Global| Oct 26 2020

Global| Oct 26 2020IFO Expectations Back Off

Summary

The German IFO survey for October produced a gain of 1.4 points in overall 'Climate,' a progression of 5.9 points on its current all-sector index was logged as well as a decline of 0.7 on the all-sector index for expectations. For [...]

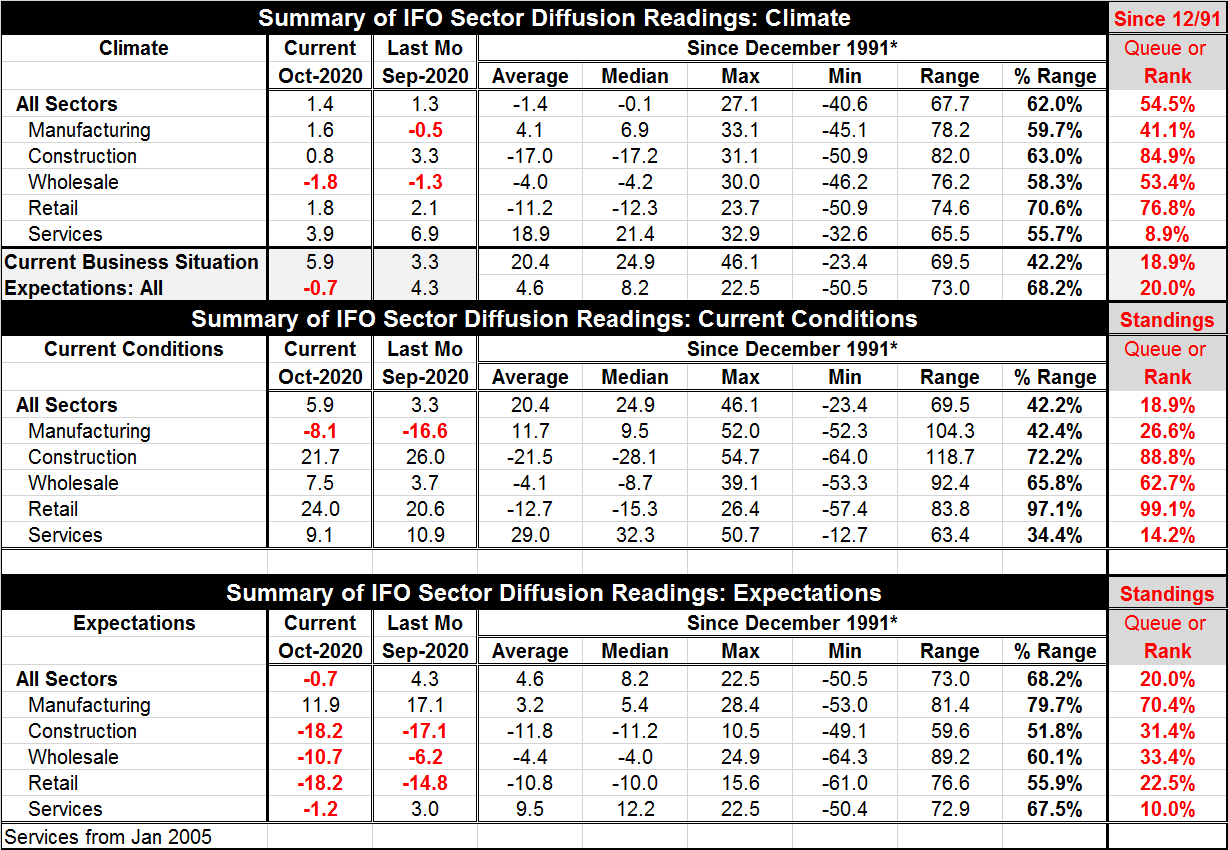

The German IFO survey for October produced a gain of 1.4 points in overall 'Climate,' a progression of 5.9 points on its current all-sector index was logged as well as a decline of 0.7 on the all-sector index for expectations. For expectations it was a small set back, but the first month-to-month step back following five months of advances. The back-off definitely is a signal about expected growth being scaled back. It comes as the virus is spreading rampantly across Europe and as the Bundesbank warns that the recovery is going to be more stretched out in the future. As we await some very strong news on QIII growth, various institutions are pointing out that the one quarter surge we anticipate is essentially a one-trick pony and will be followed by a very different sort of recovery process.

The German IFO survey for October produced a gain of 1.4 points in overall 'Climate,' a progression of 5.9 points on its current all-sector index was logged as well as a decline of 0.7 on the all-sector index for expectations. For expectations it was a small set back, but the first month-to-month step back following five months of advances. The back-off definitely is a signal about expected growth being scaled back. It comes as the virus is spreading rampantly across Europe and as the Bundesbank warns that the recovery is going to be more stretched out in the future. As we await some very strong news on QIII growth, various institutions are pointing out that the one quarter surge we anticipate is essentially a one-trick pony and will be followed by a very different sort of recovery process.

Ranked on data back to 1991, the all-sector climate reading has a 54.5 percentile standing, the current index has an 18.9 percentile standing and the expectations index has a 20.0 percentile standing. These are moderate-to-weak readings. For these standings' statistics, the historic median occurs at a ranking of 50%. Construction and retailing generally have the strongest standings on each of the three categories (Climate, Current and Expectations). Generally, these two sectors log standings in their respective 80th – 90th percentile ranges except for expectations where expectations for construction drop to the 31st percentile and retailing to the 22nd percentile but where expectations for manufacturing rise to the 70th percentile.

The main story this month is about how improvement in expectations has stopped and stepped backward. At the same time, the Bundesbank has announced that recovery is going to continue at a much slower pace. Analysts are looking for German GDP to make up more than half of the drop of the previous quarter in QIII alone. But thereafter the pace of recovery will be more circumspect the Bundesbank warns. And of course, there will also be the impact of the recent rise of infections because of the coronavirus that has to be accounted for. Expectations slid in each sector in October. Only manufacturing retains a net positive assessment and that corresponds to its 70th percentile standing. Still, the manufacturing index back tracked sharply in October, falling to 11.9 from September's 17.1.

Standings for current conditions are below their historic medians (below a ranking of 50%) for all sectors except construction, wholesale and retail. The weakness and weighting of the manufacturing and services sectors helps to drive the all sector index down to an 18.9 percentile standing.

We can also evaluate changes since the virus first hit by looking at changes in the IFO diffusion components since February of this year. On that basis, all the current assessments are lower on balance. The weighted average all-sector index is lower by 19.2 points. Manufacturing is lower by 12 points. Construction is lower by nearly 17 points. Wholesaling and retail are lower by about 7.5 points each. Services, however, is still weaker by some 28 points. This is the sector that has been hammered by social distancing requirements and continues to hold back the speed and degree of recovery.

Despite the fact that services have been so hard-hit, when we look at changes in expectations since February, we do not see much hint of faster rebound expectations for services ahead. The sector is moribund and expected to stay that way. Services expectations are weak in their lower 10 percentile and have improved by barely more than one half point from their February level. Manufacturing expectations rose 20 diffusion points above their January level while expectations in October are 2 points above their February level. Only construction and retailing expectations lag behind their levels of February. Harboring optimism about the substantial rise in manufacturing since February is sharply undercut by its five-point backtracking in October. The overall all-sector expectations index had a back-track of five points as well month-to-month in October.

On balance, we seem to be on some sort of odd inflection point. QIII data are posed to be released showing a jackrabbit recovery. But the month-to-month data show backtracking is already in progress. We know that the virus is back in gear and that many growth-inhibiting virus-slowing actions have been put in place across Europe where the spread is up and yet so far the death toll has not risen by much (It often lags but this time infections seem to have spread among the younger, healthier, population.).

It is not clear how long it will take Europe to get control of its outbreak. The U.S. now has joined Europe with a number of states seeing the outbreak spreading as the U.S. election date approaches. Sweden which is also seeing some rise in infections refuses to implement coercive polices to gain control. However, this week, it announced stricter local guidelines in Uppsala, a university town 45 miles north of Stockholm that has seen a spike in cases since students returned to school in the autumn. And locals have been advised to avoid public transport and in-person contact with people outside their own household until November 3. Sweden relies on advice not on requirements and most Swedes tend to follow advice. This is unlike other places where people might not even follow rules with penalties attached! Sweden still does not recommend face masks. In Sweden, it is thought that face masks give a false sense of security that undermines social distancing efforts that it deems more important. In America, people would have you believe that Donald Trump's opposition to face masks has caused thousands of deaths. The truth is there somewhere.

As the debate rages in the U.S. and as various groups take their own particular views as gospel we see Europe with many different approaches being used and various degrees of success. I think one thing we see here that is never acknowledged is that there are different cultures and depending on the national culture one approach might work better than another. There may not be a single approach that is 'the best' for everyone.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief