Global| Sep 01 2008

Global| Sep 01 2008Germany Retail Sales Give Way…

Summary

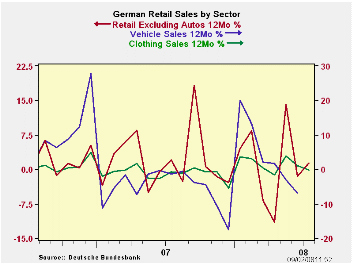

German retail sales have now put in back-to-back declines, each of substantial magnitude. Real and nominal sales are now lower over 12 months. Over 6 months the rate of decline is more severe and over 3 months the pace of decline is [...]

German retail sales have now put in back-to-back declines, each of substantial magnitude. Real and nominal sales are now lower over 12 months. Over 6 months the rate of decline is more severe and over 3 months the pace of decline is even more severe. The loss in momentum is unmistakable.

For the current quarter, the results are very poor. It is July, so we calculate the growth RATE in July centered over the average for sales in Q2. There are different ways to annualize things. We compound the growth rate and present it as an actual rate from its current position compared to the actual Q2 base. Since Q2 centers in May we take the resulting growth rate to the 6th power to annualize it. That leaves us with retail sales falling at a 4.3% pace in Q3 or at a -11.3% pace in real terms (ex autos). However if we treat the level of sales in July as the level for the whole quarter we compound by four instead of six giving us a still weak growth rate of -7.7% for real ex-auto sales. There is not much arguing with the notion that German retail sales are falling sharply.

| German Real and Nominal Retail Sales | QTR | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Nominal | Jul-08 | Jun-08 | May-08 | 3-MO | 6-MO | 12-MO | YrAgo | Saar | |

| Retaill Ex auto | -1.3% | -1.4% | 1.7% | -4.1% | -3.0% | -0.2% | -0.7% | -4.3% | |

| Food Bev & Tobacco | -1.6% | -1.2% | 0.1% | -10.4% | -5.0% | -1.2% | -4.3% | -13.4% | |

| Clothing footwear | 2.8% | -10.2% | 15.1% | 27.4% | 1.3% | 1.5% | 2.1% | 0.4% | |

| Real | |||||||||

| Retail Ex auto | -1.5% | -1.4% | 1.3% | -6.2% | -5.4% | -3.2% | -1.0% | -11.3% | |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief