Global| Jan 27 2014

Global| Jan 27 2014Germany's Ifo Is Still Climbing

Summary

Germany's diffusion indices have been at it again as they improved in January compared to December. For business confidence it is the third straight month of month-to-month increases and it is the third straight month of increases for [...]

Germany's diffusion indices have been at it again as they improved in January compared to December. For business confidence it is the third straight month of month-to-month increases and it is the third straight month of increases for expectations as well.

Germany's diffusion indices have been at it again as they improved in January compared to December. For business confidence it is the third straight month of month-to-month increases and it is the third straight month of increases for expectations as well.

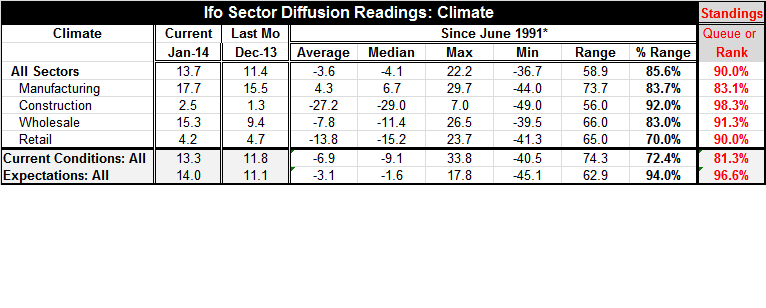

In the chart we depict the index values for expectations, business conditions and climate. In the table we present the diffusion indices available by sector to judge how the various sectors are performing.

The sector readings are uniformly strong. Interestingly, manufacturing is the most lagging sector when we present the data as a percentile standing in their respective historic queue. This method of presenting data ranks the current observation in the historic queue of data, presenting the result is a percentile standing. As a result sectors are not ranked by the height of their raw diffusion index in the month but rather by a statistic that tells us how close the current measure is to being in the top of the queue of all historic numbers. On this basis manufacturing stands at the 83rd percentile of its historic queue. It is the weakest sector of all those presented in the table. The strongest sector is construction which sits in the 98.3 percentile of its historic queue. It has only been higher about 2% of the time. Let me emphasize that we create these statistics from the queue of data so interpreting the result in terms of the percent of the time that the statistic is higher is correct. These are not statistics based upon the percent of the range. The queue statistics have the merit of using all of the observations in the distribution. The percent of range statistics have the shortcoming of using only the highest and the lowest statistic along with the current observation. These are percent of queue data that are more powerful and that use the full spectrum of data historically to ranking sector.

The all-sector index is in the 90th percentile and in fact each one of the sectors is in its respective 90th percentile or higher. This is a very impressive report on the German economy.

Turning to the overall assessments on current conditions and expectations, we find that current conditions stand in the 81st percentile of their historic queue compared to expectations which stand in the 96th percentile of their historic queue. Each of these metrics expanded this month. While the standing of expectations is much higher than for current conditions both measures represent strong readings on the German economy.

Looking at the various sectors, unfortunately, retailing took a step back in January as its diffusion reading deflated to 4.2 from 4.7. Germany has been criticized for running a recovery which has been export-led in which has not spun out many externalities to help the other economies in the monetary union. The German Finance Minister Wolfgang Schauble has said that Germany within the community has been balanced trade but noted that Germany will take steps to reduce its trade surplus in the future. But as we can see, as of January, retailing is lagging every sector but manufacturing. Retailing is deflating in January and it is the only sector to do so.

While Germany is the strong economy of Europe, let's understand that by that we mean it is an economy that is stuck in a very powerful first gear. Germany is not strong because it is spinning out growth rates of 4%. A strong German growth rate is something in the area of 2%. But German growth tends to be relentless and has been able to push through difficult times and turn positive when other countries were still experiencing setbacks. Germany now also has the largest current account surplus in the world, something else for which it is receiving criticism. The surplus means that Germany has a high savings rate and that it is under consuming at a time that other nations' producers are looking for demand to spur the growth in their output. Instead of helping, it is the strong German economy that is scarfing up demand everywhere satisfying it with German output, generating little retail demand for foreign goods, and leaving little for the firms in other countries to exploit and on which to build their growth.

Unemployment in the monetary union is still hovering at record highs a 12.1%. At the same time, like in the US, Europe continues to experience problems the labor force participation rates. However, Europe is looking to recovery and as it looks to recovery the banking sector already is starting to show some strains as the pressure on interest rates is beginning to rise above ECB-targeted levels. While many think that the emergency funding program should continue, banks are acting as though we could be coming to an end to it and everyone is awaiting the next round of results from European stress tests on banks which could either reassure of raise new uncertainties for banks. The bottom line on this is that there is still a great deal of trouble and dislocation in Europe. Whether it is appropriate to continue extraordinary help from the central bank or not remains a matter of policy discussion. But Europe needs more growth and it needs growth to be better spread-around rather than for Germany to take up the larger portion and leave the scraps for the other countries. Time will tell whether Germany is making changes that will help its fellow EMU members or whether it will continue to run policies that only make the German economy stronger to the detriment of its neighbors.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.