Global| Oct 05 2015

Global| Oct 05 2015Global MFG Takes Another Step Back in September

Summary

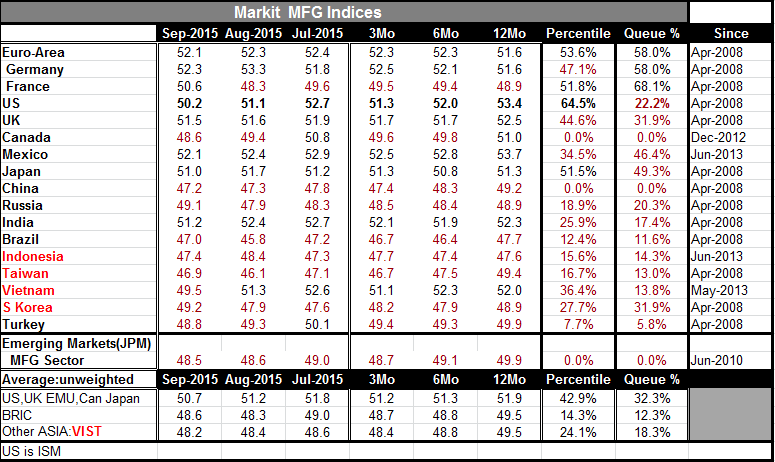

The Markit (and for the US, ISM) MFG PMI's largely weakened globally in September. There were readings below 50 in nine of the seventeen countries/units in the table. There were month to month declines in the MFG-PMI indices in 11 of [...]

The Markit (and for the US, ISM) MFG PMI's largely weakened globally in September. There were readings below 50 in nine of the seventeen countries/units in the table. There were month to month declines in the MFG-PMI indices in 11 of seventeen. Thus manufacturing readings are low and are generally moving lower.

The Markit (and for the US, ISM) MFG PMI's largely weakened globally in September. There were readings below 50 in nine of the seventeen countries/units in the table. There were month to month declines in the MFG-PMI indices in 11 of seventeen. Thus manufacturing readings are low and are generally moving lower.

To facilitate comparisons we use a history that goes back only to early 2008 or shorter for the newer respondents. But this is a set of readings for a period that the global economy has been depressed. It is all the more disappointing, therefore, that the queue standings are so weak. The queue standings rank each current indicator in the ordered queue of historic observations. The euro-area reading of 58% means that the euro-area readings are weaker 58% of the time and stronger only 42% of the time- a very moderate reading. Canada and China have readings at zero marking them as the lowest readings on this time horizon. Obviously that is not good.

The queue percentile column shows only three readings (for EMU, for France and for Germany) above the 50th percentile of their respective historic ranges. Among the underperforming countries Japan and Mexico are the closest to their 50th percentiles (which mark their historic medians; Japan 49.3% and Mexico 46.4%). But after that, the rankings are all very weak. Eight of 17 percentile standings are below their respective 20th percentiles. The U.S. stands only at its 22nd percentile; barely out of this group of weaklings.

Taken as a group the emerging economies are at their weakest point on this time-line. The BRICs are in their lower 12th percentile and a group of other Asian economies is at its 18th percentile. An unweighted group of developed economies consisting of the US, Canada, the UK, EMU and Japan has a 32 percentile standing.

The performance of the global economy is poor and trends are still not coalescing. In the Middle East Saudi Arabia is joining a price war to maintain market share by matching the price discounts offered by competitors. However, Russia has just suggested that it might be party to some agreement to limit output. That is having the larger impact on oil prices early today. Yet, the Russian offer may not be achievable because Russia is so at odds in its Middle Eastern policies by supporting Syria.

What is troubling about the onset of weakness is that it is encroaching on growth at a time that global monetary policy is still at full stimulus. Fed policy has been on hold for a while, but as the Fed likes to point out rates are still very low and its balance sheet is very large. The Fed thinks it can hike rates and still stake a claim to being very stimulative for a while longer. And we have similar largesse in play from the BOJ, the ECB and the BOE...and none of it is bearing fruit. That economic conditions could deteriorate with so much monetary stimulus in play is both surprising and disappointing.

One thing this lack of policy traction does suggest is that monetary stimulus is not the right medicine. Maybe, in the end, that is the argument for cutting back on it. Since excesses in monetary policy will at some point exact a price, if those excesses are not helping now, maybe they should be withdrawn. This, however, creates a problem for the central banks. The ECB and the BOJ are still using low rates and QE for stimulus. If the Fed reverses policy because those policies no longer work does that undermine the actions of those banks? Moreover, if the US exits those policies and others don't, there will be a toll taken on the dollar with further adverse consequences for the US economy. The Fed does not have a costless path by which to exit from its current policy tilt. And other central banks simply seem to be running ineffective policies. There is not much hope here as the MFG PMIs weaken further.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.