Global| Nov 24 2020

Global| Nov 24 2020IFO Outlook Loses Momentum

Summary

The IFO climate index rose to a net value of 1.2 in November from 1.1 in October as current conditions weakened to a net of 5.1 form 5.9 and expectations weakened sharply to -8.1 from -1.4. As the virus impacts Germany, the current [...]

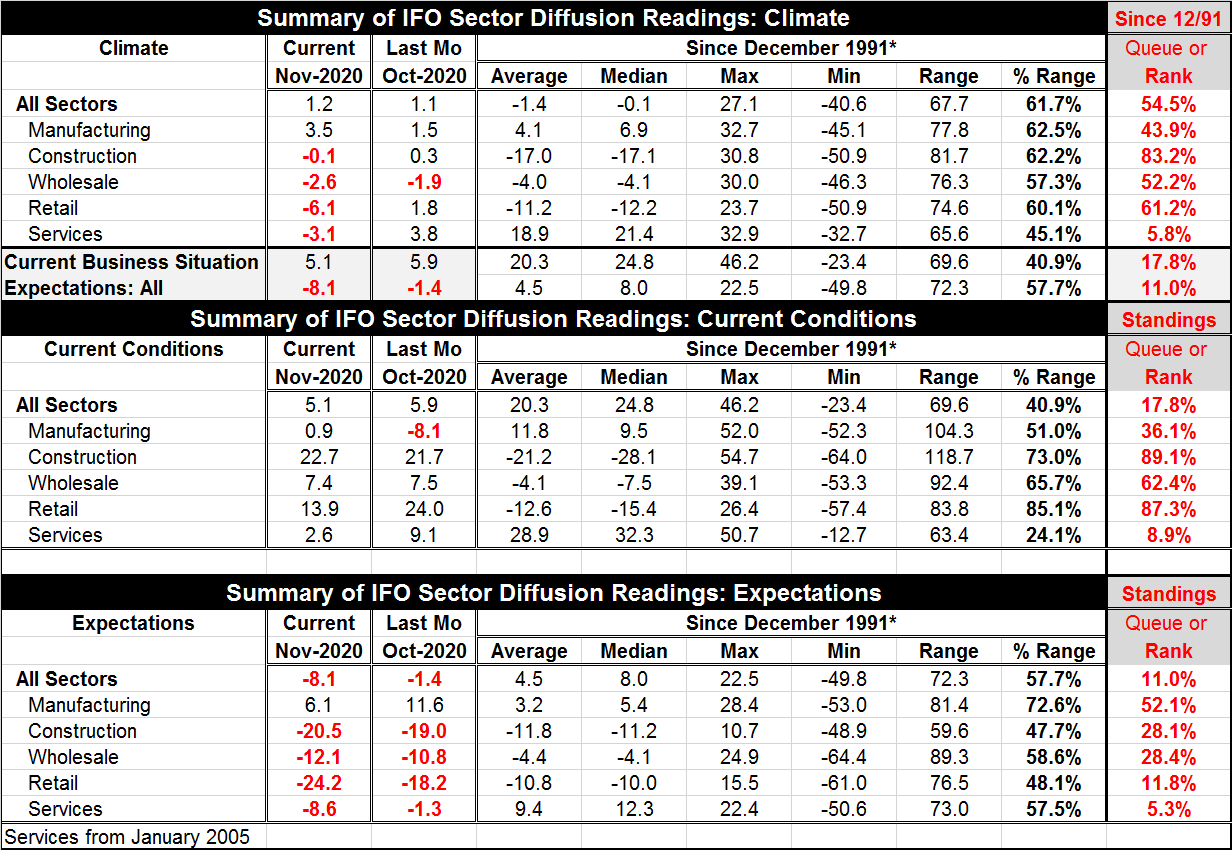

The IFO climate index rose to a net value of 1.2 in November from 1.1 in October as current conditions weakened to a net of 5.1 form 5.9 and expectations weakened sharply to -8.1 from -1.4. As the virus impacts Germany, the current situation and output are seeing setbacks.

The IFO climate index rose to a net value of 1.2 in November from 1.1 in October as current conditions weakened to a net of 5.1 form 5.9 and expectations weakened sharply to -8.1 from -1.4. As the virus impacts Germany, the current situation and output are seeing setbacks.

Rankings are weak

The climate index is the only index of the three that is above its historic median on data since late-1991. However, it barely goes over that hurdle with an all-sector ranking of 54.5% (the median is at 50%). For current conditions the all sector ranking is 17.8% and for expectations it is 11.0%. The latter two are well below their historic medians. The economy in Germany currently is not doing well and expectations are being cut sharply as the virus has spread and interfered with economic activity. Officials are warning of a sharp slowdown and of the potential for negative real GDP in the fourth quarter. What’s worse is that the German economy is heavily dependent on international trade and the rest of the world – especially the rest of the EMU- has been harder hit by the virus than Germany making the export path more challenging.

Sectors by ranking

The services sector that is the one requiring the most social contact is naturally the hardest hit of all sectors in terms of climate, current conditions and expectations.

• Services rank in the lower 10th percentile of their historic range in terms of each of these concepts. And services have weakened significantly month-to-month on each concept.

• At the other end of the spectrum, construction has rankings in its top 20th percentile except for expectations where the assessment is in its lower 28th percentile- its lower 30%. Construction deteriorated month-to-month in two of the three measures rising only modestly under current conditions.

• Manufacturing tends to be more insulted from special distancing rules, but it can be slammed by the virus if overall demand collapses. Manufacturing still has a low ranking except that under expectations it’s the only sector above its midpoint in ranking under expectations with a 52.1 percentile standing. Manufacturing climate and current conditions improved this month but its expectations reading fell sharply to 6.1 from 11.6 because of the recent virus spread and policy counteractions to contain it.

• Wholesaling and retailing have mostly mid-range standings above their medians in climate and current conditions. But each of these sectors is much weaker on their expectations assessment. Both sectors deteriorated month-to-month in all their October to November comparisons.

Summing up

The IFO shows that the German sectors do fall into categories of performance that can be for the most part rationalized by the impact of the virus on the various sectors. Services perform the worst. Wholesaling and retailing occupy a sort of weak middle ground. Construction work is often outside and usually done with less physical proximity and so it is less affected by all things virus. Manufacturing also is a sector less affected by the virus and is doing better in terms of raw readings except under expectations where this recent virus resurgence has undercut expectations for future performance. Also manufacturing had been hit hard by the virus initially as aggregate demand imploded and while it is making some monthly gains its rank standings are still behind other sectors except under expectations where ‘make-up’ gains are still expected. But the case for ‘make-up gains’ has been undercut this month by the spread of the virus in Germany and in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief