Global| Mar 26 2019

Global| Mar 26 2019Germany's Consumer Confidence Is Set to Slip

Summary

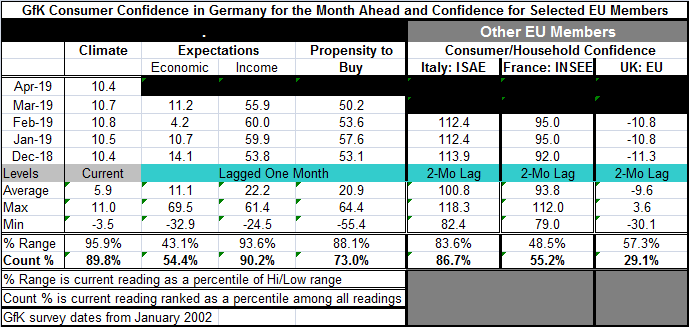

The GfK German consumer confidence reading is lower in April at a level of 10.4, down from 10.7 in March. The drop marks the second monthly drop in a row. The level of the reading in April is the weakest since December 2018. GfK is a [...]

The GfK German consumer confidence reading is lower in April at a level of 10.4, down from 10.7 in March. The drop marks the second monthly drop in a row. The level of the reading in April is the weakest since December 2018. GfK is a forward-looking consumer confidence survey for Germany that assesses the climate.

The GfK German consumer confidence reading is lower in April at a level of 10.4, down from 10.7 in March. The drop marks the second monthly drop in a row. The level of the reading in April is the weakest since December 2018. GfK is a forward-looking consumer confidence survey for Germany that assesses the climate.

GfK components

The GfK index has several components, but they are only available with a one month lag. In March income expectations sank to 55.9 from 60.0. The propensity to buy rating slipped to 50.2, its weakest since December 2016, from 53.6. The income expectations reading was last weaker two months ago. Income expectations as assessed in March have been higher historically only about 10% of the time. But the propensity to buy has been stronger more than 25% of the time. By comparison, the economic expectations produced a step up in March to a reading of 11.2 from a 37-month low of 4.2 in February. But the economic reading has only a 54th percentile standing implying that it lies close to its historic median.

Overall climate

The German overall climate reading that slipped to 10.4 for April has an 89.8 percentile queue standing overall. It too is still quite strong having been stronger only about 10% of the time historically. In addition, expressed as a position in its high-low range, the overall climate reading stands in the 95.9 percentile of that range with the top of the range itself higher by only 4.1 percentage points. While there is some setback to confidence expected in April, conditions in Germany remain very solid and for the most part extremely high-valued. Economic expectations are the exception.

Germany vs. other Europeans

We contrast the German experience with the readings from Italy, France and the U.K. although the comparisons are not 'strong' since the GfK is a look-ahead index that is updated through April (and it is still March in the real world) while data from these three countries are up-to-date at the moment only through February. Nonetheless, this is what is most topically available.

Italy

Italy, while having had one of the most miserably-performing economies in the euro area since the great recession, nonetheless logs a consumer sentiment reading with an 86.7 percentile standing. In February the index was unchanged at the January level and January had been a step down from December. Still, for an economy that is being torn politically and at odds with the EU, Italian economic performance has been poor yet consumers have remarkably strong spirits.

France

France also logs a consumer metric that is unchanged in February. The January reading, however, represents a step up from its December level. The level of confidence in France has only a 55.2 percentile queue standing, marking it as slightly above its historic median. The current reading is below its historic average and is below the midpoint of its high-low range.

The United Kingdom...if it ain't broke don't Brexit?

The U.K. is beset with Brexit woes and with a still-scheduled March 29 departure date set and no deal with the EU yet and no formal inquiry for an extension requested. The U.K. quite simply is sailing toward a potentially hard Brexit departure. But yesterday the U.K. parliament seized control of the Brexit process for one day to see if it might break the impasse. Looking at the process as a whole body and with highly charged partisan tensions still at work but doing it in a bargaining framework outside a formal coalition setting, it is possible that a deal of some sort might be struck. But it is not clear that there is anything parliament can accomplish or any modification of Theresa May's deal that will work since any proposal must to go back to the EU for acceptance. And there is no guarantee that if parliament is able to conjure a compromise short of hard Brexit that the EU would either accept it or find it promising enough to move the goal posts on the Brexit exit date to talk about it some more. Against such a background, it can't be surprising that the U.K. confidence index also is stuck for two months running at a level lower than it was in December and at a standing in the lower 29th percentile of its historic queue of data.

Global linkages

Global economic data have been weak. And this morning Charles Evans of the Chicago Fed is in Asia giving a talk, mentioning that in part the U.S. policy decision is going to depend on how much Asia slows down. Clearly, the global linkage have become more important, but as we can see from the European confidence readings, there are still very different impacts being assessed by consumers in countries that trade very closely and in some cases are connected through special economic linkages as Germany, France and Italy are. And the U.K. formally still has such a connection since its EU membership card has not yet expired.

Globalization is not homogenization

Globalization is a funny thing. Different countries and companies have exploited it to differing degrees. The impact of globalization is different for each country according to a number of factors. With global slowing, one might expect Germany where exports are 50% of GDP to be hit hardest by a slowdown, but that has not been the case. Not surprisingly, it is the U.K. and its repeated failed attempt to reformulate its international linkages that has hurt confidence the most. No one has any idea what is coming next. Uncertainty is simply bad for business.

Globalized risks

But trade negotiations between the U.S. and China drag on. Brexit decisions continue to be postponed. The U.S. and the EU have yet to pick up their trade talks. There is a lot of geopolitical uncertainty in the mix as well. Against that background, how can it be surprising that the yield curve in the U.S. has inverted sending a warning shot across the bow of global growth expectations? The inverted U.S. yield curve is – or should be- one of the most feared signals in all of economics. But for now the U.S., the Fed and the global economy continue to treat it as though it is just a stub of the toe, or maybe a slip, or a stumble, maybe a pain in the appendage, but it is not being treated as the precursor to a fall. Why not? Yield curve inversion has been a reliable signal of recession over the last 50 years at least. I guess one reason is that globally consumer confidence is still solid. And in the U.S., confidence continues to be at a high level even if of mixed performance. Confidence had been recovering from its own stumble- at least until the March reading. Today's the Conference Board report on U.S. confidence may raise new questions about the consumer. But as long as denial is a viable option, there will be deniers. Beware of what you think, believe or deny. We are entering the part of the business cycle that demands brutal honesty for survival.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief