Global| Mar 25 2020

Global| Mar 25 2020IFO Plunges

Summary

German business sentiment logged its steepest fall ever recorded since German reunification. The IFO also released analysis saying that the German economy could contract by 20% because of actions taken to prevent the spread of the [...]

German business sentiment logged its steepest fall ever recorded since German reunification. The IFO also released analysis saying that the German economy could contract by 20% because of actions taken to prevent the spread of the coronavirus.

German business sentiment logged its steepest fall ever recorded since German reunification. The IFO also released analysis saying that the German economy could contract by 20% because of actions taken to prevent the spread of the coronavirus.

Lock-down and forecasting

The BBC reports that one-quarter of the world's population is under some form of lockdown. With the German economy so export-dependent, it is not surprising to see such draconian projections being bandied about. The bottom line is that no one really knows. Forecasting in this environment is simply an exercise in thinking about what might happen under different future scenarios. Handicapping which future scenario is most likely is a thankless and impossible job. Welcome to economics.

February vs. March

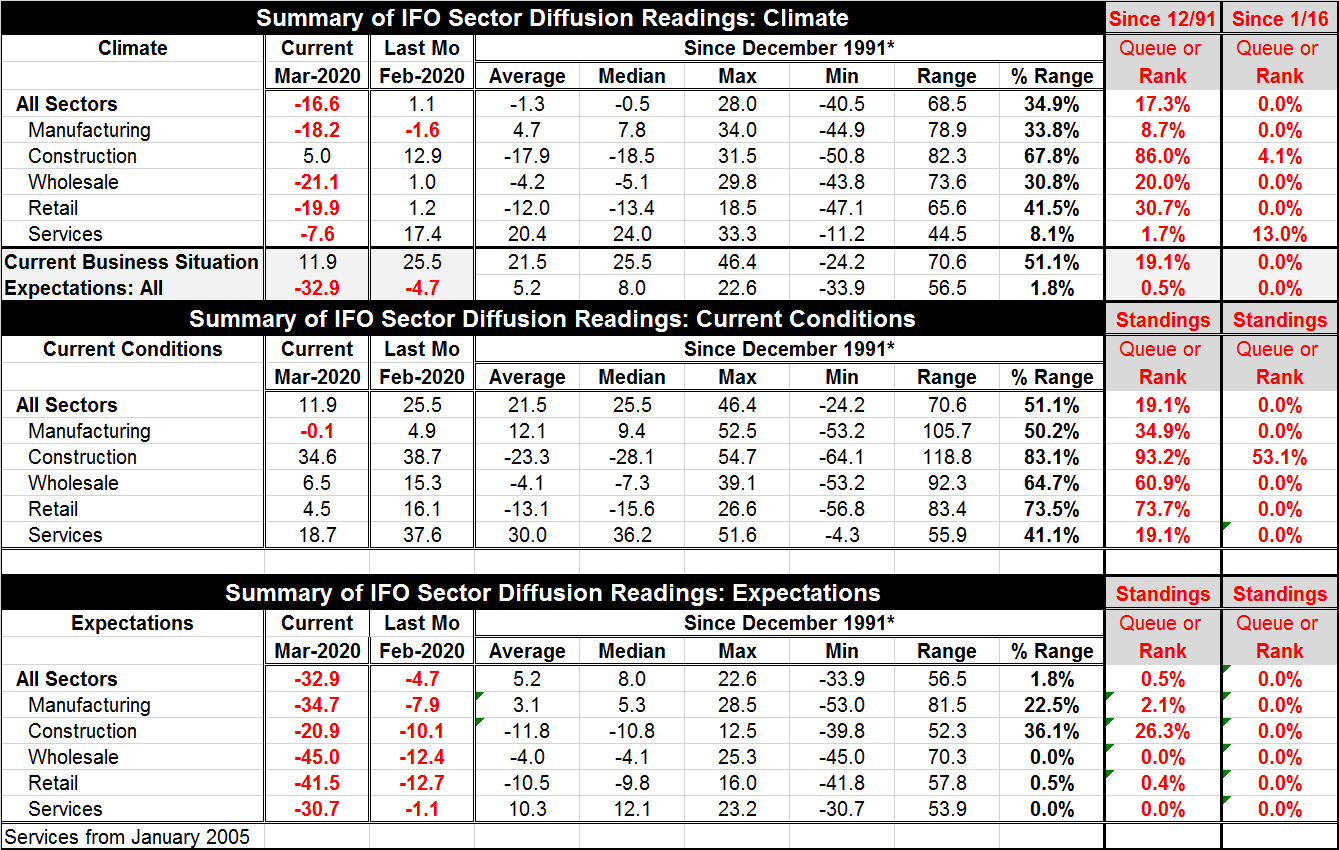

The IFO report shows a sudden collapse in economic conditions in March. This finding accords with Markit PMI data and with other incoming reports in other countries. Basically, data from February are simply to be viewed as one-off. The British CBI retail sales report today dismissed itself knowing full well that next month with a lock-down in store, conditions would weaken greatly. The U.S. durable goods report showed a nice gain and some building momentum as of February, but that hardly reflects the ongoing reality either. Even March reports are flawed since they are the first month of what is going to be an extraordinary string of unusual economic reports.

The IFO in March

The IFO shows sharp drops in economic climate made up of sharp downgrades in current conditions as well as generally deeper mark downs of expectations that were already in the red. Ranked since early 2016, most of the standings are on their all-period lows this month - with very few exceptions. Ranked over the longer span since end 1991, rankings are higher; three sector rankings stand above their respective medians on that timeline (construction, wholesale and retail), but manufacturing and services are below median on their current gauges and everything is well below its long period median for expectations. Expectations are simply extremely weak readings across the board.

What's next?

The real question is what's next and what does this mean. With one quarter of the world's population in some sort of lock down, whatever number you put on the future it is going to be a low one. Picking the inflection point for 'all this' to end and for recovery to set in is yet another opportunity for forecasters to disgrace themselves.

Already 'camps' are forming... In the U.S., Donald Trump and some Republicans are becoming advocates of an early end to the lockdown calling the cure 'worse than the disease.' I must admit I have a great deal of sympathy for this view. Taking a general lockdown and transforming it to a targeted lockdown focused on at risk groups, people with preexisting conditions and older people, would seem to apply the action where it is needed and limit externalities. Other economic agents could go 'about their different businesses' and still take caution to retard the spread of the disease which, once the at-risk groups are accounted for, is little more than the risk of flu-like symptoms to the remaining population. However, in Europe there are strong advocates for remaining hunkered down until there is a vaccine to eradicate it. I simply do not understand the 'need' for that much caution once the at-risk categories are dealt with.

One point to bear in mind is that the kinds economic destruction created by a broad prolonged lock-down would greatly damage Western economies and destroy many peoples' lives and careers. There would be a separate wave of problems induced by these policies including psychological problems for job losers, suicides and other risks. In short, the draconian lockdown strategy preferred by health-care officials would create even more health-care problems and do so among that larger group of people who are only at risk of getting flu-like symptoms. Does that seem like a wise choice?

Does science rule or drool (hint it's a little of both)

The media is already stacking this up as a clash of Trump vs. Science. But I hope we can all see beyond that. Science has not done a good job here in a lot of places. In some places it was interfered with by politics (China), but in other cases it was tripped up by its own biases and practices (USA). Sometimes science, too, needs to learn. In the U.S., Trump closed borders early against medical advice; that decision helped protect the U.S. from infection that was spreading faster than health officials knew. Trump left policy in the U.S. to the CDC (Center for Disease Control). CDC would not accept test kits offered from abroad preferring its own standards and protocols to be met. In the event, this was a costly decision that CDC made on its own. As a result, test kit development in the U.S. was impaired. The first kits did not work. Then because CDC did not believe in widespread testing because testing itself might cause a panic, ramping up testing capacity was not a priority. It has since emerged that countries that tested aggressively have had the best containment results (South Korea vs. Italy is the prime example). That is all 'science' folks. So there is science and there is 'science.' And even scientists have gaps in their knowledge, biases and things to learn. I am a social scientist. My PhD is in economics. I do believe in science, but I also believe in understanding its limits and in collaboration. I do not believe in putting some 'scientist' on a pedestal because he/she has an opinion. I think intelligent people need to weigh the scientific evidence which we can trust and make decisions informed by the facts and advice of health professionals. What is needed is collaboration, not capitulation to a single view.

Caveat Emptor!

Health professionals cannot be responsible for putting policies in motion that will wreak the global economy for no good reason. Be careful of the advice that you are buying… Unless there is something about the coronavirus they are hiding from us, there is no reason for these lockdowns. Or to put it another way, there is an alternative strategy. There is a strong case to protect those classes of people who are most at risk. Protect them and then get on with it. Everything we do in our economic lives involves some risk, from flying in an airplane, to driving a car to working in factory and more. If one sets the risk tolerance to zero nothing gets done anywhere. To be at risk of flu symptoms is no reason to play fast and loose with the global economy where the stakes are even higher. If global or national economic conditions are impaired that could send out more severe shock waves of their own. This idea is not even triage. It does not condemn people to death in favor of growth. It just approaches the protection of at-risk groups differently and in a way that permits more flexibility.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief