Global| Apr 23 2020

Global| Apr 23 2020Germany: The Hammer Falls on Confidence in May

Summary

The expectation for German confidence in May has taken the sharpest, deepest and broadest turn for the worse on record. The German April reading had taken 'a step down' and a significant one at that. But the full realization of what [...]

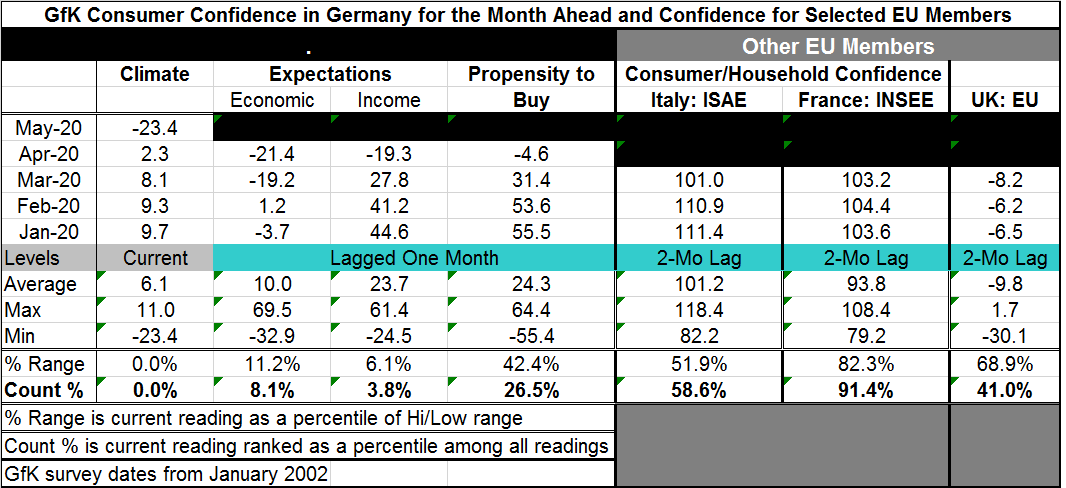

The expectation for German confidence in May has taken the sharpest, deepest and broadest turn for the worse on record. The German April reading had taken 'a step down' and a significant one at that. But the full realization of what lay in store appears to be laid out in all the consternation possible in May. The German climate index fell to a reading of -23.4 in May from 2.3 in April. The previous weak reading on data back to 2002 was -3.5. There is simply no comparison. And the weakness is reflected across the components as well.

The expectation for German confidence in May has taken the sharpest, deepest and broadest turn for the worse on record. The German April reading had taken 'a step down' and a significant one at that. But the full realization of what lay in store appears to be laid out in all the consternation possible in May. The German climate index fell to a reading of -23.4 in May from 2.3 in April. The previous weak reading on data back to 2002 was -3.5. There is simply no comparison. And the weakness is reflected across the components as well.

Component readings lag by one month. The economic expectation in April fell to -21.4 after logging a -19.2 in March. March was the 'month-of revelation' for economic expectations as the drop was from +1.2 in February. There has been little reassessment in April compared to March as that month-to-month slippage was minor. We'll see later about May. The April reading for economic expectations has been weaker in the past, from November 2002 to May 2003, and also from October 2008 through May 2009. There have been sporadic negative readings in this cycle since July 2019 pre-dating the emergence of the corona crisis.

Income expectations, however, have held to firmer ground until April. The topical reading for April finally plunged negative, falling to -19.3 from March's 27.8. This was the sharpest month-to-month drop on record. March had been weaker at 27.8 compared to 41.2 in February. There are only eight income expectation readings weaker than the reading posted in April.

The propensity to buy index turned negative in April, dropping very sharply to -4.6 from March's 31.4. This is the second-sharpest fall in the propensity to buy exceeded only by its January 2007 month-to-month drop of 65 points. The two-month drop in this cycle logs a plunge of 58 points. As with the other components, it had also slipped in March to 31.4 from February's 53.6. The buying climate has three broad periods of negative readings previously. But the last negative reading was in December 2008. This series that dates back to January 2002, has just seen its longest period of consistently positive readings terminated.

The assessment of the impact of the virus in Germany has clearly been on the minds of consumers and weighing on them mildly, then more forcefully, and finally with full impact. German GDP is expected to decline and policy is doing what it will to cushion the blow.

The consumer confidence readings from around Europe, also chronicled in the table, are still more or less a walk in the park. None are more up-to-date than March and the German March reading (that we got in late-February) was the start of the German unravelling. But Italy's March reading fell to 101 from February's 110.9. The French reading ticked lower to 103.2 from 104.4. The U.K. reading, already negative in the wake of wresting over Brexit terms, fell to -8.2 from -6.2. All of these are just garden variety slippages, except Italy. Italy has a queue percentile standing for confidence at its 58th percentile; the U.K. standing is weaker still at its 41st percentile; France held high at its 91st percentile in March. But all those reading are from the cusp of the emerging crisis.

The German percentile standings in May/April put the headline GfK index at it all time low. Economic expectations are at their 8th percentile. Income expectations are at their third percentile. And the propensity to buy is at its 26th percentile.

The virus is sweeping away consumer optimism in Europe and installing a very sour mood in its place. Its impact on jobs, spending, income and growth will be manifest in the coming months. Authorities are doing what they can which is a mixed message since they are ordering people not to mingle then trying to cushion the blow of preventing them from earning a living. In Germany, there are some signs of letting up on the strictures. But France is still battling the unrest in its Paris suburbs from the reaction to the order for confinement. The U.K. had a later start and it still waiting for conditions to improve. Still, the situation in the U.K. has improved enough for the political backlash and criticism over the late start to have emerged. Europe still has a very rough road ahead. However, there are signs of progress and if backsliding is prevented, Europe will go through a very rough patch then see how quickly and fully it can get back to or toward normal. That process is going to be much more drawn out than the optimists had hoped and we see that in the tempering of consumer sentiment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief