Global| Dec 01 2008

Global| Dec 01 2008Graceful but Painful Swan Dive in MFG PMI’s… Into an Empty Pool

Summary

The NTC final indices are now out and are weaker than their FLASH counterparts were. The percentile column on the far right seems due for an ‘out of order’ sign except that it is not out of order. The overall index as well as the [...]

The NTC final indices are now out and are weaker than their

FLASH counterparts were. The percentile column on the far right seems

due for an ‘out of order’ sign except that it is not out of order. The

overall index as well as the country components and the UK index are

all at lifetime lows- even for Germany an index that goes back to 1996

and for the UK that goes back to 1992. The drop off in MFG in Europe

has been very sharp and the authorities have been caught off guard.

They watched the troubles in the US unfold largely thinking that the

problems would not migrate over the ocean to such a great degree but of

course they have.

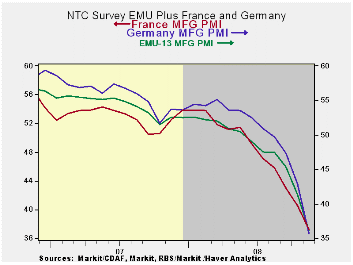

Germany’s MFG index stood at 49.68 barely indicating any

contraction as recently as August, just three short months ago. At that

time the EMU index had slipped to 47.55. Over three months the EMU MFG

index has dropped by 11.97 points compared to a drop of 14.02 points

for Germany. Over six months the EMU index is lower by 15.02 points

compared to a drop of 17.91 for Germany. But over 12-months the EMU

drop at 17.22 is very similar to Germany’s drop of 18.08 points.

Spain’s index has dropped by 21.31 points over 12-months and the UK, an

EU member nation, has seen its MFG index drop by 20.23 points over that

period.

In short, Europe is sliding very fast. The US PMI dropped by

11.5 points in 12 months though October compared to a drop of 10.42

points for EMU. So the US unravel has been a bit faster than Europe’s

–at least through October. The US MFG report for November will be out

later today. It would have to fall to 28.32 in order for the US MFG PMI

(ISM) to have the same point drop as the EMU index over the last

12-months (though November). To do that it would have to drop to a

level of 21.7. For now it appears that Europe has caught up to or

surpassed the US in the race to show which region’s MFG sector is

declining the most rapidly.

A dubious distinction…

| NTC/Markit MFG Indices | |||||||

|---|---|---|---|---|---|---|---|

| Nov-08 | Oct-08 | Sep-08 | 3-Mo | 6-Mo | 12-Mo | Percentile | |

| Euro Area 13 | 35.58 | 41.10 | 44.97 | 40.55 | 44.29 | 48.07 | 0.0% |

| Germany | 35.66 | 42.88 | 47.36 | 41.97 | 46.51 | 50.31 | 0.0% |

| France | 37.28 | 40.59 | 42.97 | 40.28 | 43.82 | 48.25 | 0.0% |

| Italy | 34.95 | 39.67 | 44.42 | 39.68 | 43.06 | 46.35 | 0.0% |

| Spain | 29.42 | 34.60 | 38.32 | 34.11 | 37.43 | 42.16 | 0.0% |

| Austria | 38.26 | 43.44 | 46.01 | 42.57 | 45.28 | 48.69 | 0.0% |

| Greece | 42.25 | 48.14 | 50.81 | 47.07 | 49.85 | 51.37 | 0.0% |

| Ireland | 37.10 | 39.69 | 43.70 | 40.16 | 42.25 | 44.59 | 0.0% |

| Netherlands | 38.71 | 45.28 | 48.30 | 44.10 | 46.86 | 49.72 | 0.0% |

| EU | |||||||

| UK | 34.36 | 40.70 | 40.80 | 38.62 | 41.78 | 46.23 | 0.0% |

| percentile is over range since March 2000 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief