Global| Jun 27 2008

Global| Jun 27 2008Global and EMU Money Supply Slows…but Gradually

Summary

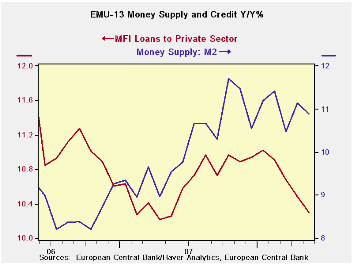

Money growth is slowing on a gradual pace. In EMU credit growth is slowing more rapidly, undoubtedly helped along by banks’ own credit tightening moves. The table shows that nominal money supply growth rates are slowly deteriorating [...]

Money growth is slowing on a gradual pace. In EMU credit

growth is slowing more rapidly, undoubtedly helped along by banks’ own

credit tightening moves.

The table shows that nominal money supply growth rates are

slowly deteriorating in various key money-center countries. The growth

in real balances (inflation adjusted money and credit amounts) is

decelerating faster than for nominal balances as the domestic price

level has shot up across all these nations even as nominal money growth

has slowed. We show the increase in the price of oil (WTI) to the far

right of the table.

Money and credit slow…

In EMU money and credit real balance growth (bottom of the table) is in

the 4% to 5% range over three months compared to the 7% to 8% range

over 12-months. In the US, the UK and Japan money growth is in the 0.5%

to 2% range over three months. In each case there is a deceleration

from the 12-month pace that is significant. These are growth-impeding

polices.

Policy risks may not be what they seem…

A slowing stimulus from real balances will help to slow growth in these

countries. Meanwhile, the myriad factors that remain in play from high

energy prices to banking sector problems continue to crimp growth. At

this point real money balances are simply slowing but their growth

rates remain positive. Still, there could be a substantial dose of

slowing that is in the pipeline from current policy restrictiveness due

to sluggish real balance growth let alone any tighter policy.

Still central banks are focused on interest rates and real

interest rates as they struggle to keep inflation expectations

‘anchored’. The ECB that places more weight on money and credit

aggregates than does the Fed in the US has the aggregates that are

growing the fastest even when adjusted for the effects of inflation.

The ECB is preparing to hike rates, a move that should further slow

money and credit growth there and could pressure other countries to

follow suit event though they seem farther along the road to credit

restrictiveness than the ECB – despite the fact that other countries

have cut rates when the ECB has not.

Too easy or too tight?

Based on the actual slowing of real balances the risk of being too

tight with policy seems quite plausible despite the obvious worry in

the tone from central banks that are concerned with inflation that is

over the top of its target ceiling or guideline. Slippage in inflation

expectations is not a price that any central bankers are wiling to pay.

But the policy risk now may be turning to the potential for overkill on

the side of restrictiveness when the credit crunch and depressing

effect of oil prices are both fully accounted for. Don’t look for it in

many central bank speeches, however. So far, only the UK’s Mervyn King

has said explicitly that to get control of inflation will require

slowing growth. He had previously said that controlling inflation would

involve pain. In the US its dual mandate does not allow the Fed

purposefully dish out pain to slow inflation. So look for the Fed’s

analysis of the economy to be too-cheery in order to permit it to be

tighter than it needs to be. The Fed is already cheerily saying that

spending has firmed, while it has jettisoned language about expecting

oil prices to flatten or fall yet it still expects inflation to fall.

Nice if you can get it. But will it be that simple?

| Look at Global and Euro Liquidity Trends | |||||||

|---|---|---|---|---|---|---|---|

| Saar-all | Euro Measures (E13): Money & Credit | G-10 Major Markets: Money | Memo | ||||

| €€-Supply M2 | Credit: Residential |

Loans | $US M2 | ££UK M4 | ¥¥Jpn M2+Cds | OIL:WTI | |

| 3-MO | 9.2% | 9.0% | 8.5% | 5.5% | 7.3% | 0.7% | 203.4% |

| 6-MO | 10.0% | 10.9% | 9.8% | 7.9% | 10.8% | 2.0% | 73.0% |

| 12-MO | 10.9% | 12.0% | 10.3% | 6.3% | 10.1% | 2.0% | 96.5% |

| 2Yr | 10.2% | 11.4% | 10.3% | 6.3% | 12.0% | 1.7% | 32.8% |

| 3Yr | 9.9% | 11.7% | 10.8% | 5.8% | 11.8% | 1.6% | 35.9% |

| Real Balances: deflated by Own CPI. Oil deflated by US CPI | |||||||

| 3-MO | 4.9% | 4.7% | 4.2% | 0.6% | 2.2% | 0.7% | 189.2% |

| 6-MO | 6.2% | 7.2% | 6.1% | 3.7% | 5.9% | 1.6% | 66.3% |

| 12-MO | 7.0% | 8.0% | 6.4% | 2.2% | 6.5% | 1.2% | 88.8% |

| 2Yr | 7.2% | 8.4% | 7.3% | 2.8% | 8.7% | 1.3% | 28.4% |

| 3Yr | 7.1% | 8.8% | 7.9% | 2.1% | 8.9% | 1.3% | 31.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief