Global| Oct 25 2013

Global| Oct 25 2013Germany's Ifo Stalls in October

Summary

The German Ifo index has slowed over the past three months. We present the diffusion indices for the sectors and the overall measures in the table, but the Ifo also presents these measures as indices. The business climate index has, [...]

The German Ifo index has slowed over the past three months. We present the diffusion indices for the sectors and the overall measures in the table, but the Ifo also presents these measures as indices. The business climate index has, in the past three months, stood at 107.4, 107.7 and 107.6, sequentially. This climate measure has hit plateaus and backed-and filled only to advance again in the past. But each one of these pauses, slowdowns or setbacks is a new reason to re-inspect the trend. The chart plots the Ifo measures as indices instead of as diffusion indicators, as in the table. The trend seems to be bending lower.

The German Ifo index has slowed over the past three months. We present the diffusion indices for the sectors and the overall measures in the table, but the Ifo also presents these measures as indices. The business climate index has, in the past three months, stood at 107.4, 107.7 and 107.6, sequentially. This climate measure has hit plateaus and backed-and filled only to advance again in the past. But each one of these pauses, slowdowns or setbacks is a new reason to re-inspect the trend. The chart plots the Ifo measures as indices instead of as diffusion indicators, as in the table. The trend seems to be bending lower.

The index plot of the Ifo measures shows that the current situation assessment is still advancing, but that it had a set-back this month. Expectations have faltered in the month as well. The expectations index is at 103.6 in October, down from 104.2 in September, but that is still up from its 103.3 value in August. The current situation index is off for two months in a row but it had strong upward momentum prior to that.

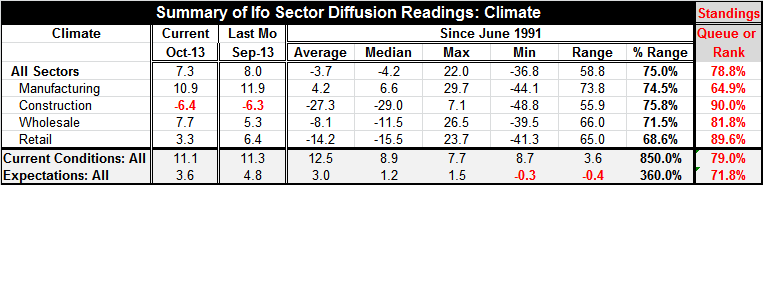

The diffusion indices in the table show us the results for climate by sector. All sectors backed off in October except for wholesaling, which advanced.

Over 12 months the manufacturing has been improving the most, but it has slipped back in recent months. The wholesaling sector has been a leading sector recently, in terms of making the strongest monthly changes. Retailing has also improved, but it has been only middling at best over the past year. Retailing slipped back in October.

Over the past year the monthly improvement in current conditions has surpassed increases in expectations. This raises the question as to whether or not the outlook is going to be able to improve, or worse, if it will begin to slip. Over the past 12 months expectations have risen by only 0.3 points per month compared with current conditions that have advanced by 0.9 points per-month. Questioning momentum is valid given the recent time-line of data.

When we look at the outright diffusion values by sector and rank each in an historic context, we find somewhat surprising leadership in this recovery. Construction is the relative strongest sector with its October index standing in the 90th percentile of its historic queue. Retailing is next at the 89th percentile of its historic queue. Wholesaling is in the 81st percentile of its historic queue. Manufacturing stands only in the 64th percentile of its historic queue - lagging the pack.

It is not surprising to see manufacturing lagging in terms of its standing in recovery. We have already showed that manufacturing has the strongest gains over the past 12 months. In a recession the manufacturing sector always gets hit the hardest; therefore, moving up in recovery from a very weak position at the bottom of the recession. This is true of this recession episode for Germany. Still, at this point in the recovery the German manufacturing sector is lagging the retailing sector by the largest amount in any period since the early 1990s.

Even though manufacturing has the highest net diffusion reading in the table when we compare its current value to its history, manufacturing is weaker relative to its own history than the metrics for the other sectors. Since Germany is a strong manufacturing-based economy, what we see is how much Germany's recovery is being battered by world events. The German manufacturing sector is strong relative to its fellow EMU members, but relative to its own standards German manufacturing is still spinning its wheels.

Germany is still the leading economy is Europe. But the weaker Mediterranean counties are beginning to get some traction. Conditions in the South are still quite poor. But all eyes are on recovery. It would be a difficult time for Germany to start backsliding. But the rebound/improvement in the South is not yet a dependable phenomenon. While Germany's retail sales are doing relatively better than manufacturing, Germany is still no locomotive for European growth. The rest of Europe will have to find its own way to recovery. That will be even harder - probably impossible- if Germany's recovery slides back and weakens.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief