Global| Mar 18 2005

Global| Mar 18 2005Imported Price Inflation Up

by:Tom Moeller

|in:Economy in Brief

Summary

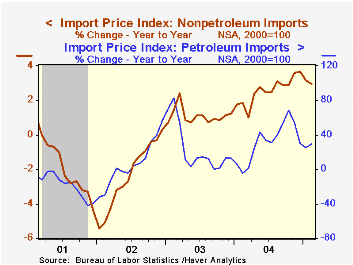

Import prices rose 0.8% last month and about matched Consensus expectations for a 0.7% rise. The prior month's increase was revised down slightly due to a lessened gain in petroleum prices but the estimated rise in nonpetroleum prices [...]

Import prices rose 0.8% last month and about matched Consensus expectations for a 0.7% rise. The prior month's increase was revised down slightly due to a lessened gain in petroleum prices but the estimated rise in nonpetroleum prices was revised higher.

Petroleum prices jumped 3.9% on top of the 3.4% surge the prior month. So far in March the price of Brent Crude oil has averaged $52.15 per barrel, up 14.2% versus the $45.66 averaged last month.

Other than oil, import prices continued to move moderately higher. Prices for nonauto consumer goods rose 0.2% (1.0% y/y) though prices in most categories were little changed. Capital goods prices also were unchanged m/m (-0.6% y/y) but lower computer prices (-0.4% m/m, -6.8% y/y) accounted for most of the weakness. Excluding computers capital goods prices rose 0.2% (2.5% y/y) and contrasted with price deflation in excess of 2% early in 2002.

Export prices were unchanged last month as a 0.9% decline (-8.2% y/y) in agricultural prices offset a 0.1% (4.7% y/y) gain in nonagricultural export prices.

Exchange Rates and the Prices of Manufacturing Products Imported into the United States is a 2002 article from the Federal Reserve Bank of New England.

| Import/Export Prices (NSA) | Feb | Jan | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Import - All Commodities | 0.8% | 0.7% | 6.1% | 5.6% | 2.9% | -2.5% |

| Petroleum | 3.9% | 3.4% | 26.6% | 30.4% | 21.0% | 3.0% |

| Non-petroleum | 0.2% | 0.3% | 2.9% | 2.6% | 1.1% | -2.4% |

| Export - All Commodities | 0.0% | 0.9% | 3.4% | 3.9% | 1.6% | -1.0% |

by Tom Moeller March 18, 2005

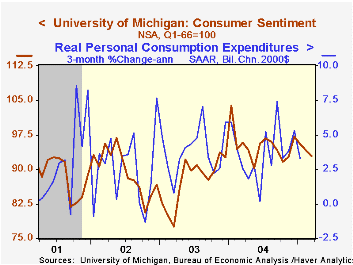

The preliminary March reading of consumer sentiment from the University of Michigan fell to 92.9. The 1.3% m/m fall was similar to the declines logged during the prior two months. Consensus expectations had been for a slight rise to 94.8. During the last ten years there has been a 75% correlation between the level of consumer sentiment and the y/y change in real PCE.

The reading of current conditions fell for the second month. The 1.7% decline was led by a 6.0% drop (-7.3% y/y) in the sentiment of families earning more than $50,000 per year. Sentiment in families earning less than $50,000 per year rose 7.0% (0.8% y/y).

Consumer expectations slipped 0.9% (-5.9% y/y) for the third consecutive monthly decline as the expected change in real income fell 4.7% (-8.0% y/y).

The University of Michigan survey is not seasonally adjusted.The mid-month survey is based on telephone interviews with 250 households nationwide on personal finances and business and buying conditions. The survey is expanded to a total of 500 interviews at month end.

Reexamining the Consumption-Wealth Relationship: The Role of Uncertainty from the Federal Reserve Bank of New York is Available here.

| University of Michigan | Mar | Feb | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Consumer Sentiment | 92.9 | 94.1 | -3.0% | 95.2 | 87.6 | 89.6 |

| Current Conditions | 107.3 | 109.2 | 0.5% | 105.6 | 97.2 | 97.5 |

| Consumer Expectations | 83.6 | 84.4 | -5.9% | 88.5 | 81.4 | 84.6 |

by Carol Stone March 18, 2005

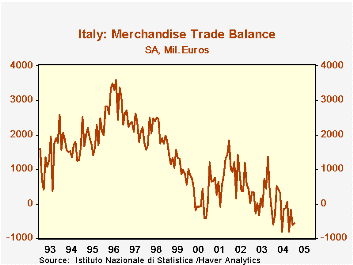

Italy's merchandise trade accounts have turned to a deficit position, with the total balance for 2004 in deficit for the first time since 1992. In January, reported today by Italy's National Institute of Statistics, the deficit was €554 million, seasonally adjusted, nearly the same as December's €609 million. Exports eased €168 million, while imports were off €223 million. Longer trends in exports and imports indicate that adverse developments on both sides of the trade accounts generated the deficit.

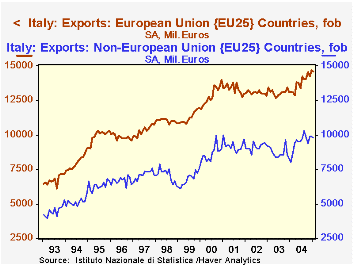

Exports drifted downward from late 2001 until early last spring. This slack was reflected in shipments to customers elsewhere in the EU and also to non-EU areas; see the accompanying graph. By type of product, all three major categories were flat: consumer goods, investment goods and intermediate products. The latter two have rebounded in recent months, while consumer goods exports remain sluggish.

Imports didn't expand in that 2001-2003 period, but they did stay steady as exports declined, and they have run up rapidly since last April. The surge in energy prices is an obvious driver of this growth, but notably, consumer, investment and intermediate goods categories have all participated, nearly equally. It will be interesting in coming months to see if the continuing pressure on energy prices will eventually eat into demand for other goods and services, in Italy, but also among Italy's trading partners.

| Italy: Trade | Jan 2005 | Dec 2004 | Nov 2004 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total Trade Balance, Months SA, Mil.Euros | -554 | -609 | -170 | -1513 | +2751 | +8815 |

| Exports, NSA, Yr/Yr % Chg | 11.0 | 18.7 | 15.3 | 7.7 | -2.0 | -1.5 |

| Imports, NSA, Yr/Yr % Chg | 7.4 | 20.5 | 19.1 | 9.4 | 0.3 | -1.1 |

| Energy, NSA, % of Imports | ||||||

| EU25, Months SA, Mil.Euros | -490 | -486 | -117 | -2799 | -197 | +1045 |

| Non-EU25, Months SA, Mil.Euros | -64 | -123 | -53 | +1288 | +2949 | +7772 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief