Global| Sep 16 2009

Global| Sep 16 2009HICP and Core Rate Are in Good Shape but Some Trends are Not

Summary

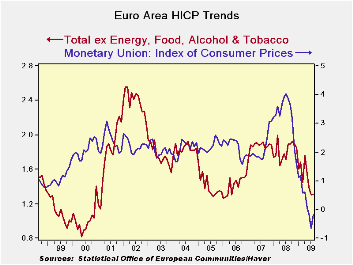

The EMU HICP finalized with August’s headline rate rising by 0.5% in and still dropping by 0.2% Yr/Yr. Core prices rose by 0.2% in August and rose by 1.2% Yr/Yr – a moderate result and indicating that inflation pressures are within [...]

The EMU HICP finalized with August’s headline rate rising by

0.5% in and still dropping by 0.2% Yr/Yr. Core prices rose by 0.2% in

August and rose by 1.2% Yr/Yr – a moderate result and indicating that

inflation pressures are within the ECB’s HICP ceiling constraint. With

headline inflation DOWN Yr/Yr the headline constraint is not going to

be an issue for a while. Keeping inflation below 2% will be easy. But

the core rate will provide better guidance as to what true inflation

trends are doing when the energy sector is not bashing the headline

rate hither and thither each month like a tennis ball caught in a long

rally.

So far the picture is still a good one. Goods sector inflation

is down by 1.5% Yr/Yr while service sector inflation is at 1.8% Yr/Yr.

Goods inflation is off in the recent three-months but service sector

inflation has locked in an increasing trend with six month inflation at

3.1% and three-month services inflation at 4.7%. That trend is a more

than a bit uncomfortable.

At the country level core inflation (excluding food, energy

and alcohol) is well behaved over twelve months with Germany France

Italy and Spain each with 12-month rates below 1.5%. But over the

shorter horizons things get dicey. Only Italy shows a core rate that is

not accelerating. There the core HICP is up by 0.7% over three-months

when annualized. For Germany, France and Spain core inflation has

accelerated to a pace of 1.6%, 1.4% and 1.9% respectively. Those are

uncomfortable results.

Europe remains a troubled economic zone, even as it is engaged

in the recovery process. Recovery is not instantaneous; those who are

displaced have to live through the process until they are re-engaged in

economic activity. And the weaker than expected IFO survey for Germany

has economists thinking that the EMU recovery will be slower rather

than faster. Still at such an early stage of recovery and with the

upswing still nascent, the ECB’s ceiling for headline inflation at 2%

implies a lot of room for discretion but the core rates are doing

things that are troublesome and testing that flexibility. It will be

interesting to see how the ECB handles this delicate proposition. At

least it has a rising exchange rate to help fend of any imported

inflation. With the headline rate under wraps The ECB does have some

time, but when nettlesome inflation trends are present the ECB has not

been known for its patience. Yet the currency is so strong that the ECB

probably does not want to signal that it is closer to the upside of the

cycle for interest rates. The ECB has a dilemma in the making. Core

inflation trends yet could evaporate. But unless they do the ECB is on

a collision course with some hard and unpopular decisions.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Aug-09 | Jul-09 | Jun-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU | 0.5% | -0.3% | 0.3% | 2.0% | 0.6% | -0.2% | 3.8% |

| Core | 0.2% | 0.0% | 0.1% | 1.5% | 1.4% | 1.2% | 2.6% |

| Goods | 0.4% | -1.7% | 0.2% | -4.1% | 0.1% | -1.5% | 4.6% |

| Services | 0.2% | 0.8% | 0.1% | 4.7% | 3.1% | 1.8% | 2.7% |

| HICP | |||||||

| Germany | 0.7% | -0.5% | 0.5% | 2.6% | 0.6% | -0.1% | 3.3% |

| France | 0.5% | -0.1% | 0.2% | 2.4% | 0.6% | -0.2% | 3.5% |

| Italy | 0.5% | -0.6% | 0.3% | 0.7% | 0.9% | 0.1% | 4.2% |

| Spain | 0.7% | 0.1% | 0.4% | 4.9% | 1.3% | -0.7% | 5.0% |

| Core excl Food Energy & Alcohol | |||||||

| Germany | 0.4% | 0.1% | 0.2% | 2.7% | 1.7% | 1.2% | 1.9% |

| France | 0.3% | 0.1% | 0.1% | 1.6% | 1.4% | 1.4% | 2.3% |

| Italy | 0.5% | -0.4% | 0.1% | 0.7% | 1.3% | 1.2% | 3.2% |

| Spain | 0.1% | 0.2% | 0.2% | 1.9% | 1.1% | 0.5% | 3.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief