Global| May 14 2007

Global| May 14 2007Germany’s retail sales flounder

Summary

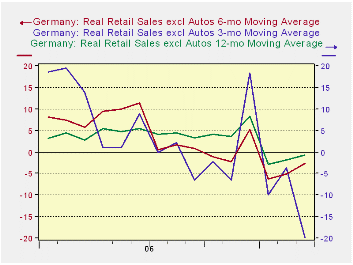

German retail trends are hard to pin down. The German VAT tax that took effect in January of 2007 helped to bulge retail sales in December and to wither them in the following months. The three-month growth rate is particularly weak in [...]

German retail trends are hard to pin down. The German VAT tax that took effect in January of 2007 helped to bulge retail sales in December and to wither them in the following months. The three-month growth rate is particularly weak in March, but that is because its base for the calculation is the elevated December level of sales. Even so, the Yr/Yr and six-month growth rates moved sharply lower in January and have stayed in a very weak growth plane.

March sales fell month to month. The March drop offset the sharp 1% gain in February that followed the 6.1% plunge in January. Sales declines were widespread in March. Auto sales were the contrary category with nominal sales up by a sharp 5.9% in March after rising by 7.1% in February. Autos seem to be recovering from their January plunge when sales fell by 30%.

Next month 3-mo sales should snap back strongly as 3-mo growth rates move their base to January the weaker from the strong December level. Even so that will not rid the six month and Yr/Yr growth from their weakness. While German retail sales are holding in, they are also much weaker than they were throughout 2006.

Officials remain upbeat on the prospects for growth in Germany. Early in the year results are mixed. Car sales alone are making a strong comeback but even they are lower by 2.7% Yr/Yr.

| Nominal | Mar-07 | Feb-07 | Jan-07 | 3-Mo | 6-Mo | 12-Mo | Year Ago |

| Retail Ex auto | -0.6% | 1.4% | -5.7% | -18.2% | -2.0% | -0.2% | 3.1% |

| Motor Vehicle and Parts | 5.9% | 7.1% | -30.2% | -60.7% | -17.8% | -2.7% | 8.2% |

| Food Beverages & Tobacco | -0.5% | -0.4% | -2.0% | -10.9% | -2.7% | -0.3% | 2.8% |

| Clothing & Footwear | -0.9% | 5.0% | -6.7% | -11.2% | 9.5% | 3.9% | 3.1% |

| Real | |||||||

| Retail excl Auto | -0.4% | 1.1% | -6.1% | -19.8% | -2.6% | -0.8% | 2.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief