Global| Apr 24 2020

Global| Apr 24 2020Germany's IFO Plunges to All-New Depths

Summary

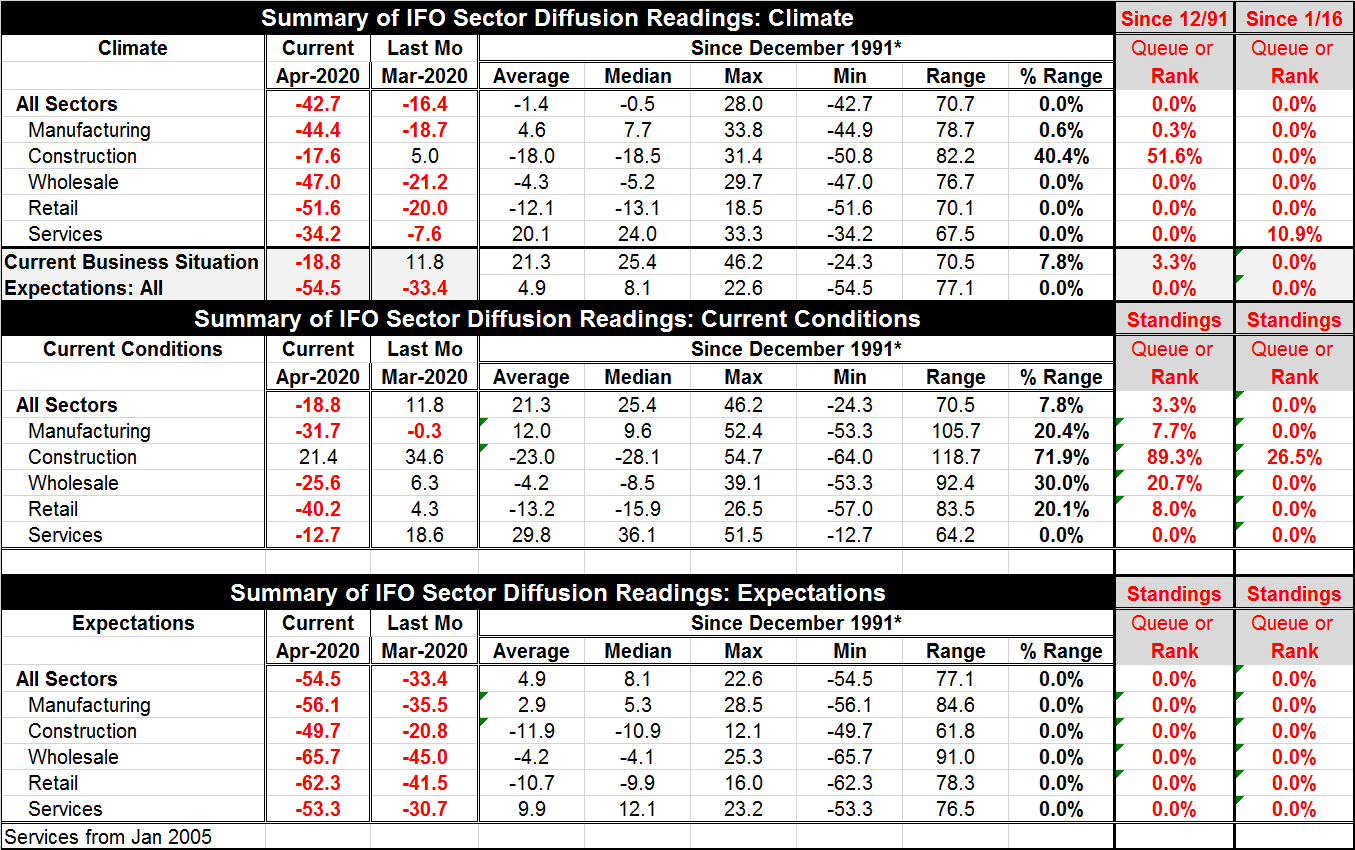

This is not snorkeling or even deep sea diving; it requires a bathyscaphe. The German IFO has sunk to new depths even after a substantial plunge a month ago. All of the rankings display severe weakness with the ongoing lone exception [...]

This is not snorkeling or even deep sea diving; it requires a bathyscaphe. The German IFO has sunk to new depths even after a substantial plunge a month ago. All of the rankings display severe weakness with the ongoing lone exception of the construction sector in current time; but even that sector succumbs in the expectations profile where on both horizons' sectors are looking at expectations of their worst conditions.

This is not snorkeling or even deep sea diving; it requires a bathyscaphe. The German IFO has sunk to new depths even after a substantial plunge a month ago. All of the rankings display severe weakness with the ongoing lone exception of the construction sector in current time; but even that sector succumbs in the expectations profile where on both horizons' sectors are looking at expectations of their worst conditions.

Without splitting hairs all readings have fallen and all are showing either extreme weakness or a most abjectly negative outlook. Even Angela Merkel has admitted that this virus has hit Europe hard and will require a larger EU budget than the EU members have been sued to.

However, even with that statement from the German leader at a time that Germany has continued to be fiscally conservative, the EU is having a very hard time deciding what to do and more importantly how to fund it. Pooled liability corona-bonds seemed to be on the table and at one point a few weeks ago French President, Emmanuel Macron, had said that their use had been decided. Then that proposal was gradually pulled off of the table as the most fiscally conservative EU nations could agree to do it. EMU members want to do something, but they cannot agree what or more precisely they cannot agree on how to fund ‘it' whatever ‘it' is. And without funding, ‘it' does not happen. The Mediterranean (or Southern) members of the Union have been hit hardest and are in need of help. While they have been offered some respite from Maastricht budget and debt constraints, they are wary and want to be indemnified from any future austerity programs imposed because of debt – excess to the Maastricht allowance- taken on during the crisis. No one wants to go through austerity programs again. But the richer North still will not back funding. This is a case of the EU knowing most precisely what it will not do and that standing in the way of what it must do.

The German situation is bad even though Southern Europe may be feeling the pinch harder and with fewer resources to respond to it. Germany and Austria are beginning to open up slowly. Today Spain reported the fewest death knells heard in a month. However, the German IFO survey shows NO optimism in its expectations index.

The future...lies ahead of us

That is about all we are sure of... The future lies ahead, but no one has a clue what it will look like. Bank of England policymaker Gertjan Vlieghe said today that the U.K. economy is still undergoing contraction and called a quick rebound ‘unlikely.' While the U.K. is no longer an EU member, that sentiment sums up what many are coming to think. The belief that the economy was healthy when the virus struck and the conclusion that that that will imply a ‘V-shaped' recovery is falling out of favor. German expectations fell hard in April and fell broadly for each and every segment. Right now the IFO assessment is that Germany is still on the slippery part of the slope. This is despite a move to open some industries and businesses. The return-to-normal progression is untested and is fraught with pitfalls. Maybe NEXT MONTH, the IFO expectations reading will gain some footing and improve month-to-month. That is what we will be looking for. Survey participants will have to be able to see a future improved relative to the present. Currently, that does not describe the payoff matrix seen by industry participants in this survey. But that is what we will be looking for as a sign that turnaround is on the horizon. Certainly, seeing actual policy initiatives change for the better is a first step. But it is not enough of one to shift sentiment on the outlook just yet.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief