Global| Mar 03 2016

Global| Mar 03 2016Globally Services Sector Implodes -Be Afraid; Are We Locked Up in a Prison of Ideology?

Summary

When I began to detect a slowdown in the U.S. and the global economy, I portrayed the final outcome as likely to be the result of a strong services sector vs. a weak manufacturing sector. So the final outcome would be the result of [...]

When I began to detect a slowdown in the U.S. and the global economy, I portrayed the final outcome as likely to be the result of a strong services sector vs. a weak manufacturing sector. So the final outcome would be the result of this tug-or-war winner. Manufacturing continues to be weaker than services - at on a head to head comparison of PMI values. Manufacturing has slipped to a lower level and has fallen faster than services- well at least until this month it has... But the services sector too has been eroding; while services still show expansion (PMI value above 50), the sense of erosion is palpable. And suddenly the drop in the global service sector index is substantial. Hey, where did that come from? Indeed, that is the point. Usually you do not see it coming. But I have been warning nevertheless.

When I began to detect a slowdown in the U.S. and the global economy, I portrayed the final outcome as likely to be the result of a strong services sector vs. a weak manufacturing sector. So the final outcome would be the result of this tug-or-war winner. Manufacturing continues to be weaker than services - at on a head to head comparison of PMI values. Manufacturing has slipped to a lower level and has fallen faster than services- well at least until this month it has... But the services sector too has been eroding; while services still show expansion (PMI value above 50), the sense of erosion is palpable. And suddenly the drop in the global service sector index is substantial. Hey, where did that come from? Indeed, that is the point. Usually you do not see it coming. But I have been warning nevertheless.

Is manufacturing's importance underrated? A U.S. example...

While a lot of economists and investors have been comforted by the bedtime story of a puny and unimportant manufacturing sector, that story has been nothing but a misleading fractured fairy tale. Manufacturing is an important sector and while its employment share is low, goods drive a lot of activity and the sector is much more important than just its employment share. There is a new piece of research (here) from the MAPI Foundation that uses input-output analysis to show the fully integrated impact of the manufacturing sector in the context of the U.S. economy. The report points out that there are some glaring deficiencies in categorizing of manufacturing in the U.S. NAICS framework. From the descriptions in this report, I assume foreign data will have at least some of the same sorts of drawbacks. But the report goes on to look at the full output and employment effects of bringing a manufacturing dollar's-worth of product to market. It finds a surprising substantial impact

David beats up Goliath again

Viewed in this way, the U.S. manufacturing footprint and multiplier rise sharply. It is still not fair to call these effects either `manufacturing' jobs or spending (they might be in some cases), but it is fair to call it a broader manufacturing sector impact. And this report helps to explain why the tiny-seeming manufacturing David is felling the service sector Goliath.

More weakness to come?

Manufacturing has an added feature (unlike services) that goods can be stockpiled (a phenomenon known as the accelerator model when it interacts with the economy) so that manufacturing excesses can be amplified. Services are more hand-to-mouth, but there is little focus on the fact that many services are things that people can and will do without when times get tight. In the U.S., I know some people who stopped filling their built in swimming pools to save on operating costs. Some will fire the lawn service and cut their own grass. Some will turn the ever dangerous to-do-it-yourself projects around the home-hello urgent care..

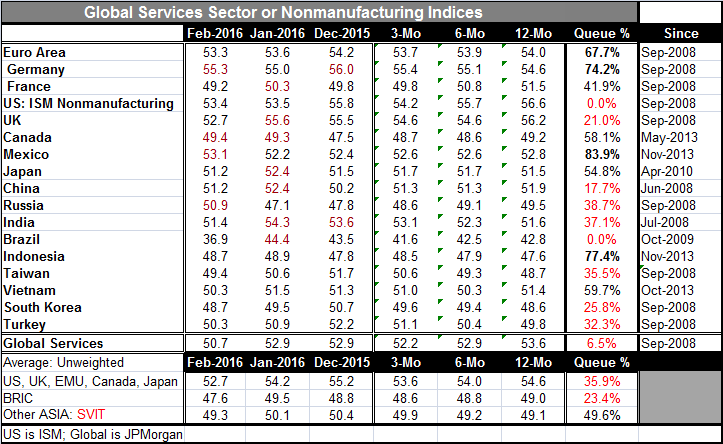

Services in February dropping like a rock

In any event we see the global services indicator dropping like a rock in February. In the U.S., the services indicator eroded slightly after a large drop in January. In our table of somewhat overlapping countries and regions (we have both the EMU and Germany and France separately as well as global services module), we have 18 mostly separate observations of which only four showed any service sector improvement month-to-month in February. In January, only seven had improved month-to-month. In December, only two had improved month-to-month. So this is a feature that has been in train. The weakening has been broad-based.

Nowhere to run, nowhere to hide

We now see contracting impulses in play for both goods and services sectors. Housing/construction is not likely to be much of an offset if any.

Levels of activity are low even if they still signal growth

As for the levels of these service sector indicators let's set aside the magical number of 50 after noting that 12 of 18 gauges are still above 50. Now let's ask what does that mean? If we rank the various service sector index standings in a queue of data over the last seven or so years, we get the result that only four countries/regions are above the 60th percentile of their historic queue of data. These will be the euro area, Germany, Mexico and Indonesia. On the other hand, 10 of 18 have percentile queue standings below their respective 40th percentiles of their historic queues. Five of these have readings below their respective 25th percentiles; these include the weakest standing on the period for the U.S. and Brazil as well as a lower 6.5% standing for all of global services. To clarify, global services since late 2008 have been this weak or weaker than this only 6.5% of the time.

China: can you hear me now?

Goods sector weakness continues to knock the heck out of global growth. China is seeing pullbacks in manufacturing and in services as it tries to shift gears-looks like the gear box froze up. Despite its pledge to the G20 that it had no policy of exchange rate weakness, immediately after the G20 meeting China cut bank reserve requirements setting loose more liquidity, then announced at 13% money growth target leaving plenty of room for prices to rise (and undermine exchange rate values) as the real growth `target' is `only' 7%.

Optimism? We don't have no stinking optimism

It is hard to be very upbeat on the global economy now. There is no fallback position with strength behind it. Oh yes, the services sector is expanding, but it is limping and its momentum is terrible. In the U.S., the nonmanufacturing ISM labor metric fell to a 24-month low, but the U.S. ADP survey continued to show 200K-plus growth in jobs per month in February. Europe also has continued to post solid job growth in the face of economic weakness. Still, you can see what the global services gauge did in February. I am concerned that job growth can do that too. One day it zooms ahead like the Roadrunner. The next day it is Wylie E Coyote falling off the plateau with and anvil close behind. Conditions can change very rapidly.

The oracle of ideology

In the U.S., the Fed does not have its guard up. It all seems tragic to me. We have learned so much about economics and yet we will put none of it in play. The world is being governed by anti-fiscal mentality and free-trade advocates are in denial as well. Fiscal policy would be so much more effective in this environment- most places. Beggar thy neighbor exchange rate policies are only stimulating the cheaters and pressuring the non-players. Exchange rates are vastly misaligned meaning we are not getting the `free-trade' results when global trade is expanded. The U.S. is in such a position with the dollar overvalued that fiscal spending probably would not work; all the stimulus would go out the back door abroad. Virtually no economists are weighing in on these issues. As a result, there is no consensus on what the problem is or on what the solution should be. Policymakers have fallen back on ideology. Why bother to study economics if you are going be a prisoner of ideology and never look at real life? Who will look at it with a fresh point of view?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief