Global| Nov 18 2019

Global| Nov 18 2019Global Inflation Trends Remain Subdued

Summary

Globally inflation trends remain subdued. In the EMU and within the EMU, inflation is low and trends are moderating and pointing lower still. The EMU headline is slightly deflating and the core is mixed. Between trends for year-to- [...]

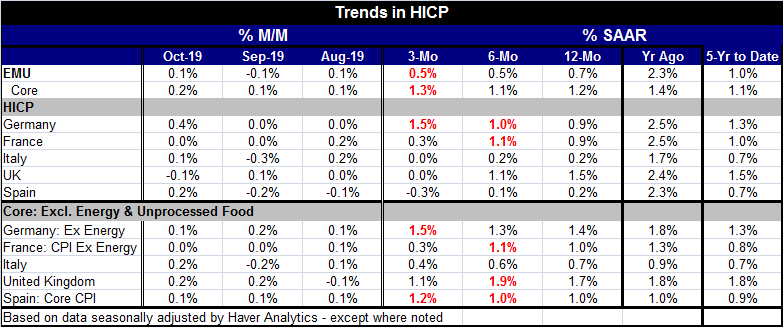

Globally inflation trends remain subdued. In the EMU and within the EMU, inflation is low and trends are moderating and pointing lower still. The EMU headline is slightly deflating and the core is mixed. Between trends for year-to-year vs. trends within one year headline and core trends are also mixed. Still, inflation's message is clear. After inflation stepped up a slight amount over one year ago, inflation is running low and well below its target. It was lower in and throughout the EMU from 2014 to 2016. That was after the collapse of oil prices globally. Currently, oil prices are undergoing a much more minor swoon and global activity is a downshifting mode in part because of the U.S.-China trade war. As activity globally has been decelerating, inflation pressure been abating and not just in Europe. Notice that for the EMU and its four largest members, as well as the U.K., headline inflation rates are generally below their five-year compounded pace while for core inflation the one-year pace is very close to its five-year average. This suggests that the weakness in oil prices has brought headline inflation down but has not had much impact on the core pace and that global weakness. Global weakness, to the extent it has been intensifying, has not had much impact on core inflation, at least not yet.

Globally inflation trends remain subdued. In the EMU and within the EMU, inflation is low and trends are moderating and pointing lower still. The EMU headline is slightly deflating and the core is mixed. Between trends for year-to-year vs. trends within one year headline and core trends are also mixed. Still, inflation's message is clear. After inflation stepped up a slight amount over one year ago, inflation is running low and well below its target. It was lower in and throughout the EMU from 2014 to 2016. That was after the collapse of oil prices globally. Currently, oil prices are undergoing a much more minor swoon and global activity is a downshifting mode in part because of the U.S.-China trade war. As activity globally has been decelerating, inflation pressure been abating and not just in Europe. Notice that for the EMU and its four largest members, as well as the U.K., headline inflation rates are generally below their five-year compounded pace while for core inflation the one-year pace is very close to its five-year average. This suggests that the weakness in oil prices has brought headline inflation down but has not had much impact on the core pace and that global weakness. Global weakness, to the extent it has been intensifying, has not had much impact on core inflation, at least not yet.

The U.S. has PCE headline and core inflation that are low (well below target) and inflation a bit less pressured lower than inflation in either Japan or in Europe. U.S. inflation appears to be more or less steady at a low sub-target pace. Meanwhile, growth in the U.S. has been stronger than in Europe or Japan perhaps accounting for the firmer tone in prices.

China shows very interesting mixed trends. China's CPI is accelerating as its PPI index is falling. As an economy designed more around the need to produce and to export than to consume, the weakness in the PPI is worrisome. To Chinese authorities, the weak PPI underlines manufacturing sector weakness. However, a falling PPI will further enhance Chinese competitiveness and bolster its ability to export if the global trade conditions allow it. The boost to China's CPI is largely because of rising food costs. China has had to kill large portions of its pig population to stop the spread of disease. This has caused food prices to rise. In response, China has lifted restrictions it had on U.S. poultry imports and portrayed that as more trade policy flexibility in the context of its trade war with the U.S. In fact, that was a move mostly to lower Chinese food prices.

China shows very interesting mixed trends. China's CPI is accelerating as its PPI index is falling. As an economy designed more around the need to produce and to export than to consume, the weakness in the PPI is worrisome. To Chinese authorities, the weak PPI underlines manufacturing sector weakness. However, a falling PPI will further enhance Chinese competitiveness and bolster its ability to export if the global trade conditions allow it. The boost to China's CPI is largely because of rising food costs. China has had to kill large portions of its pig population to stop the spread of disease. This has caused food prices to rise. In response, China has lifted restrictions it had on U.S. poultry imports and portrayed that as more trade policy flexibility in the context of its trade war with the U.S. In fact, that was a move mostly to lower Chinese food prices.

Oil prices have been on a roller coaster. They ramped up ahead of the Great recession and financial crisis then crashed, rose, over-shot equilibrium, and since have moderated. Fracking in the U.S., encouraged by the prerecession high in world oil prices, has brought new energy supplies to the fore. Meanwhile, using sanctions, the U.S. is trying to keep Iranian oil off of the world market. Despite this move, oil remains in substantial excess supply although at current price levels the profitability of fracking in the U.S. is marginal for a number of producers.

Oil prices have been on a roller coaster. They ramped up ahead of the Great recession and financial crisis then crashed, rose, over-shot equilibrium, and since have moderated. Fracking in the U.S., encouraged by the prerecession high in world oil prices, has brought new energy supplies to the fore. Meanwhile, using sanctions, the U.S. is trying to keep Iranian oil off of the world market. Despite this move, oil remains in substantial excess supply although at current price levels the profitability of fracking in the U.S. is marginal for a number of producers.

While oil has dominated the large inflation cycle swings, because there still seems to be a surplus of it - even in the face of Iranian mischief in the Gulf region - attention has shifted to the U.S.-China trade spat and the impact it has had on growth rates and therefore on inflation. As I argue above, in the European section, core inflation does not yet seem to be at all impacted by the ongoing economic slowing or trade war. But that could change. The global situation is really quite complicated with geopolitical risks of various sorts bubbling all over. The troublesome issues range from governmental instability or simply flux (the U.K., Italy, Lebanon…the U.S.? to name a few), to issues with migrants (the U.S., Europe, South and Central America), to old alliances under pressure (NATO) and to ongoing hot spots in the Middle East with protests rife in Iran and in Iraq as well some hugely divisive issues in China over Hong Kong and China's treatment of its Muslim minority. In fact, there are so many conditions in conflict and under stress; it is hard to know where the next real trouble spot might be. For example, U.S. and European pressure on China over Hong Kong has just prompted China to go on the offensive and to lash out against the U.S. for its behavior in the South China Sea that China has claimed and the U.S. and others dispute. Also in Asia, North Korea is looking less like Mr. Trump tamed it and more like it is done with its ‘peace process.' Meanwhile, the U.S. attempts to get South Korea to pay more for the U.S. troops kept there is running into resistance as has U.S. pressure to get Germany to pay more in NATO.

Who can tell?

The potential for economic or political instability to break down in dangerous ways is front and center. The U.S. and China have agreed that their various clashes are being kept on separate planes so that trade talks can occur while the two sides still trade barbs over treatment of China's Muslims, over Hong Kong, over the South China Sea and so on. That arrangement has been ‘stabilizing' for the trade talks, but it could also break down. There is a lot more risk in the wings than what markets have priced in simply because to do anything other than pretend that nothing will break down would probably be economically debilitating globally. It's not being done because it is the mostly likely scenario. It's just an expedient.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief