Global| Aug 25 2014

Global| Aug 25 2014Ifo Index Continues Its Descent as the Game of Sanctions Plays Out

Summary

Germany's Ifo climate index for August has fallen to 5.3 from 8.6 in July. The all-sector climate index is still relatively firm standing in nearly the 72nd percentile of its historic queue of ordered values. However, this standing [...]

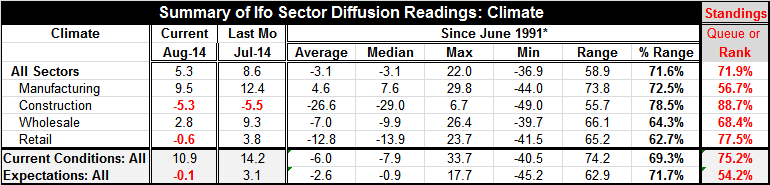

Germany's Ifo climate index for August has fallen to 5.3 from 8.6 in July. The all-sector climate index is still relatively firm standing in nearly the 72nd percentile of its historic queue of ordered values. However, this standing has been slipping steadily. The all-sector index has declined for four consecutive months from a level of 14.7 in April to a level of 5.3 in August. This four-month drop has been worse slightly less than 10% of the time, marking it as a period of substantial decline.

Germany's Ifo climate index for August has fallen to 5.3 from 8.6 in July. The all-sector climate index is still relatively firm standing in nearly the 72nd percentile of its historic queue of ordered values. However, this standing has been slipping steadily. The all-sector index has declined for four consecutive months from a level of 14.7 in April to a level of 5.3 in August. This four-month drop has been worse slightly less than 10% of the time, marking it as a period of substantial decline.

The manufacturing climate has fallen to 9.5 in August from July's level of 12.4. Manufacturing now stands only in its 56th percentile of its historic queue, marking it as just a slightly better than its median standing and as the weakest sector by standing. Manufacturing sector's four-month slippage has been worse than this 12% of the time, marking the slide as not quite as bad as for the overall index, but still substantial.

The construction sector continues to have an overall negative reading, but it actually improved slightly in August, rising to -5.3 from -5.5 in July. The construction sector, despite its weak absolute reading, stands in the 88th percentile of its historic queue and has the strongest relative standing among all the sectors.

Wholesaling fell sharply in August to a 2.8 reading from 9.3 in July. The standing of the sector has fallen to its 68 percentile, reducing substantially the strength of its reading for the past months. Wholesaling has fallen from a recent peak reading of 14.3 in April to 2.8 in August. The wholesaling sector has made a drop over the past four months that is worse historically only 7% of the time, marking this as a period of substantial relative weakness.

The retailing sector switches signs, falling from a 3.8 reading in July to a -0.6 reading in August. Even so, retailing has a historic queue standing in the 77th percentile, which is relatively firm. Retailing hit its peak five-months ago and has fallen from an 8.4 reading in March to the -0.6 reading in August. This is a relatively large five-month drop for retailing. It only sits in the 14th percentile of its historic queue. That still registers as a substantial slippage over five months.

Current conditions assessments have declined to a reading of 10.9 from 14.2 in July. This leaves the current conditions index in the 75th percentile of its historic queue, a relatively firm standing, although still the envy of most European Monetary Union members. Expectations slipped to a -0.1 reading in August from a 3.1 reading in July, implying a queue standing in the 54th percentile just slightly above its historic median.

The drop in the current conditions index is weaker only 17% of the time, while the drop in the expectations index has been weaker about 20% of the time, implying that the aggregate declines in current conditions and expectations are more moderate than most of the setbacks in the sectors that we have seen. Still, these are substantial givebacks over the last five months.

Concerns have grown in Germany surrounding the continued aggressive behavior of Russia in Ukraine. Last week, in an action that came subsequent to this survey, the German convoy that was waiting to cross the border to deliver him humanitarian aid to the Ukraine insurgents stopped waiting for authorization and bolted across the border at a site of its choosing without getting authorization or the accompaniment of UN officials as had been agreed. It's widely believed that this convoy of inspected vehicles was joined by a group of uninspected vehicles carrying a cargo of military-related goods. Russia has continued aggressively to cross the border and is alleged to be firing artillery from Russia into Ukraine. Russia has just announced that it plans to send the second convoy to the area. All of this is subsequent to the deterioration that we see in the Ifo survey in Germany this month. The future still looks grim.

Just today Denmark announced that it is preparing to prune in its forecast based upon its trade with fellow EMU members that are themselves suffering a slowdown.

For the time being, Vladimir Putin's domestic ratings remain relatively strong. However, there are signs of food prices going up in Russia. Price rises as well as developing shortages could undermine his popularity in the months to come. For the time being, his response to sanctions has been to pretend to be a peacemaker, while actively undercutting the peace process everywhere possible, including supporting direct military incursions into Ukraine. On the mercantilist front, he has made sanitary allegations against Polish agricultural products to block their importation into Russia. And he has taken aggressive action against the US chain McDonald's alleging sudden sanitary concerns.

Given these reactions the possibility remains that economic impact on the West could worsen in months ahead, although conditions stand to worsen much more in Russia. Since Russia has a strong central government with a leader willing to impose his will on the economy, the odds are that the initial deleterious impact on Russia's economy will be played down and the adverse impact may only be seen after it reaches more catastrophic stages when even Putin's strong personality can no longer suppress the extent of the damage. If the standoff goes on that long, we have to wonder whether Putin will decide that he has less to lose by intensifying military action in Ukraine than by admitting he has lost in the game of sanctions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief