Global| Jun 22 2007

Global| Jun 22 2007IFO Index Drops to 107 from 108.6

Summary

Germany's IFO index fell sharply in June from 108.6 to 107. It stood at 108.6 for two months in a row and peaked in this cycle back in December 2006 at 108.7. No wonder the IFO says that levels are still high and that the economy is [...]

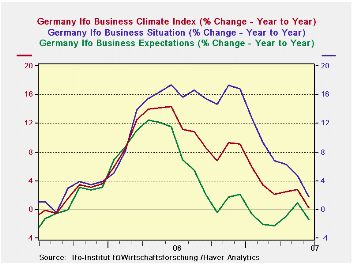

Germany's IFO index fell sharply in June from 108.6 to 107. It stood at 108.6 for two months in a row and peaked in this cycle back in December 2006 at 108.7. No wonder the IFO says that levels are still high and that the economy is still strong. But looked at another way, all this ebullience misses the point. The IFO survey has been weakening for some time. And here I refer to weakening in terms of its rate of growth. The IFO Climate headline hit a growth peak in June 2006, at just a tic higher than the pace it posted in November, a month before it hit its numeric peak for the index level. The index growth rate had been trapped in a narrow range around 16%. IFO growth had been strong and stayed in a narrow band from April to December of 2006. But, since then, the rate of growth has been dropping - sometimes sharply - as the chart above shows.

Both current conditions and expectations have lopped digits off their growth rates over this period. Expectations fell first dropping from a growth rate of 12.4% in April 2006 to below zero by October of the same year. Since April expectations growth has been waffling around the unchanged line. Current conditions growth, however, has continued to erode at a more or less steady pace. From March to May that erosion took a pause but in June current conditions are sharply lower again and the decline in the rate of growth is ‘back on’ track and has fallen to zero from over 14% in June of 2006.

The drop in the overall climate reading spreads across main sectors as the IFO sector diffusion readings tell us. Readings are still 'high valued’ as the percentage of range figures tell us at the far right of the table. Diffusion readings of climate peaked in April 2007; confidence peaked in December 2006, expectations peaked in March 2006. Still the month to month drop in June was sharp for most sectors; the decline in services was moderate.

And although IFO Chief Economist Gernot Nerb says he is not worried about exports and says that the export readings in the IFO survey are strong the truth is that those conditions have eroded dramatically across industry groups.

| CLIMATE Sum | Current | Last Mo | Since Jan 1991* | |||||

| Jun-07 | May-07 | average | Median | Max | Min | range | % range | |

| All Sectors | 13.2 | 16.3 | -8.8 | -9.5 | 16.6 | -30.6 | 47.2 | 92.8% |

| MFG | 23.9 | 27.5 | -1.1 | 0.3 | 27.5 | -35.5 | 63.0 | 94.3% |

| Construction | -16.0 | -14.6 | -29.2 | -32.2 | 0.3 | -50.7 | 51.0 | 68.0% |

| Wholesale | 14.3 | 18.3 | -14.8 | -16.5 | 23.3 | -39.6 | 62.9 | 85.7% |

| Retail | -5.0 | -3.2 | -14.8 | -14.8 | 25.3 | -40.3 | 65.6 | 53.8% |

| Services | 26.0 | 26.5 | 8.2 | 7.8 | 28.5 | -15.7 | 44.2 | 94.3% |

| * May 2001 for Services | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief