Global| Dec 01 2015

Global| Dec 01 2015Globally Manufacturing PMIs Are Weak

Summary

November was a difficult month for global manufacturing. The PMIs from select countries in the table above show 14 countries and one area (EMU); among these, PMI gauges fell in six of them and two others were flat. That's bad news for [...]

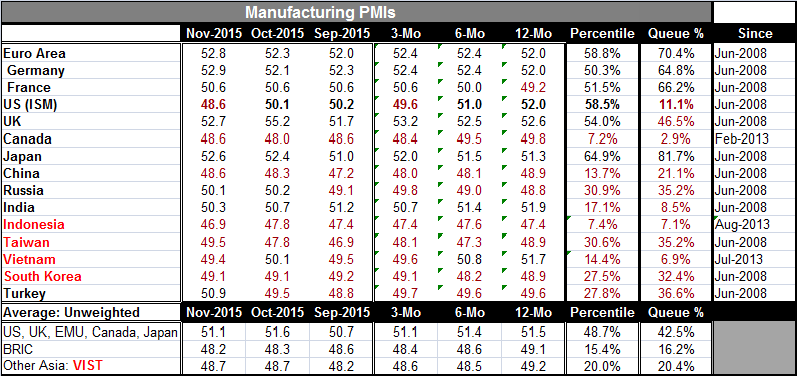

November was a difficult month for global manufacturing. The PMIs from select countries in the table above show 14 countries and one area (EMU); among these, PMI gauges fell in six of them and two others were flat. That's bad news for more than half of this sample. There was a strong gain of 1.7 points in Taiwan where the PMI index remained nonetheless below 50, signaling contraction.

November was a difficult month for global manufacturing. The PMIs from select countries in the table above show 14 countries and one area (EMU); among these, PMI gauges fell in six of them and two others were flat. That's bad news for more than half of this sample. There was a strong gain of 1.7 points in Taiwan where the PMI index remained nonetheless below 50, signaling contraction.

Among the 15 entities in the table above, seven have diffusion values below 50 indicating contraction in manufacturing activity. Four more have values less 51 indicating very weak expansion. The highest value in the table is a 52.9 diffusion value for Germany, followed by 52.8 for all of the EMU.

The queue percentile readings (Column: Queue %) place each of the raw diffusion values in their respective ordered queues of data expressing the position as a queue percentile standing. The highest queue percentile standing is in Japan at 81.7%. That is followed by the euro area at its 70th percentile and by France at its 66th percentile and so on. These queue standings deteriorate rapidly from something on the threshold of strong (Japan) to pronounced moderation (France). In fact, the bulk of these queue percentile standings are very weak. The median queue percentile standing is Taiwan which has a 35 percentile standing. The average standing is at the 37th percentile. Both readings are well below 50, which represents the median value in both series.

The simple average of the diffusion values is 50.5 showing a slim margin above 50, which for a diffusion index is the line of demarcation between expansion and contraction.

In addition, China, Russia, Indonesia, Taiwan, South Korea and Turkey each have their three-month, six-month and 12-month averages below 50 indicating ongoing contraction in manufacturing. Only Russia among these shows a steadily rising period average. Among countries showing more persistent expansion, France, the U.K, and Japan show a tendency toward improved growth. The EMU and Germany show three-month and six-month averages that have plateaued. Canada, the U.S., India, China, and Vietnam show a steady erosion in their manufacturing PMIs - and that is not a list to be ignored.

A number of international forecasting agencies have cut their respective outlooks for growth in 2016. Among major reserve currency central banks, only the Federal Reserve in the U.S. is contemplating a rate hike. The European Central Bank is on the verge of stepping up its QE stimulus, the Bank of Japan has made no changes to its QE program and the Bank of England has its QE on hold. All-in-all it is not a set of configurations by central banks that gives rise to the view that growth is about to bust out all over. And crude oil prices continue to behave as if they have a bigger downside.

Over the last five weeks, I have applied these same ranking operations to the weekly indicators of U.S. economic activity and - by a wide margin - U.S. economic indicators are losing momentum and below their average year-over-year gains posted since 2010. Yet, the Fed seems determined to press ahead with its rate hike. These are peculiar times. Risks are where they are; but they are fought only where policymakers see them. Remember the Maginot line?

Geopolitical risks have stepped up over the last month and world leaders can see the risks multiplying. Consumers have been very tight with their wallets in buying everything except autos and trucks. At least these sales have remained strong in the U.S. and Europe even if they have slowed in China. Unemployment in Europe has fallen to its lowest point since early 2012. But that does not make it low. There are signs of some progress being made. But there is still a lot of dislocation. Perhaps policymakers need to be reminded of the risk of backsliding at least as much as the risk of overheating. While economic recovery has been in train for a long time, it has been an enfeebled recovery and has not reached the goals that most recoveries reached in a much shorter period of time. It hardly has sowed the seeds of inflation. A good policy maker prepares his or her economy for the right risk. Do our central bankers and fiscal authorities have it right or are they setting the stage to make things worse? Is fiscal tightness and more monetary accommodation the right policy mix for Europe? Is less monetary accommodation the right policy for the U.S.? We are about to find out.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief