Global| Apr 07 2017

Global| Apr 07 2017Germany: Dispelling the Myth of Hard-Data Weakness/Soft-Data Strength?

Summary

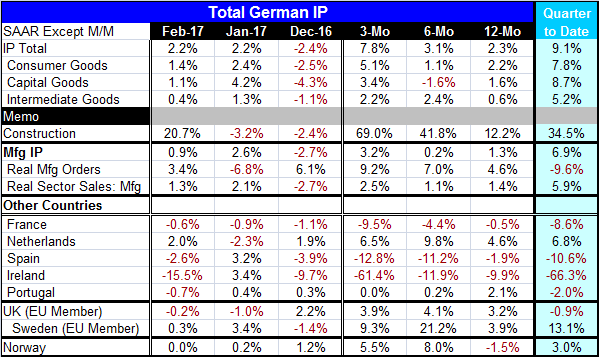

German industrial output has put in a better-than-expected February with output rising by 2.2% month-to-month, the same as in January. Overall output is now expanding at a robust 9.1% annualized rate two months into Q1... so much for [...]

German industrial output has put in a better-than-expected February with output rising by 2.2% month-to-month, the same as in January. Overall output is now expanding at a robust 9.1% annualized rate two months into Q1... so much for the assertion of weakness in the so-called hard-data or accounting data reports compared to soft-data reports. Soft data or survey data reports (like the PMIs) have been showing strength for some time. The hard-data or accounting data have been slow or reluctant to follow. We have pointed out that survey type PMI data, for example, are indicators of breadth, not of strength. These sorts of indicators tend to be sensitive and can indicate activity stirring at its earliest point, but can also over-predict the strength of a move. Still, the German data at least are coming in strong behind their PMI values. Both Germany and the EMU manufacturing PMI readings are on five-year high readings. Over the past five years, the current German IP gain ranks in the top 30th percentile of all year-on-year growth rates. So while the PMI is tipping off an authentic rebound, it also is exaggerating its strength- at least so far. German hard data sequential growth rates from 12-month to six-month to three-month show the pace of output is still accelerating.

German industrial output has put in a better-than-expected February with output rising by 2.2% month-to-month, the same as in January. Overall output is now expanding at a robust 9.1% annualized rate two months into Q1... so much for the assertion of weakness in the so-called hard-data or accounting data reports compared to soft-data reports. Soft data or survey data reports (like the PMIs) have been showing strength for some time. The hard-data or accounting data have been slow or reluctant to follow. We have pointed out that survey type PMI data, for example, are indicators of breadth, not of strength. These sorts of indicators tend to be sensitive and can indicate activity stirring at its earliest point, but can also over-predict the strength of a move. Still, the German data at least are coming in strong behind their PMI values. Both Germany and the EMU manufacturing PMI readings are on five-year high readings. Over the past five years, the current German IP gain ranks in the top 30th percentile of all year-on-year growth rates. So while the PMI is tipping off an authentic rebound, it also is exaggerating its strength- at least so far. German hard data sequential growth rates from 12-month to six-month to three-month show the pace of output is still accelerating.

Hard-data/soft-data U.S. and Europe- some sector observations

For what it's worth, I have made the same point about U.S. IP. U.S. IP has been weak for different reasons: weather and energy. The U.S. manufacturing IP index has been stronger than the IP headline because utilities (and until recently, mining output, too) have been weak. Looked at by sector, manufacturing has been quite solid. If you had removed the energy sector, there would have been more strength. So one problem with IP type data is that one-sector can depress the whole report if the monthly swing is big enough. In the U.S., output has been rebounding on a broader scale, but that has been masked by the energy/utilities performance. So keep an eye on hard data looking ahead. An exception to this is retail sales where some are still quite optimistic, but the recent data have been weak (in both the U.S. and in Europe) and where U.S. data are queued up to underperform in March because of troubles in the auto sector- troubles that are sure to last more than one month as rising interest rates, deteriorating credit and an avalanche of cars coming off lease are going to hit this sector hard. Europe's consumer rebound has also leaned hard on its auto sector, which has been a bright spot. But other retail sales measures have been uneven and much weaker than counterpart retail PMIs. Actual retail sales also have lagged behind consumer sentiment readings.

Germany's strength is solid and widespread

All German sectors are showing solid rates of growth. The three-month growth rates range from a 5.1% pace for consumer goods output to 2.2% for intermediate goods. Still, there is not a clear progression of acceleration in any of the three principle sectors: consumer goods, capital goods or intermediate goods. Yet, in the quarter-to-date, the sector annualized growth rates range from 8.7% for capital goods to 5.2% for intermediate goods with consumer goods at a 7.8% pace. Construction output is up at a heated 34.5% annualized rate in the quarter-to-date and is showing clear sequential acceleration.

Orders and sales

German real sector orders, as we saw earlier this week, have a solid but unspectacular trend. Orders expressed in real terms have been somewhat more erratic and are actually contracting at a 9.6% annualized rate in Q1, taking some of the glow off of the manufacturing sector outlook.

Elsewhere in Europe

In Q1 so far Germany is the exception at least in terms of early reporters of 'hard data.' For the five early EMU hard-data-reporters, four have output drops logged in February. France, the second largest EMU economy, is one of them and it reports two monthly drops in a row. The Netherlands reports a February rise in output, but only after an even larger drop in January. On balance, four of five of these early reporters also have output declining two months into the first quarter, the Netherlands is an exception. The U.K. also reports an IP drop in February and is logging a decline two months into Q1. Sweden and Norway are exceptions of sorts with a small output gain from Sweden in February and flat performance from Norway. But Sweden has sharply rising output two months into Q1 2017 while Norway has a moderate 3% growth rate in progress.

European cross-currents as always

These data reconfirm that Europe is still subject to various cross currents from economic trends. Whatever it is that binds Europe together, it does not do so tightly enough to fuse the real sectors. Of course, there is the common currency and the EU membership that harmonizes a lot of regulation, but there are still a lot of loose ends. Prices are more in unison, but still not completely so. And these conditions explain why the currency union is such an ongoing problem. There is only one monetary policy, one currency exchange rate and yet many different mini-business cycles and varying credit conditions and inflation conditions in progress.

EMU hard data

It is still true that the soft data are relatively stronger than the hard data. What we see in this report suggests that the hard data IP dynamic for the EMU is not going to be a match for its soft data strength- at least not this month. Yet, there may be some convergence in train. Germany is digging itself out and showing progress as its hard data close the gap with its soft data counterpart. But I expect it will quite some time before - or even if - Germany gets ready to post its strongest year-on-year IP growth rate in five years to match its Markit manufacturing PMI standing.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief