Global| Aug 25 2017

Global| Aug 25 2017IFO Tips Back from the Heights

Summary

Still an exceptionally strong report The IFO continues to show exceptionally strong readings. This month's Markit diffusion report also produced news of more strength in the industrial sector although the German services sector [...]

Still an exceptionally strong report

Still an exceptionally strong report

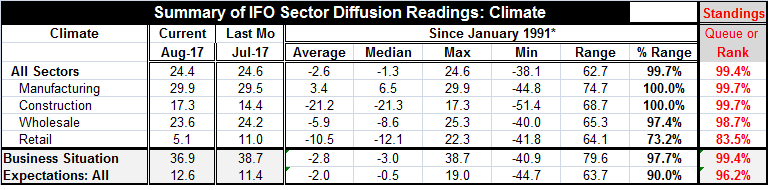

The IFO continues to show exceptionally strong readings. This month's Markit diffusion report also produced news of more strength in the industrial sector although the German services sector continues to show some very laggard behavior in the Markit framework. In the IFO framework, all is well or even better. All is strong. The IFO all-sector index stands this high or higher since 1991 only 0.6% of the time. Two of the four sectors are on peak readings for that period: manufacturing and construction. Wholesaling is higher only about 1.3% of the time. Retailing qualifies as the 'weak sector' with a queue ranking in its 83rd percentile that is higher only 17% of the time and stands some 27% below its all-time strong reading.

The overall metrics are very strong

The overall business situation reading scores a 99.4 percentile standing. It is rarely stronger. Expectations register a 96.2 percentile queue standing.

The month-to-month stuff

Month-to-month the all-sector index 'pulled back' to 24.4 in August from 24.6 in July. It's really not much of a consolidation move. Manufacturing and construction continued to reach higher levels with each of them establishing new high readings since 1991. Wholesaling backtracked to 23.6 from 24.2. But the big step back on the month is the retail sector which fell back to a reading of 5.1 in August from 11 in July. That retail back-step was huge; it has only made larger month-to-month drops 13% of the time historically. And it is quite odd for retailing to sour in a month when the rest of the economy is doing so well in both absolute terms and in terms of momentum. So while the whole of the report is quite impressive, the setback to retailing is real and sharp and also quite hard to explain. And it's the second large step back in a row for retailing. The two month drop in retailing has been exceeded only 16 times (0.5% of the time) since 1991. Retailing in Germany is having issues. Apparently car dealers are the segment most concerned about the outlook. Germany has been wrestling with several auto sector scandals one concentrating on mileage standard cheating in general and a second focusing on the efficacy of continuing to use diesel engines at all.

The overall assessment

The business situation actually slipped this month with its index falling back to 36.9 in August from 38.7 in July. Expectations, however, gained in August, rising to 12.6 from 11.4. It is quite extraordinary for the IFO reading to be so strong and to have expectations continue to ramp up. But that is the situation. The German economy is really doing well and expectations are for it to do even better.

Overview

With the economy doing so well in Germany, there is interest in what ECB President Mario Draghi will say in remarks at the Federal Reserve symposium on world growth being conducted in Jackson Hole, Wyoming. In remarks made just ahead of the Fed meeting, Mr. Draghi played out this well-worn theme of patience as he deemed the use of unconventional operating measures as largely successful. His take on these measures, however, is guarded. Draghi believes they are not fully understood and so making policy changes with theses sorts of program in force should be done carefully. This is a significant point as the ECB is widely expected to be ready to pull back some of its special stimulus programs soon and the Federal Reserve is preparing to shrink its enlarged balance sheet, having said it is ready to do it but not yet having announced a date for it. Markets are waiting for any sort of news on these topics out of - of all places - Wyoming, the 'Wild West,' Yippie yi yo kayah! (for those who need it, translation/context here).

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief