Global| Jun 01 2016

Global| Jun 01 2016Global Manufacturing PMIs Reveal Pronounced Weakness; Is It the Perfect Environment for a Fed Rate Hike or Not?

Summary

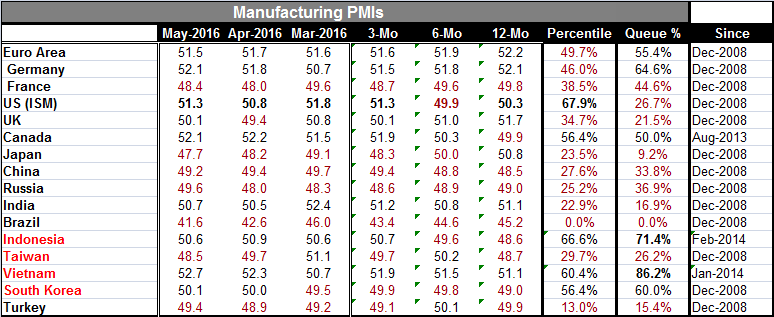

Lethargy and weakness rule Manufacturing PMI data remain weak on a global scale. Among the reporters in this table with data back to only 2008 at the most, there is NO country whose manufacturing PMI stands higher than Vietnam's 86th [...]

Lethargy and weakness rule

Lethargy and weakness rule

Manufacturing PMI data remain weak on a global scale. Among the reporters in this table with data back to only 2008 at the most, there is NO country whose manufacturing PMI stands higher than Vietnam's 86th percentile queue standing- and the Vietnam data extend back only to January 2014. The next best reading is for Indonesia with a 71st percentile standing on data that extend back only to February 2014. Ranked and positioned amid data back to 2008, there are 9 of 16 countries/areas with rankings below their 40th percentiles- in the bottom 40% or lower of their historic ranges. On data ranked back to 2008, only South Korea and Germany have manufacturing rankings in their 60th percentile range. For all of EMU, the ranking is in its 55th percentile. The global economy remains weak without positive leadership.

Japan

Japan reported a manufacturing PMI gauge of 47.7 for May, a 40-month low. Prime Minister Abe has finally officially thrown in the towel on the next round of consumption tax hikes for a time abandoning the fight for fiscal probity.

OECD

The OECD is making a plea for others to engage in fiscal spending to boost the global economy out of this low-growth trap. But as the OECD pleads it has not changed its forecast. It continues to look for 3% growth this year and 3.3% next year.

China

China's manufacturing PMI continues to hover below 50 in May. China's gauge was last above 50 in February 2015. However its 12-month, six-month and three-month averages show that China's PMI standing has been very gradually moving higher. There are six countries (France, Japan, China, Russian, South Korea, and Brazil) with readings below 50 for each time horizon and three others (Turkey, Indonesia, and Taiwan) that come close.

EMU

The euro area shows erosion is still in train. Its sequential averages show lower values on the shorter horizons. The same is true for EMU members Germany and France. The EMU remains under pressure in its manufacturing sector.

Asia

Asian economics with a large influence of China's economy show a great deal of weakness. While China itself does not show its weakness is worsening, it is lingering and that seems to cast a pall over much of Asia where China trade is so important.

Policy options: let's get fiscal?

The fresh calls from the OECD for fiscal stimulus will no doubt fall on deaf ears. Japan can scrap its planned consumption tax hike, but it is unlikely to launch much in the way of new fiscal stimulus. Policy is still largely hobbled by politics in the U.S. and will remain so at least through November and the elections. Germany continues to hold Europe's feet to the fire on Maastricht rules, putting fiscal action out of reach for most countries there. China, of course, is the exception and there the use of credit is absolutely chilling. The effectiveness of credit use is low as China is generating little growth per unit of credit compared to the way things used to work. China is playing a dangerous endgame, prolonging growth with credit can make the eventual restructuring worse.

Monetary policy: is it DOA (Dead on Arrival)?

We saw in yesterday's write-up that the ECB's action had not yet has any beneficial impact on year-over-year money and credit growth in the EMU. It seems that the black magic of monetary excess is no longer working its charms either.

Some editorial comments on why we are `here'

I will offer here only the briefest editorial comment on all these factual observations above.

Is anybody really surprised? Really?

China ramped up growth and displaced production in the West with no plan to boost its own consumption. This led to a huge shift of production to relatively high-saving low-pay China from the high-income high-wage free-spending West. It can hardly be surprising that this shift has led to global stagnation! What else could it have led to? There was no `free trade effect. There was no `mutually beneficial trade.' The West got cheap consumption and job displacement. Worker incomes have been depressed as a result of this production shift and global `multipliers' have been reduced. To think that the answer to this change in structure is more government spending is to ignore the growth depressing global structure that remains in place. For instance, if you fill your bucket with water then discover all the water has leaked out, the solution is not simply to fill your bucket again. It is to FIX THE LEAK.

What is...

China still produces too much at too low a wage and saves too much. The dollar is still too high and other currencies are too low. Although that configuration for currencies helps to boost U.S. spending power, it may not boost U.S. spending because it also makes the U.S. a very uncompetitive place and wards away goods sector job growth and investment. This pushes U.S. job and economic growth to the low productivity service sector and helps to produce economic stagnation. The too weak yuan does that to Europe as well.

What could be but isn't

Currency realignment meant to rebalance the structure of global output and consumption clearly is the most effective tool that could be applied here. But there is no global cooperation and this is no one's objective. The Fed in the U.S. has set its sights on INTEREST RATE NORMALCY and that will be done apparently even before the economy obtains conditions of economic normalcy and that will impact the exchange rate, keeping the dollar in this state of overvaluation.

So what will happen is that...

China is going to give up as little of its advantage as it can with financial capital trying to flee a country that has now so clearly been mismanaged economically, demographically and environmentally - despite what some well-known Western China-cheerleading economists have claimed. China is a mess and now it has become more militarily expansionist as it colonizes the South China Sea setting up military operations. But that is a `natural consequence' of bad economic conditions back home. It is a predictable effect that many political scientists are well aware of. Because China is so large, it is spreading malaise across the lands beyond its border. And the repercussions are much broader than just those in the South China Sea. China is not the only problem, but it is a big part of it and what it is doing is abusing an exchange rate system in the same way others have but to much greater impact because of its size. China's lesson to us all? Size matters.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief