Global| Oct 25 2019

Global| Oct 25 2019IFO Is Mixed, GfK Is Weakening and the ECB Forecasters Are a Pessimistic Lot

Summary

On the whole, there is little changed in the IFO survey this month. As the headline reports, current conditions do weaken slightly month-to-month and expectations improve. The rankings that are done on a relatively short horizon to [...]

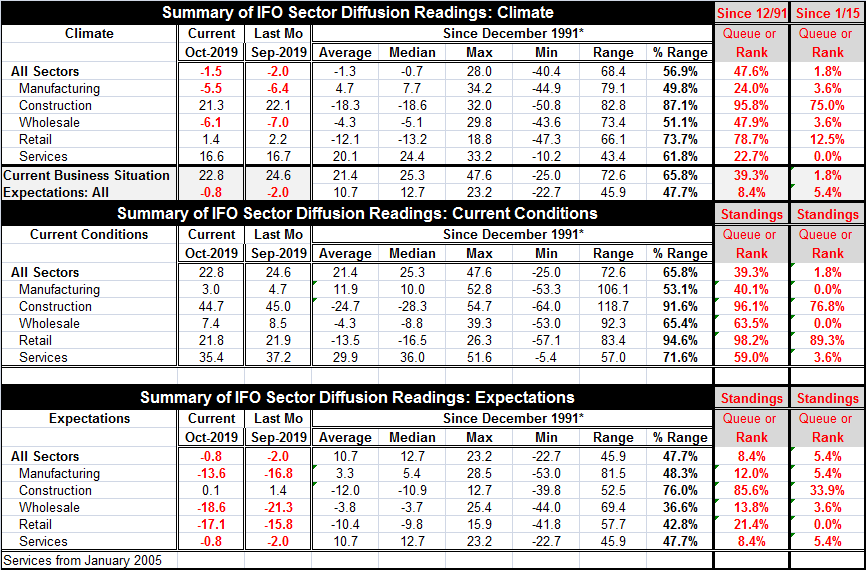

On the whole, there is little changed in the IFO survey this month. As the headline reports, current conditions do weaken slightly month-to-month and expectations improve. The rankings that are done on a relatively short horizon to match the availability of the Markit survey (from January 2015 on) and the longer survey (from December 1991) continue to report the same degrees of weakness that has been the hallmark of this report as the chart shows. On the long horizon, climate has a below-median rank, as it lies in its 47.6 percentile matched with a very weak 1.8 percentile rank since January 2015. The longer-period rank gives a more credible relative picture of where Germany stands. On the long ranking, manufacturing still has a very weak 24th percentile standing – a standing so low that it has been this low or lower only about 25% of the time since 1991. That is impressive weakness. And this month that metric improved a bit with manufacturing diffusion moving up to a net of -5.5 from -6.4 last month. In the last 21 months, this is only the third time manufacturing climate improved in a month-to-month reading.

On the whole, there is little changed in the IFO survey this month. As the headline reports, current conditions do weaken slightly month-to-month and expectations improve. The rankings that are done on a relatively short horizon to match the availability of the Markit survey (from January 2015 on) and the longer survey (from December 1991) continue to report the same degrees of weakness that has been the hallmark of this report as the chart shows. On the long horizon, climate has a below-median rank, as it lies in its 47.6 percentile matched with a very weak 1.8 percentile rank since January 2015. The longer-period rank gives a more credible relative picture of where Germany stands. On the long ranking, manufacturing still has a very weak 24th percentile standing – a standing so low that it has been this low or lower only about 25% of the time since 1991. That is impressive weakness. And this month that metric improved a bit with manufacturing diffusion moving up to a net of -5.5 from -6.4 last month. In the last 21 months, this is only the third time manufacturing climate improved in a month-to-month reading.

Manufacturing is typical of the sorts of changes we see this month with nothing major in the works in the way of change. Momentum is the most changed aspect of this report. Generally, there is a sense that the erosion has paused at least for the month. That much is apparent from looking at the graphic.

It continues to be true that the current situation is below its median while the expectations reading is in the lower 10th percentile of its historic queue of standings even on the long assessment. The weakness in the IFO is not just 'extreme weakness' when assessed on the short horizon from January 2015 forward but also a true deep weakness in expectations on a comparison with a longer time-series.

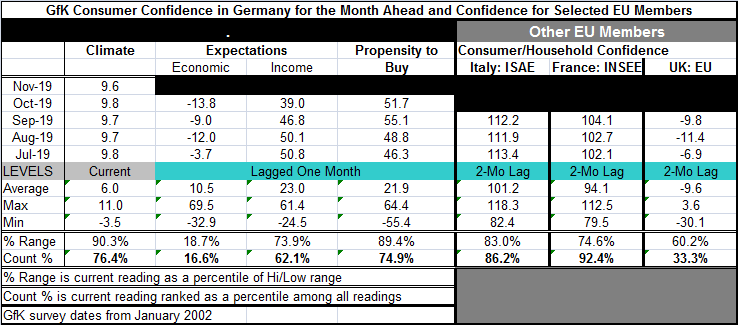

Germany also has a look-ahead consumer confidence measure from GfK that was released today. It projects confidence for November. It gives a reading that is two months ahead of the readings on confidence available for Italy, France and the United Kingdom. While this still a decent ranking for Germany (a 76.4 percentile standing), it is also the weakest reading on this metric in 43 months (3.5 years). And while confidence data availability for fellow European countries lags the German report, based on assessments that are two months older, Italy is at an 86th percentile standing and France at a 92nd percentile standing; they both have higher relative readings than Germany. The U.K., still battling its Brexit ghosts and realities, has only a 33rd percentile standing.

Of the three German confidence components in the table, the economic expectations have the worst standing at a 16.6 percentile reading. This is a weak standing for a metric that traces back to January 2002 and spans nearly 18 years. The message certainly reinforces the signals from the IFO that expectations are a real issue. German income expectations have a 62 percentile standing. That one is above its median for the period still only a lukewarm assessment. The propensity to buy component is the firmest reading at a 74.9 percentile standing. It is on the brink of its top 25th percentile. Consumer sentiment in Germany reached its top value in the second quarter of 2018 revisiting a peak level it saw briefly in 2017. Since then, there has been relatively steady ongoing erosion.

The German economy has its concerns. Apart from macroeconomic data, these concerns stem importantly from its slippage as a leader in the auto sector in the wake of the mileage scandals that gripped some German auto-makers. Not only has Germany lost its edge in the internal combustion sector, but the electric car is taking its place gradually. This is not a market where Germany is dominant. Moreover, electric cars have fewer parts in the drive train and their production will absorb fewer workers. German industry will have to find some new niches for workers as it moves ahead. Germany has some deep seated issues of competitiveness to deal with; its problems are not all Brexit, sanctions on key would-be customers, and trade war.

And the ECB professional forecasters think...Today the ECB Survey of Professional Forecasters (SPF) showed that inflation expectations for the euro area were cut to 1.2% for this year and next year from 1.3% and 1.4%, respectively. Some this revision was on the back of a new lower baseline for oil prices; however, core inflation for this year is still only projected at 1%, moving up to 1.2% in 2020 and to 1.3% in 2021 (“core” is the price index excluding energy, food, alcohol and tobacco). Since inflation is the sole focus of ECB policy and these forecasts post-date the new stimulus program the forecasts seem to imply that the stimulus has been needed (despite ongoing German unhappiness especially with negative rates). As for growth, this year's projection by the group fell to 1.1% from 1.2% with next year cut to a weaker 1% from 1.3%.

Survey respondents attribute weakness to the persistence of uncertainty related to Brexit and foreign trade in general according to the ECB report. That seems pretty thin gruel for forecasts that are poking three years into the future. Brexit is 'close' to being resolved. To be pessimistic, it will be resolved in the next 12 months. The U.S. and China are talking and have a first-phase-deal that appears to be about to be inked. In two or three years' time, uncertainty should be substantially less. I point this out not because I know how it will turn out but just to make it clear that conditions in two to three years should be charged with much less uncertainty. And if uncertainty is the main headwind, growth could come back into play much faster than these forecasts are now projecting. Or possibly these forecasters think that we will have 'never-ending Brexit' and 'never-ending trade wars.'

And consumer confidence is fading too...

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief