Global| Jul 01 2019

Global| Jul 01 2019Global Manufacturing PMIs Continue to Get Whacked; Japan's Tankan Shows Stress

Summary

Manufacturing PMIs globally are weak and are weakening again. We feature a chart on China's manufacturing components since China is so much a part of this story with its involvement in a trade war. As of this month, China's [...]

Manufacturing PMIs globally are weak and are weakening again. We feature a chart on China's manufacturing components since China is so much a part of this story with its involvement in a trade war. As of this month, China's manufacturing is back in the soup. But on the back of the G20 meeting, President Trump and Premier Xi met and agreed to restart trade talks although we don't exactly know from which point they are restarting them. What has been gained is unknown. But what has been avoided is palpable. There is not another round of tariffs slapped on China and China will not be prodded to retaliate. So that much is good. And that is positive looking forward. Even so, where we are positioned in a global sense is still a difficult spot from which to operate.

Manufacturing PMIs globally are weak and are weakening again. We feature a chart on China's manufacturing components since China is so much a part of this story with its involvement in a trade war. As of this month, China's manufacturing is back in the soup. But on the back of the G20 meeting, President Trump and Premier Xi met and agreed to restart trade talks although we don't exactly know from which point they are restarting them. What has been gained is unknown. But what has been avoided is palpable. There is not another round of tariffs slapped on China and China will not be prodded to retaliate. So that much is good. And that is positive looking forward. Even so, where we are positioned in a global sense is still a difficult spot from which to operate.

Excluding France and Germany but counting the EMU as a unit, there are 14 economic areas (all countries except the EMU) listed in the table. Of these 14, only three saw manufacturing PMIs improvement in June. These three are Brazil, Vietnam and Turkey. And of the 14 manufacturing PMIs, nine of them show PMI values below 50 in June, indicating sector contraction. This is a severe condition across the countries/areas. And not only is the low end low and heavy with members, but the high side PMI reading this month is 52.5 in Vietnam followed by 52.1 in India and 51.7 in the United States. These are really weak for ‘high end' readings in June.

The average PMI of 12 months compared to 12 months ago shows improvement in only about 19% of the reporting units. Over six months compared to 12-months, there also are only about 19% showing improvement. But the average for three-months compared to six-months shows nearly 44% improving. And while that is still less than half, it is better than the proportion deteriorating on previous time lines. Still, these are data from averages. And as we see for the most recent month of June, there is another sharp fall-off in progress.

At the far right, the table gives us some rankings to position the current readings. It ranks the current PMI level on a timeline since January 2015. The ranking shows Brazil and Indonesia with rankings in their respective 60th percentile deciles. Vietnam, France and India have rankings in their respective 50th percentile deciles. All the rest are weaker with readings in their lower 20th percentile – lower than they have been for all but 20% of the time -or less- since January 2015.

The period from January 2015 was a time of some relative strength for Europe and the global economy, but what the percentiles affirm is how much slower things have gotten compared to how there were. And the number of PMI readings below the level of 50 also confirms that this is not just some garden variety of slowdown. There are some significant issues here. And putting the U.S.-China trade war on hold is not going to repair all of it. Maybe even solving the U.S.-China conflict will not be enough to keep growth on track.

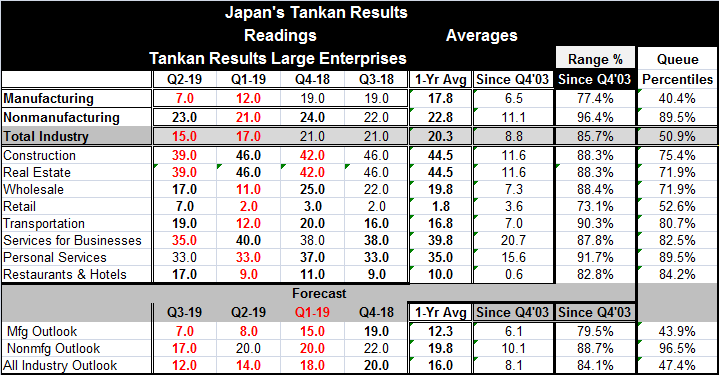

In addition to these weak readings, Japan released its quarterly Tankan report and important survey of firms. Large manufacturing firms tend to be used as the bellwether for this survey. Their reading for Q2 2019 fell to 7.0 from 12.0 in Q1 2019. That drops manufacturing firms to a 40.4 percentile standing compared to performance since Q3 2004, a level that is below its historic median. In addition, the raw net reading of 7.0 is below its 12-month average of 17.8

That drop puts downward pressure on the economy and the outlook and puts more strain on the backs on nonmanufacturing firms to maintain growth. In Q2 Japanese nonmanufacturing firms improved with a net reading of 23.0, up from 21.0 in Q1. That reading is slightly above its one-year average and has a queue standing in its 89.5 percentile.

The outlook portion of the survey, however, shows a drop off in both manufacturing and for nonmanufacturing firms. Both sectors also log Q3 2019 readings that are below their respective one year averages. Compared to historic outlook assessments, the manufacturing outlook stands in its 43.9 percentile, putting the outlook in relative terms in about the same standing as the current assessment. For nonmanufacturing firms, despite dropping, the outlook has a 96.5 percentile standing still a very strong view of the future compared to historic expectations.

On balance, Japan shows the signs of pressure from a weaker global economy and from the fact that it trades most intensely with the two warring trade countries China and the U.S.

Summing up

Beyond Japan and China the global economy show a lot of slowdown in place. One interesting exception was the unexpected report today that the EMU unemployment rate dropped to a 7-plus year low. Unemployment statistics continue to perform even in the face of what have been some very challenging manufacturing results. And these are for global players. One thing this points out is how little employment depends on manufacturing for job creating; having said that, I would not expect a severe manufacturing drop to be without its consequences. But so far, a quite identifiable manufacturing slowing globally has done relatively little damage to labor markets.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief