Global| Aug 25 2020

Global| Aug 25 2020IFO Continues to Improve After Jump; Some Good News and Lots of Reality

Summary

IFO headline The IFO business confidence index (we present data for the diffusion index below) rose for the fourth month in a row. It gained 11.1 points in May, 14.1 points in June, 9.6 points in July and this month it moved higher by [...]

IFO headline

IFO headline

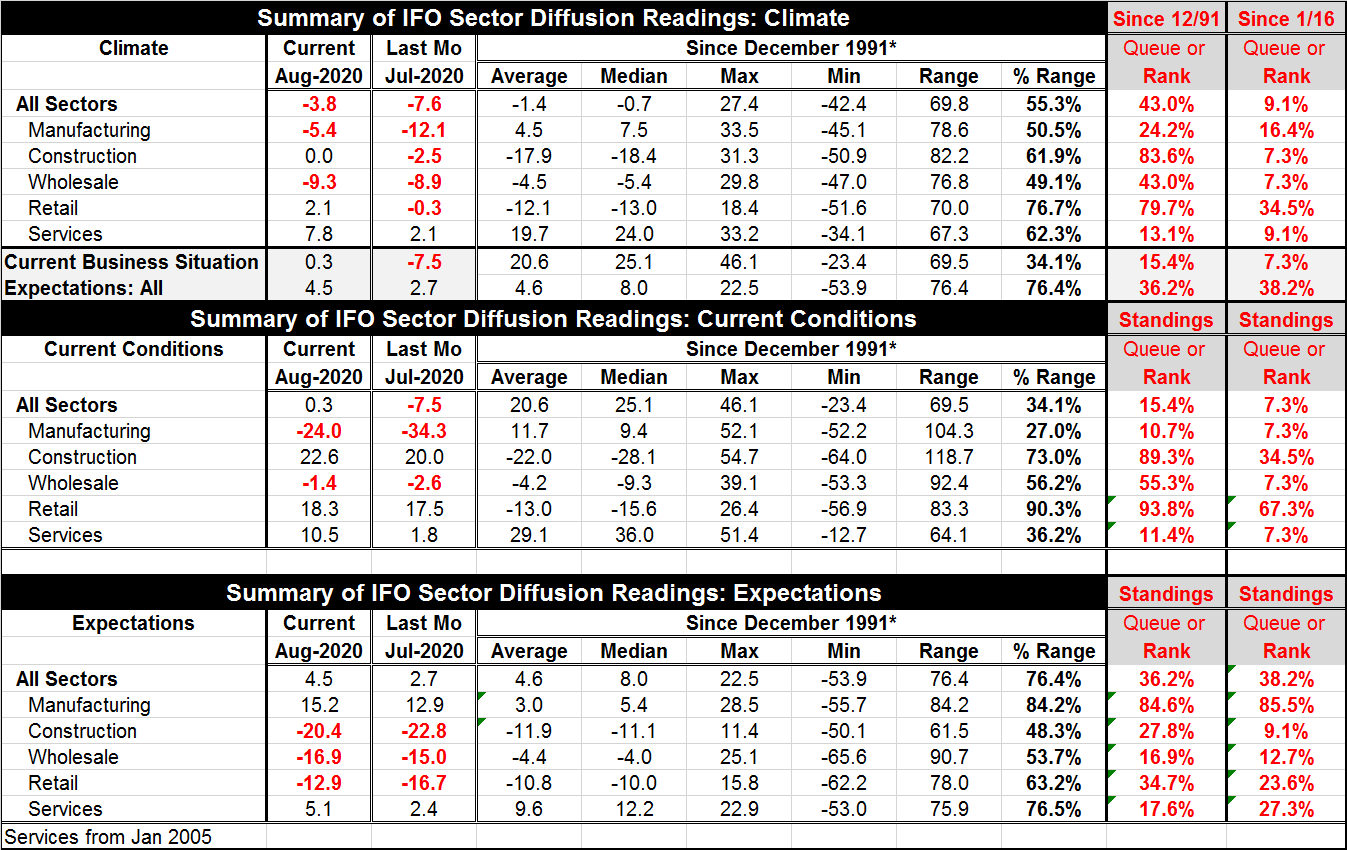

The IFO business confidence index (we present data for the diffusion index below) rose for the fourth month in a row. It gained 11.1 points in May, 14.1 points in June, 9.6 points in July and this month it moved higher by 3.8 points. The sprint to improvement is over, but the path of progress is still in place.

Recent changes in Current Conditions vs. Expectations

Most of the improvement has been in expectations. The current business situation index has improved for only three months in a row. It improved by 5.6 points in June, by 7.1 points in July, and by 7.8 points in August. The improvement profile of the current index has been more or less steady over these three months. In contrast, business expectations improved for four months in a row with a 22.8 point rise in May, a 32.2 point rise in June, a 10.6 point gain in July, and a much more gradual 2.3 point rise in August.

Quick IFO overview

The clear story told by this progression and structure of events is that progress remains in gear, but the jackrabbit has been replaced by a tortoise. Improvement in current conditions continues to be more or less steady. But expectations, which had dropped so sharply, then also rebounded sharply, have come to see their enthusiasm wane.

If there is a dark lining to silver cloud this month, it is that the slowing is occurring with still weak rank standings for expectations and that the present situation is advancing steadily but still slowly despite its extremely low ranking.

In the assessments below, I'll make reference to the longer time-series ranking since it has more gravitas. The more recent period is a time segment in which Germany was uncharacteristically strong on the IFO scale; that fact causes comparisons with the recent period to be lower than with the broader more representative historic norms.

Current situation

Let's start with the current situation. Its August reading has a ranking since 2019 in its 15.4 percentile and for the more current 2016-date period it is in its 7.3 percentile, both of them quite weak. Two current indexes continue to have negative readings as of August: manufacturing and wholesaling. The manufacturing rank standing is still weak, in its 10.7 percentile. For wholesaling, it's a standing of 55.3%. The retail standing at its 93.8 percentile is well above its longer periods median (which occurs at a ranking of 50%). Construction and retailing have strong standings on their timeseries comparisons at their respective 89.3 and 93.8 percentiles. The services long-term ranking is extremely low at its 11.4 percentile although its pick-up on the month was more robust at a gain of nearly ten diffusion points.

What it means

The long-term standings suggest strongly that Germany is being lifted by its consumer sector with the strong retail sector performance. Construction has been strong and that does not seem to have been undermined much by the virus, but it is small sector and will not drive the economy. Manufacturing and the part of the wholesale sector that feeds international trade look very weak and they are, of course, plugged into events largely out of the influence of German policy-making as globally growth has been weak. And services, the job-producing sector, is lagging.

Expectations

Expectations show better rankings overall and much less weakness across sectors as a rule. In contrast with the current index, the construction sector is much weaker on its expectation ranking, while manufacturing shows that hopes are very high for improvement there. Retailing with a very high current reading has a much more subdued outlook. Perhaps the dismal note in the expectations data is the weak standing for services that couples with a very weak current ranking since services is the jobs sector.

What it means

Jobs will be needed for recovery sustainability. Consumption in Europe is being held aloft by government intervention as in the U.S. While the U.S allows workers to become redundant and then supports them, in Germany whole firms are being propped up with the result that works receive their full package of benefits as an ongoing matter. This has aided consumption, but there must be a rotation away from government to the private sector. Bringing the service sector on board for recovery will be the key.

Upshot on the August IFO

The August IFO report should be regarded a report bearing good news. But the good news is still only what it is. There is no guarantee of a better future and no evidence of recovery gaining significant traction just a very slow slog that is continuing in a recovery that is very expensive for government to maintain. Can it keep moving forward? Well, a lot of that will depend on the virus. South Korea once considered a model country on how to contain the virus has lost significant control and is shutting down its schools in Seoul. In the U.S. after a period of the virus getting out of the tube and spreading, the toothpaste is being gradually shoved back into the tube with great effort. Many incidences of the virus spreading are now changing to a patch of receding. Yet, in the U.S. the August reading on consumer confidence in the backtracked showing an unexpected weakening. Is that significant or just episodic?

The way ahead

The virus and the policies required to contain it make economic policy-making a touch-and-go affair. Our ability to understand what is going on is impaired by various domestic elements across countries looking to ‘make hay' out of a government's perceived ‘failure' to contain the virus as well as ‘the next guy.' But what we are discovering it, that excellence in containment is hard even for those who once had success at it. The virus has a lot of moving parts and maybe no country really has it figured out completely. Because what we know about the virus depends on testing and some have tested more than others there is a quirk in which those that work the hardest at it may actually reveal statistics that make them appear to be doing worse. But this is not a case where ignorance is bliss - far from it. Ignorance is risk! Yet, no country knows as much as it wants to about its infection rates and where they may be percolating. And Sweden's model seems to have worked much better than expected as Sweden gets closer to having natural herd immunity (here), but even that is not without risk. It is foolish to think that we know what comes next. The virus has been a quite unpredictable wild card and as seasons change there could be more unpleasant surprised in store. Or maybe Covid-19 will do what MERS, SARS and Bird-flu did before it…just fade away without the use of a virus or anything else to combat it. The possibilities for covid-19 are simply too many for us to know what will happen next.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief