Global| Jul 17 2013

Global| Jul 17 2013Industrial Orders Show Some Progress

Summary

Global factory order trends are not exactly calling out the global fire department to quell the blaze of growth. But the chart above clearly shows that there is a lull in the rate of decline of orders for the US, Germany and even [...]

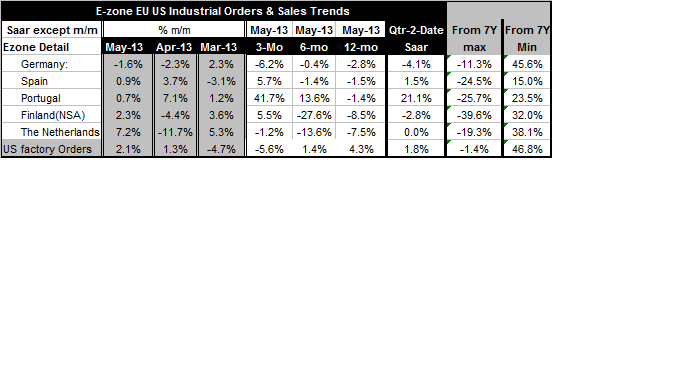

Global factory order trends are not exactly calling out the global fire department to quell the blaze of growth. But the chart above clearly shows that there is a lull in the rate of decline of orders for the US, Germany and even Spain in the euro-Zone.

Global factory order trends are not exactly calling out the global fire department to quell the blaze of growth. But the chart above clearly shows that there is a lull in the rate of decline of orders for the US, Germany and even Spain in the euro-Zone.

In the quarter-to-date for these early-reporting countries we see orders are higher from all but Germany and Finland. In May, only German orders fell. Portugal, while struggling with its adjustment program and still laboring under political instability for its governing regime, but has seen a strong rise in orders two-months into the second quarter.

What is surprising is the German weakness which may reflect Germany's ties to China and China's switch to domestically oriented growth and all the dislocation that has entailed. While China is still fast-growing by global standards it is weaker relative to tis past trends.

US order growth leads the parade over 12-months where European orders still are declining across the board- but by less than over the past year, generally. Over six months Portugal's orders outstrip growth in the US, while over three-months US orders have turned negative along with orders from the Netherlands and Germany. Those are traditionally strong European economies.

Three-month growth rates show acceleration in Portugal, Spain and Finland. These are not exactly traditional drivers of European growth.

Europe is still undergoing changes and is shifting gears but always in the same direction. There is good news today on the sharp drop in claimants in the UK economy. But construction output in the euro-Zone is still contracting yet it has slowed its rate of descent. Europe is much more on thin ice this summer that on a clear path of mending its ways. The cross currents in economic trends and the upside down nature of having German orders lagging Spain and Portugal is just one example.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief