Global| Aug 23 2019

Global| Aug 23 2019Globally Inflation Sinks As Japan's Inflation Languishes

Summary

Globally, inflation pressures continue to diminish. In Japan, inflation is creeping along at 0.5% over 12 months and at 0.6% excluding food and energy. Since 2001, U.S., EMU and Japanese inflation rates have remain large below 2%. In [...]

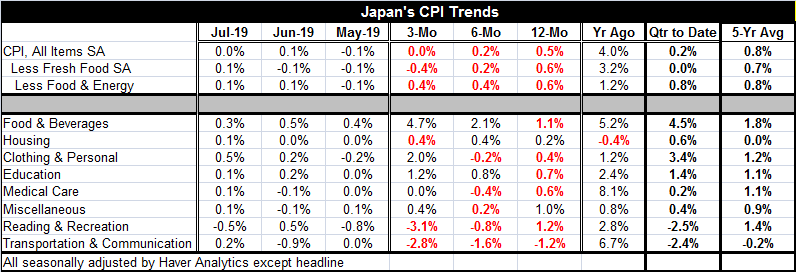

Globally, inflation pressures continue to diminish. In Japan, inflation is creeping along at 0.5% over 12 months and at 0.6% excluding food and energy. Since 2001, U.S., EMU and Japanese inflation rates have remain large below 2%. In Japan, the consumption tax hike boosted inflation for 12 months then it went back into hiding. The U.S. and EMU has seen only brief excursion of inflation over the 2% mark. Currently, inflation is declining in Japan, Europe, and the U.S. There are no inflation pressures to speak of. Globally, oil prices are weak and the strong dollar is pressuring dollar denominated commodity prices lower as well. The ongoing trade war is sapping the global economy of its vitality and that takes a toll on inflation as well. Japan is highly affected with its two main trading partners being China and the U.S., the two main trade war participants.

Globally, inflation pressures continue to diminish. In Japan, inflation is creeping along at 0.5% over 12 months and at 0.6% excluding food and energy. Since 2001, U.S., EMU and Japanese inflation rates have remain large below 2%. In Japan, the consumption tax hike boosted inflation for 12 months then it went back into hiding. The U.S. and EMU has seen only brief excursion of inflation over the 2% mark. Currently, inflation is declining in Japan, Europe, and the U.S. There are no inflation pressures to speak of. Globally, oil prices are weak and the strong dollar is pressuring dollar denominated commodity prices lower as well. The ongoing trade war is sapping the global economy of its vitality and that takes a toll on inflation as well. Japan is highly affected with its two main trading partners being China and the U.S., the two main trade war participants.

Central banks are powerless and speechless about what to do.

Japan and Europe already are running negative interest rates. The U.S. has room to cut rates and has begun to do that very methodically. Despite under-target inflation there and bond yields below the U.S. official 'Fed funds' rate across most of the maturity spectrum (across all of it for a while), the Fed has been reluctant to reduce rates in line with market movements and rate levels.

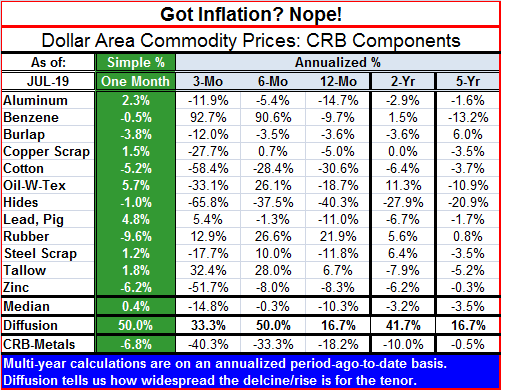

Global inflation pressures?? From oil? NO!

Global inflation pressures?? From oil? NO!

Globally at $17 trillion in fixed income assets bear negative yields. Arguably global monetary policy has met its limit. But the EMU policy summary shows that it sees a need for more stimulus and will craft a special program for that. The Bank of Japan is still watching market conditions. The U.S. is easing, but is it easing faster enough? Even where central banks have few options, their actions are being questioned. With rates so low, it seems to be a situation that calls more for fiscal stimulus. But in Japan, national debt is so high relative to GDP that fiscal stimulus is not about to happen. Japan is set to launch a hike in its national sales tax to try and get a grip on its massive national debt load. In Europe, Maastricht rules constrain many EU members from using fiscal stimulus. Germany has flexibility, but it is running a fiscal surplus. In the U.S., its long-term fiscal conditions plus political wrangling have hamstrung fiscal policy moves. In addition, arguing about the cyclical position and needs of the domestic economy also impedes U.S. policymaking.

What is a central banker supposed to do?

In Japan, inflation is tame, too tame. Headline inflation is up by 0.5% over 12 months and among its major CPI categories, only 'food and beverages,' 'miscellaneous' and 'reading & recreation' sectors have prices expanding by as much as 1% or more over 12 months. Inflation is about to be bounced higher by the coming consumption tax, but then it will go right back down. We have seen this after previous hikes in the consumption tax in Japan. The main point this year is to make sure that the consumption tax hike does not weaken the economy. But then what? Japan has no plan for raising inflation other than to wait and let its negative interest rate policy take effect.

China has just today slapped tariffs on $75 billion of U.S. exports to China in retaliation for the pending next round of U.S. tariffs on China. This move is not going to aid growth and despite the fact it is an import price-raising tariff, ultimately it does not pose an inflation risk either. What it portends is more economic weakness and that will result in less price pressure. The global economy is slowing. Central banks are losing or have has lost their grip on interest rates. Soon central bankers will become wholly reliant on balance sheet operations which have been shown to be much less effective than rate cutting. Central bankers likely need to shift their inflation targets lower or come to some understanding that they will not be meeting them for quite a while. However, they do not seem inclined to admit that. Lacking the guidance will leave central bank policies and policy realization sadly out of alignment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief