Global| May 23 2008

Global| May 23 2008Here’s a Real FLASH: The Euro Area is Weak and Weakening

Summary

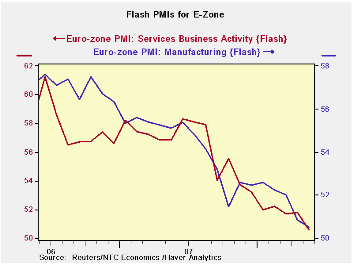

The chart is pretty clear. The table is pretty clear. The Euro Area is pretty certainly on a still-declining path - and that path is not showing any slowing. Growth is not contracting yet. But with the two main sector PMIs teetering [...]

The chart is pretty clear. The table is pretty clear. The Euro Area is pretty certainly on a still-declining path - and that path is not showing any slowing. Growth is not contracting yet. But with the two main sector PMIs teetering on the brink of a neutral ‘50’ reading ‘contraction’ isn’t just a word with an apostrophe. It’s a real threat.

The tabular data remind us that over this horizon both indexes are on their respective low readings for the period. A longer period of calculation for the MFG PMI shows it standing in the 43rd percentile of its range since mid-1997. The reading in May 2008 is at 96.1% of its average for the longer period. Put another way however, if we rank the various MFG readings we find that the current reading ranks 95th out of 132 observations back to mid 1997. That means in terms of ranking it is in the BOTTOM 28th percentile of all MFG readings of that time – a very weak result.

The history of the MFG survey is longer that for services. And while 28% isn’t as weak as 0%, it is a more powerful number since it is for a longer period of time when real weakness has visited the Euro Area. Lying firmly in the bottom third of its range, the MFG reading is not emitting signals that are very reassuring. The MFG PMI has been below 50 only 30 times. The last time was in June 2005 (a streak of three consecutive sub 50 readings). This month’s reading is the weakest since August of 2005, just after that streak. It’s a disturbing report for the Euro Area and possibly a warning about the future.

| FLASH Readings | ||

|---|---|---|

| NTC PMIs for the E-Zone-13 | ||

| MFG | Services | |

| May-08 | 50.52 | 50.59 |

| Apr-08 | 50.85 | 51.78 |

| Mar-08 | 52.01 | 51.69 |

| Feb-08 | 52.25 | 52.25 |

| Averages | ||

| 3-Mo | 51.13 | 51.35 |

| 6-Mo | 51.78 | 51.93 |

| 12-Mo | 52.70 | 54.10 |

| 24-Mo Range | ||

| High | 57.61 | 61.21 |

| Low | 50.52 | 50.59 |

| % Range | 0.0% | 0.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.