Global| May 16 2014

Global| May 16 2014In Europe Auto Sales Rebound! Are Auto Sales/Registrations a Barometer of Growth?

Summary

Perspective: As we get excited about the return to growth in Europe, or at least hope that it will return to growth after what was a worse-than-expected first-quarter, it's important to look back and think of days gone by. While I [...]

Perspective: As we get excited about the return to growth in Europe, or at least hope that it will return to growth after what was a worse-than-expected first-quarter, it's important to look back and think of days gone by. While I know the old expression, "there is no good crying over spilled milk," it's important to understand where the European economy is today, compared to where it has been. The chart does exactly that with some brutal honesty. When we are predisposed to look at growth rates while assessing economic data, it's a good thing once in a while to go back and look at levels of activity from the past. The chart looks at the level of retail sales volume for the European Monetary Union compared to auto registrations for the European Union. In both cases, what we see is the enormous gap between the current selling pace of autos and where it was at the past peak. There is also a large gap between the current volume of retail sales compared to where sales were at their past peak. There have been huge drops in demand in both of these markets. Despite putting growth back in gear, there are still great shortfalls compared to the past.

Perspective: As we get excited about the return to growth in Europe, or at least hope that it will return to growth after what was a worse-than-expected first-quarter, it's important to look back and think of days gone by. While I know the old expression, "there is no good crying over spilled milk," it's important to understand where the European economy is today, compared to where it has been. The chart does exactly that with some brutal honesty. When we are predisposed to look at growth rates while assessing economic data, it's a good thing once in a while to go back and look at levels of activity from the past. The chart looks at the level of retail sales volume for the European Monetary Union compared to auto registrations for the European Union. In both cases, what we see is the enormous gap between the current selling pace of autos and where it was at the past peak. There is also a large gap between the current volume of retail sales compared to where sales were at their past peak. There have been huge drops in demand in both of these markets. Despite putting growth back in gear, there are still great shortfalls compared to the past.

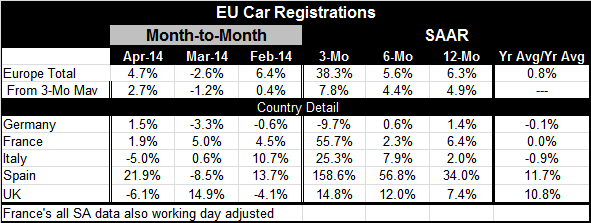

Current events: Auto registrations in Europe rose by 4.7% in April, offsetting a 2.6% drop in March. Registrations were up by 6.3% over 12 months. The sector's sequential growth rates show that strong sequential gains have turned even stronger over three months.

Even so, nothing can be taken for granted with auto sales because they are so volatile. For example, the 4.7% gain in April turned to a 2.6% drop in March that was preceded by a 6.4% rise in February that itself was preceded by a 6.8% drop in January. These are huge oscillations in month-to-month percent changes. Changes this great wreak havoc with attempts to calculate even longer-term growth rates let alone to make sense of them. For instance, car sales are up by 6.3% over 12 months; however, if they can fall by 6.8% in one month, how can we even be sure of the 12-month trend?

The chart for retail sales and auto registrations shows that despite this volatility, an upward trend is clear. Retail sales volumes in the EMU have moved up off their lows but still are not showing substantial upward momentum. On the other hand, auto registrations have also moved up off their lows; despite some volatility around trend, the trend is very clearly moving higher. It is interesting that in the United States the sales pace of motor vehicles has been on a steady march during the course of the recovery despite its weakness. In Europe, too, the path of auto sales encourages us to believe that the economic recovery is real and lasting as auto sales trace a much clearer and firmer recovery path than do other metrics.

For Germany, France and Spain, we can a look at the recovery of real retail sales excluding autos. In Germany, retail sales have recovered 80% of the past peak; in France, they have recovered 87% of the past peak, but in Spain, they have recovered only 5% from their trough to their past peak. In Italy, we have nominal retail sales excluding autos; there, nominal sales remain at the cycle low. Not only are European retail sales and auto sales well short of the past peaks but there is great variation across countries.

Auto registrations show vastly different measures of resiliency across countries. Sales in the UK are only 6% below their cycle peak sales. In Germany and France, sales are about 30% off of their cycle peaks; in Italy and Spain, sales were about 40% below their past cycle peaks.

But viewed as a time series, a sequential path of data, auto registrations have put together seven straight months of year-over-year gains. October 2013 was the first year-over-year gain in auto registrations for EU nations as a whole as they switched to a growth rate of 4.7% following a -2.6% year-over-year drop in September. From that point onward, registrations oscillated between year-over-year gains of 4% and 6%. In April 2014 the year-over-year gain of 6.3% follows a weakening year-over-year gain of just 1.6%, which is the weakest year-over-year gain since those metrics turned positive back in October 2013.

Meanwhile, European retail sales volumes, which lag by one month, rose by 0.3% in March and were up 0.9% year-over-year that time. On the same horizon as retail sales, motor vehicle registrations rose by 2.1% in March and were up by 1.2% year-over-year (and were set to accelerate sharply in April).

Of the five countries in the table, three of them had gains in vehicle registrations in April. They were Germany, France and Spain. There were declines for Italy and the United Kingdom.

Still, the UK has a long string of year-over-year auto registration gains; its string stretches back an astounding 26 months. The next longest string is from Spain at seven months. Italy has a string of four consecutive months; France has a string of two months in a row. Germany has a one-month string of increases, but the decline of last month was the first decline in seven months. The persistence of year-over-year auto registration gains in the UK is quite impressive.

Even so, the strongest year-over-year gains have come from Spain, where sales are up by 34% year-over-year. In April, UK sales are up by 7.4% by comparison, France by 6.4%, Italy by 2%, and Germany by 1.4%. For some of the periods back to September 2013, UK year-over-year sales do surpass Spain's, but in September 2013 Spain posted a year-over-year gain of 24%, then in October a gain of 34%, and then a gain of 20% in November. On balance since September of last year, Spain's auto sales have been expanding even faster than UK sales.

Car sales in these markets are good markers for economic recovery. From August 2011 until February 2013 when Europe was weak, auto sales fell in a range of 100% to 66% of these six markets. After February 2013 these percentages slid and by August 2013 none of these countries had declining auto sales, as sales in each country increased in August 2013. From that point on, the percentage of these markets with sales increasing has ranged from 100% to 66%, exactly the mirror image of the previous period when registrations and the economy both were weak.

Auto sales remain a marker of continuing growth for the US and Europe. In both cases, auto sales have served as a very good barometer in both boom and bust periods. We can hope that that functionality continues. Interestingly, the pace of auto registration gains remains the lowest in Germany. And Germany has the weakest upward momentum in this group of countries. But Germany also has a relatively low variance for sales.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief