Global| Nov 02 2015

Global| Nov 02 2015Globally Manufacturing PMIs Remain Lethargic

Summary

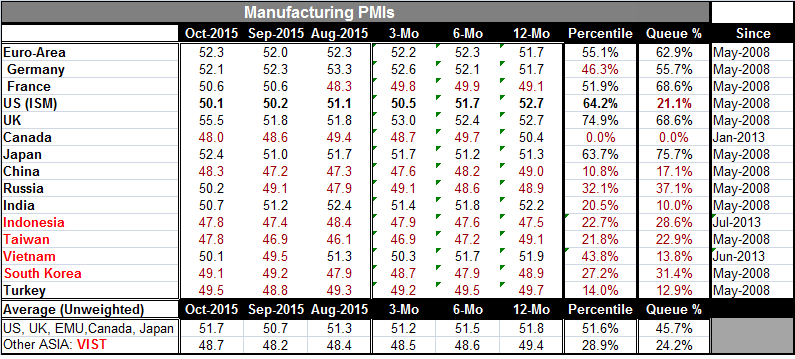

Manufacturing PMIs remains relatively weak. Note the percentile standings posted in the table and also note the period over which these are calculated. These are all comparative readings from the post-apocalyptic economy of the [...]

Manufacturing PMIs remains relatively weak. Note the percentile standings posted in the table and also note the period over which these are calculated. These are all comparative readings from the post-apocalyptic economy of the financial crisis/recession. These are not comparisons that include any observations for what times were good. So the relatively `firm' reading in the 75th percentile for Japan and 62nd percentile for the EMU region and the U.K.'s 68th percentile standings all are flawed examples comparing the bad with the worse.

Manufacturing PMIs remains relatively weak. Note the percentile standings posted in the table and also note the period over which these are calculated. These are all comparative readings from the post-apocalyptic economy of the financial crisis/recession. These are not comparisons that include any observations for what times were good. So the relatively `firm' reading in the 75th percentile for Japan and 62nd percentile for the EMU region and the U.K.'s 68th percentile standings all are flawed examples comparing the bad with the worse.

These readings are simply relative to a period where manufacturing already has been weak. Even so, the new miracle economy, India, has a manufacturing reading that stands in its 10th percentile. The old Asian miracle economies rank in their 31st percentile at best (South Korea) to the 13th percentile at worst (Vietnam).

While the China manufacturing PMI saw some pick-up in October, at 48.3, the index is still showing manufacturing contraction for the eight straight month. Its relative strength stands it in the 17.1 percentile of its historic queue of data, making it a very weak reading- weaker only about 17% of the time.

There are six of 15 readings below 50 in October with another four below a reading of 51. There are eight below 50 in September. Those that have `crossed over' to show growth in October have not done so in convincing fashion.

One theme here is how badly economies are doing despite a good deal of effort with monetary policy. The Fed, of course, has kept its monetary largesse about unchanged for about a year as it has pondered raising rates from emergency levels and beginning to withdraw stimulus. The Bank of England is more or less in the same position. The Bank of Japan has been waiting to see if it needs to do more after its initial slug of QE. In the EMU, European central bank President Mario Draghi has been saying that he is willing to do more if needed. Over this weekend he opined that further stimulus is an open question. While comments like that once gave markets a boost, thinking they meant more stimulus was coming, the cynics seem to have taken control and see commentary about more QE as a replacement for more QE. As an example, the euro firmed on Monday after Draghi made that comment over the weekend. That is not what you'd expect if markets thought the ECB was set to queue up more QE in December.

The manufacturing PMIs were a mixed lot in October in terms of changes. But in terms of levels, the assessment of weakness is unambiguous. Yet, the ECB is prevaricating on what to do next and the Fed is apparently hunting for bear and looking for scat as evidence it is looking in the right place- so far without success. While interest rates have been very low for very long, there have been periods in history when inflation stayed low. It is reasonable to ask if central bankers are applying the right monetary rules or not appreciating the stresses in play at this point in history. It is clear that the central bankers themselves are still grappling with this dilemma. They will make policy, but it may not be in unison.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief