Global| May 06 2020

Global| May 06 2020Global Composite PMIs Take a Sudden Deep Dive

Summary

Once again the data demonstrate a sharp drop that has had no real prelude. February was a more or less normal month; then March and April saw collapse come out of the blue as the wheels went spinning off the wagons. These are the [...]

Once again the data demonstrate a sharp drop that has had no real prelude. February was a more or less normal month; then March and April saw collapse come out of the blue as the wheels went spinning off the wagons. These are the composite PMI indexes that include the manufacturing and services sectors. While there has been a slowing in place for some time (note that slowing was wide spread for one year ago and from six months ago), the preceding slowdowns were generally much more moderate. The three-month, six-month and 12-month data are averages. The changes February to April are nothing short of shocking.

Once again the data demonstrate a sharp drop that has had no real prelude. February was a more or less normal month; then March and April saw collapse come out of the blue as the wheels went spinning off the wagons. These are the composite PMI indexes that include the manufacturing and services sectors. While there has been a slowing in place for some time (note that slowing was wide spread for one year ago and from six months ago), the preceding slowdowns were generally much more moderate. The three-month, six-month and 12-month data are averages. The changes February to April are nothing short of shocking.

The queue standings on these short-period comparisons nearly all show new historic lows across countries back to early-2016.

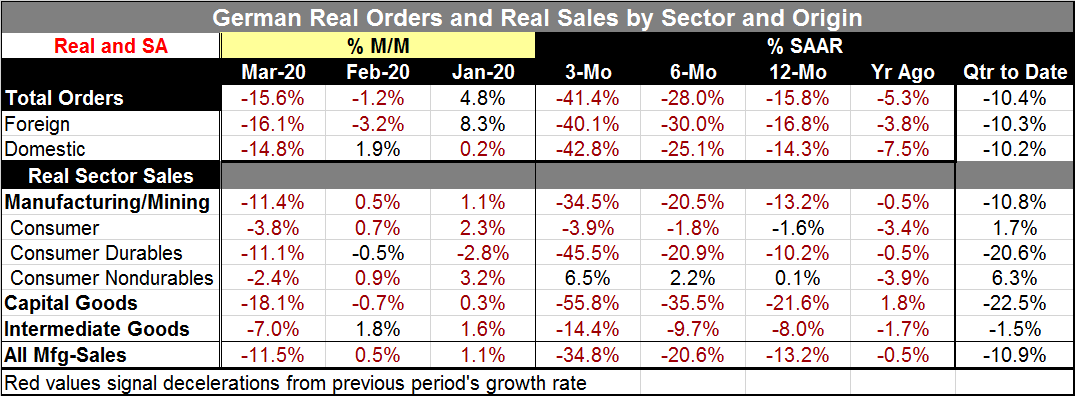

The day's reports featured a plunge in euro area retail sales, a record drop in German factory orders, and an implosion in the U.K. construction sector. India logs its weakest service sector reading ever.

The weak German orders data more or less speak for themselves. There is extreme monthly weakness, sequential weakness progressing across periods, and quarter-to-date weakness. Sales are imploding too. All these are inflation adjusted. The data simply show economic carnage.

The weakness story spins on, but a new wrinkle is that the German courts have found an aspect of ECB policy to be 'illegal.' However, the EU courts do not see it that way so no policy shift will be forthcoming. But it is a clear sign that in Germany they have had enough of this and the reaction in the Italian bond market shows that the markets got that message loud and clear. Governments can do only so much.

Historic Weakness in German Orders

Today/yesterday both the Fed and the EU Commission issued pronouncements about their economic conditions. The EU Commission weighed in on how bad their recession would be; The Fed laid out the case for how slow the recovery would be. Thee ae no quick fixes...

Governments are not going to begin to keep Humpty Dumpty together through this fall. And all the King's men (well, many of them anyway) are unemployed to boot.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief