Global| Feb 03 2017

Global| Feb 03 2017Global Upswing Chronicled by PMI Gauges - Can It Last?

Summary

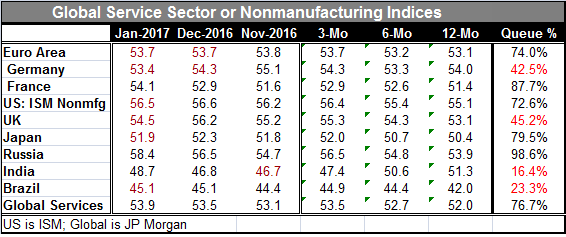

The global PMI services gauges show that both manufacturing and services are on an upswing globally. The global services sector has a 76th percentile standing. The global total PMI gauge had an 86th percentile standing in January. [...]

The global PMI services gauges show that both manufacturing and services are on an upswing globally. The global services sector has a 76th percentile standing. The global total PMI gauge had an 86th percentile standing in January. Global manufacturing has an 89th percentile standing on the timeline back to January 2011. All of these are good solid-to-strong readings and they are on improving trends.

The global PMI services gauges show that both manufacturing and services are on an upswing globally. The global services sector has a 76th percentile standing. The global total PMI gauge had an 86th percentile standing in January. Global manufacturing has an 89th percentile standing on the timeline back to January 2011. All of these are good solid-to-strong readings and they are on improving trends.

Germany does not appear as strong (in percentile standing terms) because it had been stronger more consistently earlier. As the chart above shows, global sector indices have had two serious swoons on this timeline, one of them in the wake of the Great Recession and the other started appearing around 2014 as Europe went through some serious difficulties to say nothing about China.

Because manufacturing has been under much pressure, the services sectors had to carry the burden of growth on a broad front. Eventually that became a heavy load and the services sector began to lose ground. However, recently manufacturing has been reviving and services are picking up right alongside it.

Country level results

Germany and the U.K. have sub-median readings for services on this timeline, but Brazil and India show much more serious weakness. Russia and France show exceptional relative strength; France does so on a relatively modest raw diffusion score, but it is showing strength relative to what has been common in this recovery. Russia is more explosively strong according to the survey. But I would have to call the Russian number quite surprising since the Russian economy has been under pressure with sanctions still in place. Putin has been rationing his public payments. While Russia did ramp up some oil production, it is now on the OPEC bandwagon and it is committed to production restraint. It is hard to understand how the Russian services sector is making an eight and one-half year high in this environment.

Japan is at its 79th percentile level, showing some solid behavior after a good deal of weakness. The U.S. shows a 72nd percentile standing and the EMU logs a 74th percentile standing. Of the nine reporting locales, six of them showed backtracking this month. Still, the JP Morgan overall services gauges still post a month-to-month increase.

Upswing in gear

On balance, we can see that some sort of upswing is in the making. At the same time, there is still some backtracking on the month. It is encouraging that both the manufacturing and services sectors are moving up together. Still, the global economy is not out of the woods. China is still in the midst of making its shift to more domestic sector consumption. In Japan, the Bank of Japan reported today that inflation expectations are back-tracking. Even in the face of oil prices going up, the BOJ is not able to sustain the belief that it can and will raise the rate of inflation there. Europe still has many challenges. While Germany wants rates to rise there, because of rising energy prices and headline inflation, ECB President Mario Draghi has said that oil is a transitory factor, does not affect the outlook for inflation and that he is going to ignore oil prices so long as they stay out of the rest of the sector inflation rates.

The U.S. as wild card

In the U.S., there is a new President who is stirring the pot geopolitically and on trade. So the U.S. right now has the rest of the world a bit scared especially because the President has said his policies are going to be oriented to put America First. While that may seem odd, "what else has the U.S. been doing?" you might ask. But U.S. policies have allowed other countries to exploit it on trade. The U.S. has run only three current account surpluses in the last 35 years and this has resulted in a loss of a great deal of wealth and it is emblematic of an economy that is no longer competitive. Donald Trump is focusing on the U.S. exchange rate and struggling to make clear that he does not want the dollar overly strong while his Treasury Secretary walks a thin line on that same subject. Basically, Trump has taken the gloves off on U.S. commercial policy and has really focused on Mexico (which is now reeling as a result of U.S. pressure). The U.S. is relying on commercial policy threats because one country cannot force all the others into currency reform. The simple fact is that the exchange rate system has been manipulated by U.S. trading partners to keep their exports flowing especially to the U.S. while U.S. exports have been stagnant and U.S. domestic investment has suffered. If there is one thing Trump means for the global economy, it is that the rest of the world will have to stand on its own a bit more especially when it comes to creating demand. The U.S. is no longer going to be handing out its domestic demand like a door prize at a bridal shower. Things have changed. There is a new sheriff in town law. Enforcement is going to be different.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief