Global| Jan 25 2016

Global| Jan 25 2016Germany's Ifo Turns Sour; Is It Part of the Global Malaise?

Summary

The German Ifo survey stepped back in January as it deteriorated much faster than the ZEW survey had expected. The ZEW index is a survey of financial experts and reveals their perceptions of the economy. The Ifo is an industry survey [...]

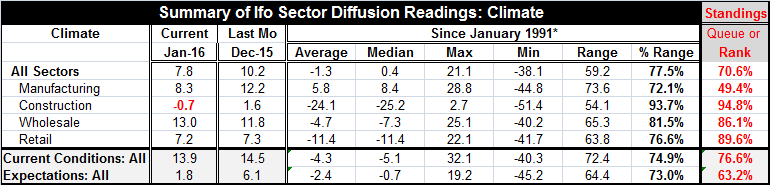

The German Ifo survey stepped back in January as it deteriorated much faster than the ZEW survey had expected. The ZEW index is a survey of financial experts and reveals their perceptions of the economy. The Ifo is an industry survey that queries the participants themselves by sector. Only Wholesaling improved in January compared to December. Manufacturing was set back substantially in January compared to December. Both current conditions overall and expectations weakened. Expectations were set back reasonably hard in January. Business expectations have fallen by more in one month only 4% of the time historically. Over two months the drop has been larger only 13% of the time. Clearly expectations are running into some hard times.

The German Ifo survey stepped back in January as it deteriorated much faster than the ZEW survey had expected. The ZEW index is a survey of financial experts and reveals their perceptions of the economy. The Ifo is an industry survey that queries the participants themselves by sector. Only Wholesaling improved in January compared to December. Manufacturing was set back substantially in January compared to December. Both current conditions overall and expectations weakened. Expectations were set back reasonably hard in January. Business expectations have fallen by more in one month only 4% of the time historically. Over two months the drop has been larger only 13% of the time. Clearly expectations are running into some hard times.

In the graph, we present the overall Ifo current conditions and expectations indices. In the table, we present the diffusion indices which provide more early information on sectors. Both sets of data show the onset of weakness. While the construction sector metric turned negative, it has been so weak that its negative reading still has a very high queue standing, in the mid-90th percentile. However, manufacturing's drop has taken its standing to the 49th queue percentile, leaving it just below its historic median. Wholesaling, improving on the month, moved up to its 86th percentile. Retailing moved lower but still stands in its 89th percentile. Clearly there are substantial differences in performance across sectors. The overall multi-sector assessment fell to its 70th percentile in January. It stands at its lowest level since February 2015.

Migrant issues nag

Issues over migrants, their behavior and their suitability continue to dominate the dialogue in Germany. There has been a rash of examples of migrants behaving badly and this is creating a problem and has undermined Angela Merkel and her ongoing support for migrants.

Meanwhile, at the EU level, preparations are being made to give Turkey a slug of funding to help it block migrants. Greece was warned about the possible withdrawal of its Schengen privileges because on the influx of migrants it has not been able to control. It is hard to know what the EU wants Greece to do as migrants come in by sea and pile up. Of all EMU/EU nations, Greece is a very small country with extremely limited resources and is vulnerable to the sea landing of migrant people. Pressuring Greece seems to be just another example of how irrational the approach has become to the issue of migrants in the EU.

There is palpable weakening afoot

While Germany has this political problem with migrants that it is trying to solve, it also has a slipping economy. Germany remains the best-performing economy in Europe by far, but the day's report from the Ifo underlines that there is also some erosion in place. We can argue about its source, but it is there. Business expectations have fallen to their 63rd percentile in the diffusion format while overall current conditions are holding at their 76th percentile level in January.

Are there negative market effects in tow?

Apart from worrying about migrants, there are concerns in Germany, the EU and globally, about how much damage the global stock selloff will do to the real economy. Germany already had some special issues with carmaker Volkswagen under pressure before the generalized stock selloff began. One view is that stock indices are not predictive of the economy's condition. There is the famous line by economist Paul Samuelson that the stock market has predicted nine of the last five recessions. Still, the point remains that the stock market selloff has been severe and is not simply `predictive' or not. It has become an issue in and of itself. The selloff is lasting. It is also global so its impact is worldwide. And it has resulted in a significant loss of wealth which could show up as less consumption through a negative wealth effect or simply could erode consumer confidence and affect adversely the feeling people have about economic wellness.

For these reasons and because the oil price continues to fall, there are many policymakers watching stock markets very closely and a lot of conjecturing about the significance of the selloff. Simple sobriquets from the past hardly seem to be the appropriate treatment under current circumstances. One aspect of our current circumstance is that interest rates globally already are so low, limiting the impact of what central banks can do should they wish to offer some simple support. Another aspect is that this stock market selloff comes with economic growth already so weak and weakening further in some places. This is not a selloff occurring in a robust economic environment. That could mean that the potential for wealth effect damage could be much worse than in the usual case. We all can recall the view of there being a Greenspan `put' in the U.S. Well, Greenspan is gone and Yellen seems put-out with stimulus, let alone trying to save the stock market.

Wrap up

For whatever reasons, the German Ifo has stepped back and its drop has undercut the more rosy view offered by the ZEW index previously. Germany's Ifo report shows some significant weakening, not surprisingly, featuring a weaker manufacturing sector. Despite a vague statement by the ECB about being able to do more, perhaps in March, markets are still adrift and policymakers seem to be reluctant to do anything. This has as much to do with their outright policy agnosticism or skepticism about the need for action as it has to do with the fact that policymakers have little scope to take any action that might be helpful even if they wanted to act.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief