Global| Sep 18 2017

Global| Sep 18 2017HICP Gains 0.2% in August and Flies Under Target

Summary

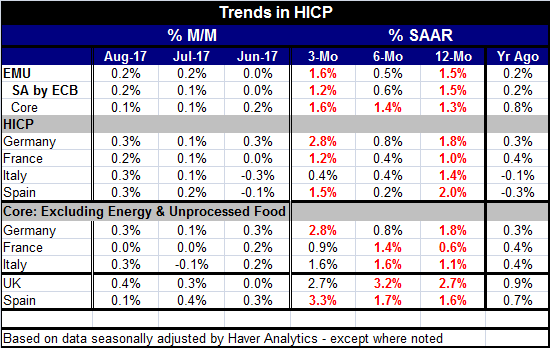

U.S. PCE and EMU HICP track similar trends Inflation continues to bedevil central banks. In the EMU, the latest harmonized index of consumer prices (HICP) runs at 1.5%, still below its target of a 'little less than 2%.' The core HICP [...]

U.S. PCE and EMU HICP track similar trends

U.S. PCE and EMU HICP track similar trends

Inflation continues to bedevil central banks. In the EMU, the latest harmonized index of consumer prices (HICP) runs at 1.5%, still below its target of a 'little less than 2%.' The core HICP rose by 0.1% in August and has gained 1.3% year-over-year. Core inflation in the EMU has not been above the 2% mark since December 2008. Eight and one-half years have passed since core inflation was 'too strong' in the EMU. Since December 2008, the last time core inflation was excessive, the core HICP has risen at an annual rate of about 1.2% - well short of its 2%-ish mandate. The ECB does think in terms of price level targeting, but it does not make policy from that respect explicitly. Its headline price level has generally been very close to the implied 2% ceiling over long periods. But since the financial crisis and great recession, the ECB has fallen well short of that goal for both the headline and core. The ECB, like the Fed, has a lot of leeway to let inflation run over the 2% target and still to be within its specified framework over the long haul. Of course, ECB policy does not approach the inflation rate this way. In fact, these days, it oddly seems to act more or less as if inflation were on a hair-trigger and no tick above target is to be tolerable. The ECB has been much more tolerant of inflation undershoots than overshoots. And this asymmetry is one of the reasons that growth is held back. Because hard money members dominate the ECB having inflation short of target has been much more allowable than to have it over target. And even though under Mario Draghi the ECB eventually did manage to take some extraordinary efforts to use monetary stimulus, these efforts were stifled and fought every step of the way with the result that by the time policies were implemented they were much less effective than they might have been.

Toothpaste and the tube

The ECB like the Fed in the U.S. still does not have a plan to achieve its inflation goal and instead it is making plans to ease off on the stimulus. The idea is that doing nothing or being only mildly more restrictive is still consistent with hitting the inflation goal. That is an idea with no empirical support. It is an idea borne of extreme ideology. Despite the big head start the central bank has in keeping inflation to its mark on its timeline, the ECB is fighting to keep the toothpaste in the tube even though no one is squeezing it.

Inflation conundrum?

The BIS this week spoke of the lack if inflation as a conundrum. Let me argue that what is happening to inflation is more an international trade and technology set of events than a problem with new and heretofore unseen macroeconomic processes.

Price vigilantes

I think that there is very little that is different in how the economy works, but there are distinct differences in emphasis and new channels that dominate cause and effect. For one, the U.S. and Europe are no longer as important places to produce things. The U.S. especially and Europe are more places to consume things than to produce things although Europe still has a current account surplus. Asia has a variety of economies geared more to produce things than to consumer things. Current account surpluses are the norm in Asia. This is an important difference. Since firms in the U.S. and Europe know they are not the low cost producers firms, there are very vigilant on prices. Every consumer has a price checker on his or her person when they shop. We call it a cell phone. As a result, we have an economy built on price vigilantism. Both producers and consumers are participants. It is not irrational and I do not believe it is any sort of a conundrum except to economists who are not open-minded about how the economy has changed. However, the basic economic mechanisms are the same. But what has lambasted the inflation rate is the 'sudden' introduction of the massive low cost producers in Asia. And along with that, there is the Asian bias to create output over ramping up consumption. Not only are Asian wages lower, but Asian savings rates are higher. To the extent, a dollar's worth of output is shifted to Asia the global multiplier for growth is made lower.

Low begets lower

To my way of thinking, inflation is low in the U.S., the EMU and elsewhere because of the low production costs and prices from overseas. The 'knock on' effects to the local U.S. and EMU markets are to keep all businesses there on notice to keep prices low. In a low-price high price-competition environment where foreigner producers are gobbling up most of the growth on the margin, there is little choice but for surviving firms to engage in price discipline. This dynamic permeates the system because even service sector firms are drawn in since goods sector companies buy from them and they must keep costs down. Wages are kept down to keep prices down. In turn that reduces the ability of consumers to spend, making them unwilling participants in this same game. Consumers become price vigilantes and that sends the game back to the cost vigilantes. And none of this has anything to do with monetary policy per se. And the monetary authorities still think that their actions are responsible for price behavior. But they have been unable to affect those conditions. And there is no sense in any of this that their actions are going to be the critical determinants of prices in the future. But this is their hubris and their inability to grasp the new economic framework will also be a factor. They may unwittingly make growth even weaker because of their fears. Their mandate is to act at least as if they control something that has moved beyond their grasp. That could make things very interesting in the months ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief