Global| May 21 2008

Global| May 21 2008Germany’s IFO in Surprise Rise

Summary

Germany continues to show resilience even in the face of weak reports it has issued. Here is a reversal that fits in with the strong 2008-Q1 GDP that Germany reported. Not surprisingly this report also boosted the euro. Oddly with [...]

Germany continues to show resilience even in the face of weak reports it has issued. Here is a reversal that fits in with the strong 2008-Q1 GDP that Germany reported. Not surprisingly this report also boosted the euro. Oddly with this rebound in hand the stronger GDP behind us the IFO’s Gernot Nerb declares autumn as the proper time for the ECB to cut rates. With Germany showing such ‘strength’ and with inflation pressures swirling and engulfing even core inflation measures why should the ECB do any such thing, let alone ponder it?

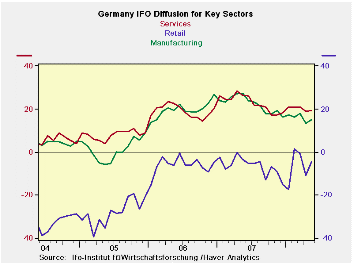

IFO measures remain at firm level in their respective ranges since 1991. The total index is in the 75th percentile of its range and most readings are in the 70s in terms of percentile readings. Wholesaling is a bit weaker and services sports a percentile reading that is pushing the 80th percentile (79.4). All sector readings also are well above their averages since 1991. The monthly rebound in May is robust and spans alls sectors except construction.

So is Germany recovering now? Is it merely cutting the losses from last month? Where does it stand?

Clearly the Nerb comments view this as a bit of a wry smile in the land of bad jokes. The improvement is not expected to continue if he is calling for an ECB rate cut buy August. But any continued strength could be a greater conduit for inflation pressures in the meantime. Those pressures clearly still are dogging the EMU economy. Granted that Germany is the strongest economy of all of these, and still it has the best inflation record. Those weaker economies in EMU have been pushing higher inflation results for some time. On the whole that growth/inflation mix remains a nettlesome problem for the ECB to attack.

The rise in the euro to a new one-month high Vs the dollar is telling. This report has shattered a paradigm that was in place. We cannot be sure how much staying power this monthly rise really has. But the Zew financial experts also saw it and flagged it correctly. Looking back at history it is hard to see how Germany and the rest of EMU can do well with such a strong euro value – looking at it in trade-weighted and inflation-adjusted terms. Orders data have been withering too. There are signs that weakness is still the operative trend.

The April diffusion reading from the IFO was the lowest since January of 2006. Plus it represents a sharp 4.7 point drop from its March value. The drop in March was the largest overall index drop since Sept of 2001. Even with the rebound in May, weakness shows though. May can be viewed as technical rebound and as still preserving the down-trend that has been put in place for the IFO barometer. But for the moment the outlook is confused enough to have boosted the euro FX rate. That strength is not going to be able to last either. But a stronger Germany makes the ECB more wary of rate-cutting and that, in turn, gives the stronger euro some fundamental support, at least for a while.

| Summary of IFO Sector Diffusion readings: CLIMATE | ||||||||

|---|---|---|---|---|---|---|---|---|

| CLIMATE Sum | Current | Last Mo | Since Jan 1991* | |||||

| May-08 | Apr-08 | Average | Median | Max | Min | range | % range | |

| All Sectors | 6.2 | 4.0 | -6.8 | -10.0 | 16.7 | -26.4 | 43.1 | 75.6% |

| Manufacturing | 15.0 | 13.3 | 3.5 | 3.5 | 27.4 | -22.7 | 50.1 | 75.2% |

| Construction | -20.3 | -20.0 | -33.4 | -39.2 | -8.0 | -50.5 | 42.5 | 71.1% |

| Wholesale | 4.0 | 1.6 | -10.6 | -15.7 | 23.4 | -39.4 | 62.8 | 69.1% |

| Retail | -4.4 | -10.9 | -20.3 | -19.6 | 1.3 | -39.7 | 41.0 | 86.1% |

| Services | 19.4 | 18.9 | 9.8 | 9.0 | 28.5 | -15.7 | 44.2 | 79.4% |

| * May 2001 for Services | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.