Global| May 24 2016

Global| May 24 2016Germany: ZEW Expectations Step Back

Summary

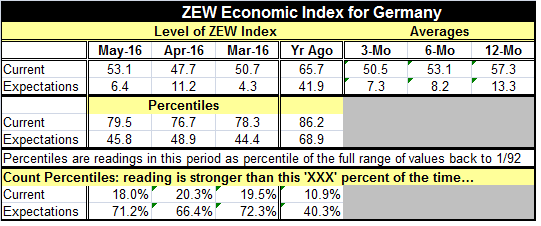

Unexpected step back for ZEW forward-looking metric The German ZEW index in May saw its expectations indicator fall sharply while the current index moved higher. The current reading is quite strong as it is stronger only 18% of the [...]

Unexpected step back for ZEW forward-looking metric

Unexpected step back for ZEW forward-looking metric

The German ZEW index in May saw its expectations indicator fall sharply while the current index moved higher. The current reading is quite strong as it is stronger only 18% of the time historically. The expectations index is higher fully 71% of the time. Since peaking in September, the current index has been steadily working its way lower while expectations have remained stuck at very low readings since February of this year.

ZEW financial experts weigh in on investment preferences

The ZEW financial experts' assessment of stocks ticked higher this month to a reading of 6.1 while the assessment for bonds slipped to -6.0 from -5.4. Both stocks and bonds are carrying very middling rating compared to their historic ratings. Stocks have been rated higher about 37% of the time and bonds have been rated higher about half the time. Neither rating is a ringing endorsement.

The most challenged sectors

The profitability of the banking and insurance sectors remained negative as it has been persistently since June 2011. Utilities profitability also has a long string of negatives. That pessimism has dogged the sector ever since nuclear power was put in a phase-out mode. The vehicle sector has a negative reading, having been negative for eight of the last nine months. Steel and metals have eight negative readings in a row.

Key stock sectors tell the story of German pluses and minuses

The consumption/trade sector has a 99th percentile standing in its historic queue of data. It has had a rating in the top 90th percentile of its historic queue of data for 15 straight months- including its all-time high reading in February. Info-tech and electronics rank particularly high as well. The construction sector has logged a top 10% position over the past four months. The consumer and tech sectors continue to shine in Germany and there is enough momentum to underpin the construction sector. In that Germany's key drivers seem similar to those in the U.S.

ZEW as an indicator

The ZEW index is a reasonably good harbinger of the upcoming industry survey from the IFO. These various surveys from ZEW, IFO, the EU Commission, and the Markit (PMIs) have been broadly consistent. Surveys consistently show that the consumer or retailing subsectors have been the relatively best-performing sectors in Germany.

The German story: a euro-fairy tale

The story for Germany has been that manufacturing, the usual economic driver, is still `strong' by the standard of other EMU members, but by its own history it is relatively sluggish. Consumer confidence and spending metrics have been consistently strong in this mature stage of recovery. The unemployment rate is the lowest in Europe by a very substantial margin. The migrant issues that for a while seemed ready to envelope and even overwhelm Germany were in the end derailed by the closure of the path to Germany by the peripheral EU nations that closed their borders.

EMU: A house divided against itself... is still standing

Germans as people as well as German policymakers seem to have stiffened their resistance to ECB efforts to take steps to stimulate EMU-area growth. The German economy is doing well-unemployment is at a reunification low- and Germany does not see the need for any special stimulus in the EMU. However, Germany's experiences, among those of other EMU members, are atypical. Other EMU nations are lagging badly the German performance as well as their own historic metrics. The problem is not simply too-low inflation although that is the only mandate that the ECB has and it is its only wedge for policy action. Germany continues to be happy with low-even too low inflation-with most policymakers in Germany referring to conditions that flirt with deflation as `moderate' inflation. Meanwhile, the ECB wants to use target undershooting as an excuse to take bolder action. This week ECB Executive Board member Peter Praet said that the risks of a de-anchoring of inflation expectations to below 1% or close to zero in the euro area have increased and argued for a more forceful ECB policy to fight it. Praet is chief economist of the European Central Bank. Within the board, Praet is widely considered to be centrist on monetary policy, perhaps with a dovish tilt-certainly to the left of the Germans. He defends the ECB's actions and asserts that the ECB still has policy tools and that it has not been crippled (by dissent). Praet also dismisses talk that the ECB has been `late' by asserting that the ECBs resolve to avoid deflation is clear. However, the ongoing dissent and obstructions to continued steps to stimulate growth by German policymakers and their opposition to the policy that has produced negative interest rates is not to be so lightly dismissed. Praet's dismissal of the criticism that the ECB was late in acting may simply be a way to brush aside the fact that the ECB was late to act because it was blocked by the Germans. And time is of the essence in monetary policy. Dissent does stalk the ECB.

Feeling the impact of a weak global economy

What we see in Europe is the result of a number of restraining factors. It has a banking system that is too weak to respond to the monetary stimulus that has been laid at its feet. Fiscal restrictiveness collars domestic demand in a number of countries. Discord over the handling of the migrant crisis, and of the future of the Schengen program, also sows seeds of disunity in Europe. In the end, there are a lot of issues dividing the EMU. The pending Brexit vote is a threat to the EU whose structure underlies the EMU. But polls seem to show that votes in favor of Brexit are not growing and that the separatists do not have the votes. In addition, weak growth globally hampers the EMU. The ZEW survey shows that despite much better than EMU-normal activity and conditions in Germany the Germans still have their own worries about where things are going. All is not well in euro-land or in the magical low-inflation world of Germany.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief