). The table shows that IP was soft in July and weak in June. But April was a very weak reading so that the May gain carries the three-month average to a decent three-month growth rate. Yes IP is clearly slowing, not accelerating, as the accompanying chart makes. The weakness is in consumer goods. Consumer good output is down in two consecutive months and in the quarter to date; it is off at an annual rate of 12.3%. But, capital goods output remains strong. It is up by 1.1% in July; a small drop in June was sandwiched between strong performance in May and July. In the quarter it is growing at an annual rate of 10.2%. Intermediate goods output seems to be slowing as well but is carrying momentum in the new quarter. Construction is choppy and is flat in the new quarter.

Still German IP is growing at a 4% Y/Y rate and that is not weak, just slower than it was. The six-month growth rate is weaker at 3.2%. The real question is that with the US slowing and the OECD leading indicators pointing to weaker growth will the strength in capital equipment remain in place? That seems unlikely. Germany keeps waiting for the consumer to join the party but that’s as long a wait as for President Bush to pull the troops out of Iraq. Even that one might come to fruition before the German consumer gets wild with the purse strings.

Europe does seem to have an authentic slowing in train. We can’t quite pinpoint how weak things will get. But, except for China, a global chill seems to have set in and surprisingly it seems to be registering before we have seen the impact from the financial turmoil that developed in August and whose larger impacts should not be seen until September or thereafter. That makes this slowing all the curious and problematic for policymakers. The OECD and IMF growth warnings now have more substance with a weakening US job growth trend already as a reality.

For Germany a further slowing lies ahead. Germany has prospered on the strength of foreign demand; now that a slowdown is in gear in the wake of its VAT tax hike the consumer will probably become even more cautious. Capital spending is pro-cyclical so it will slow, too.

Europe is no longer what it one was. Its day in the growth-sun was short-lived. And its rate of unemployment is still stubborn at a high level. Germany is a prime example of these trends.

| Saar except m/m | Jul-07 | Jun-07 | May-07 | 3-mo | 6-mo | 12-mo | Quarter-to-Date |

| IP total | 0.1% | -0.2% | 1.9% | 7.6% | 3.2% | 4.4% | 3.7% |

| Consumer | -0.8% | -2.7% | 1.3% | -8.6% | -2.1% | 0.6% | -12.3% |

| Capital | 1.1% | -0.2% | 2.1% | 12.4% | 5.2% | 7.7% | 10.2% |

| Intermediate | -0.2% | 0.6% | 2.1% | 10.4% | 3.7% | 6.4% | 5.5% |

| Memo | |||||||

| Construction | 1.3% | -2.0% | 0.2% | -2.0% | -18.5% | -4.5% | 0.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief