Global| Jun 24 2015

Global| Jun 24 2015Germany's Ifo Steps Back in June

Summary

Germany's Ifo business confidence index fell to 107.4 in June from 108.5 in May. The table below presents a diffusion treatment of the Ifo indexes since we can see sector details faster in this treatment of the survey. The all-sector [...]

Germany's Ifo business confidence index fell to 107.4 in June from 108.5 in May. The table below presents a diffusion treatment of the Ifo indexes since we can see sector details faster in this treatment of the survey.

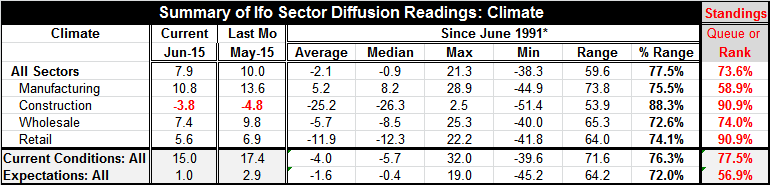

Germany's Ifo business confidence index fell to 107.4 in June from 108.5 in May. The table below presents a diffusion treatment of the Ifo indexes since we can see sector details faster in this treatment of the survey.

The all-sector climate index fell to 7.9 in June from 10.0 in May and now stands at a moderately firm level in the 73rd percentile of its historic rank (or queue) of data. Among the sectors, retailing and construction have the highest queue standings, in their respective 90th percentiles. Construction became less weak in June, increasing to a -3.8 diffusion value from -4.8 in May. But retailing took a step back to 5.6 from May's 6.9. Wholesaling with a 74th percentile standing fell to a diffusion value of 7.4 in June from 9.8 in May. Manufacturing, the weakest sector with a queue standing in its 58th percentile, stepped back sharply on the month to show a 10.8 diffusion value, down from 13.6 in May. This is a broad-based step back for the Ifo sectors' climate readings.

The overall current conditions index fell back to a 15.0 reading in June from 17.4 in May to notch a 77.5 percentile queue standing. Expectations are weaker still, falling to a 1.0 diffusion reading from May's 2.9, to a 56th percentile standing.

European data continue to swing to and fro. The data are like the Ifo showing an uptrend but with vacillation. Is this month simply a swoon on the way to further improvement or is it a real setback? The manufacturing index fell sharply and has a weaker monthly change only 14% of the time. There is some severe weakness here as well as broad-based weakness.

Germany is still caught is the euro-mire that includes ongoing sparring with and sanctions on Russia as well as uncertainty over Greece. Greece continues to hang in the balance even after a productive meeting earlier this week. Russia is considering imposing some new sanctions in the wake of the stubbornness of the EU in keeping its own sanctions in place. All of this makes for a damped business environment.

Meanwhile, global growth is still uneven. China did post another sizeable, though smaller, gain in its monthly LEI and U.S. GDP was revised in Q1 to show a smaller loss. Still, in Japan, small businesses reported unexpectedly weaker conditions. The road to better global growth remains a bumpy one with a low speed limit.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief