Global| Dec 11 2013

Global| Dec 11 2013Germany Is a High Inflation Country in EMU! But for How Long?

Summary

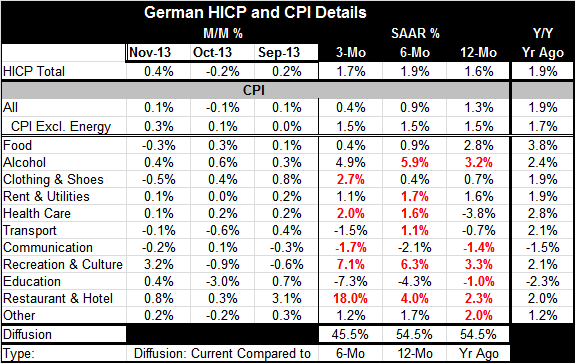

German inflation remains subdued despite a headline gain of 0.4% in November. Year-over-year the German HICP is up by 1.6% and its growth rate is only a touch greater over three-months and six-months. The diffusion calculation on the [...]

German inflation remains subdued despite a headline gain of 0.4% in November. Year-over-year the German HICP is up by 1.6% and its growth rate is only a touch greater over three-months and six-months.

German inflation remains subdued despite a headline gain of 0.4% in November. Year-over-year the German HICP is up by 1.6% and its growth rate is only a touch greater over three-months and six-months.

The diffusion calculation on the eleven categories of inflation shows a slight tendency for inflation to accelerate over 12 months with a diffusion reading of 0.54. Although overall inflation at 1.6% is below its pace of 1.9% of one year ago, inflation has accelerated in slightly more price categories that it has decelerated over the past 12-months. With 0.50 as a neutral inflation pressure reading, the 0.54 reading is one of only slight inflation pressure. Diffusion tells roughly the proportion of categories with inflation accelerating over a period. Over six months the diffusion gauge stays at 0.54 with headline inflation at 1.9%; that marks a moderate inflation tendency. But over three-months inflation tendencies are moderately withering with a headline at 1.7% and a diffusion gauge under 0.50 at of 0.455.

The chart shows that both total and ex-energy inflation trends are still working lower for Germany. Neither the Bundesbank not the European Central Bank should have any worries based on Germany's inflation trends, but that is almost always the case. The inflation situation for all of EMU is a different measure that includes the metrics of all EMU members. What does that look like?

November is a reading too fresh for many EMU members. But eight EMU members have reported out a preliminary inflation result for November. Of them, Germany has the strongest year-over-year inflation at 1.6%: the strongest inflation, not the lowest, for a change.

Austerity countries are still seeing prices depressed by their past austerity programs and by continued weak demand. Greece has the lowest year-over-year inflation in November at -2.9%. Portugal is next lowest at +0.1%; Spain is the third lowest at 0.3%; Italy checks in at 0.6%. That leaves Belgium at 0.9%, Luxembourg at 1.1% and the Netherlands at 1.2%.

That means that based on CPI data Germany is losing competitiveness to the rest of (early reporting) EMU. Since Germany has built a huge competitive advantage by running low inflation rates since the beginning of EMU, Germany has a huge competitive advantage. It not only can afford to give some away but doing so will make EMU more viable as internal competitive conditions will have less variance and the weak countries in EMU will become stronger, more solid members.

Before jumping to the conclusion that EMU is finally doing something to enhance its long-run stability by making some structural competitive changes, we need to note that the austerity countries are still doing too badly economically to permit us to think that this new lower inflation they are churning out can last. In the case of Greece a drop in the HICP of 2.9% year-over-year clearly is not sustainable.

But we need to follow inflation trends in the future to see whether Germany will continue inflating relative to the rest of EMU. For the time being this price convergence tact is working. But it is working with German inflation at 1.6%, in line with its historic norms. Other countries are unlikely to be able to keep their inflation rates significantly below Germany's -and to achieve growth- if Germany sticks to its historic inflation pace.

That will be the real test of price level convergence, whether Germany is willing to run slightly higher inflation so that the struggling EMU members can still have some inflation (below Germany's pace) and have some growth so they can make competitiveness gains vis a vis Germany. The current constellation of inflation rates is simply not sustainable for the current low inflation members in EMU to have their low inflation and to achieve growth too. EMU has yet to make the truly hard choices to keep the union together.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief