Global| Sep 24 2014

Global| Sep 24 2014Germany's Ifo Continues to Slip

Summary

In the wake of the weak PMI data from Markit released yesterday, it's not surprising to see that the German Ifo index continues to slip in September. The Ifo all-sector index has fallen from 5.3 in August to a level of 2.3 in [...]

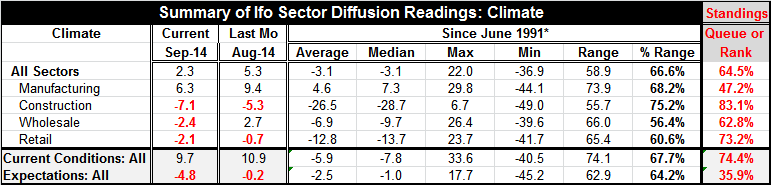

In the wake of the weak PMI data from Markit released yesterday, it's not surprising to see that the German Ifo index continues to slip in September. The Ifo all-sector index has fallen from 5.3 in August to a level of 2.3 in September; it now resides in the 64th percentile of its historic queue of data, a relatively moderate-to-weak reading. There is the month slippage in all the major categories, although the index for current conditions holds up the best.

In the wake of the weak PMI data from Markit released yesterday, it's not surprising to see that the German Ifo index continues to slip in September. The Ifo all-sector index has fallen from 5.3 in August to a level of 2.3 in September; it now resides in the 64th percentile of its historic queue of data, a relatively moderate-to-weak reading. There is the month slippage in all the major categories, although the index for current conditions holds up the best.

Sector weakness is led by the wholesale sector which makes a sharp turnaround from a 2.7 reading in August to a -2.4 reading in September. This turnaround brings the wholesale reading down to the 62nd percentile of its historic queue of data. Manufacturing slips from a 9.4 reading in August to a 6.3 reading in September. The slide brings manufacturing down to the 47th percentile of its historic queue, a level below its historic median. The construction sector remains weak and contracting; the -7.1% reading in September is down from a 5.3 reading in August. However, construction is used to a negative numbers and these deteriorating readings are still in the 83rd percentile of their historic queue. The retail sector slips to -2.1 in September from -0.7 in August. This reading leaves the retail sector in the 73rd percentile of its historic queue.

Current vs. Expectations

The current conditions reading has slipped the least in September. It has fallen from a level of 10.9 in August to 9.7 in September. At this level, it still resides in the 74th percentile of its historic queue, a moderately firm level. This tells us that in Germany, the current economy is holding up relatively well. We saw this in the PMI data released yesterday as the manufacturing index was getting quite weak but the services index was holding up quite well. Germany right now is a country being held up by its services sector while being weighed down by its manufacturing sector. The expectations index fell sharply to -4.8 in September from a level of -0.2 in August. The sharp drop leaves expectations in the 35th percentile of its historic queue. When you speak of deterioration in Germany, expectations are where the action is. As we can see, the current conditions index is holding up. But expectations are deteriorating very quickly. The deterioration in expectations has torn down the current conditions index over the recent months. There continues to be concerns about how the situation in Ukraine plays out. It's a major source of uncertainty for the German economy.

In today's news about Ukraine, we have NATO saying that it has detected no German troop withdrawal from the rebel territories. We have Ukraine itself urging the rebels to stop their shelling activity. Despite the existence of what supposed to be a ceasefire and all-around withdrawals of troops, it appears that none of that is in progress. Vladimir Putin in Russia seems to think that he can do whatever he wants as long as he says something that sounds conciliatory. He continues to deny that there have been any Russian troops in Ukraine. With such outrageous lying passing for statements of fact, it's not surprising that the situation in Ukraine continues to muddle on.

At present, Germany has three of its four sectors with negative readings. The manufacturing sector is the lone positive reading but it is relatively weaker when we look at the queue percentile rankings. On that basis, it is the weakest of the sectors. When we step away from overall climate to look at current conditions, we find things are much better off with the current conditions index in its 74th queue percentile, which is a relatively firm reading. However, up and down the Ifo report, we see plenty of evidence of weakness and that's not very reassuring. Importantly, the things that worry the German economy are still in play, remaining trouble spots.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief